Uncle Liu started his tobacco and alcohol business at the age of 28. After so many ups and downs over the years, he is now past retirement age.

The overall economic environment has not been very good in the past two years, and Uncle Liu's business has also been greatly impacted. Uncle Liu, who had originally thought about retiring, simply closed his business.

He originally thought that the business was closed and that was it, but he didn't expect that there would be many tedious things waiting for him afterwards, such as tax issues and business registration cancellation issues.

There is another problem. Over the years, Uncle Liu has applied for many bank cards from different banks for convenience, but these cards are basically useless now.

In the past, in order to ensure the normal use of the card, Uncle Liu would regularly deposit some small amounts of money into it. He thought that he just needed to withdraw all the money from the card and put it aside when the time came.

Anyway, there is no money in it, so the bank can't deduct his money. He has also not heard of any fee required to keep the bank card, and the card does not need to be used for living.

After making his plan, he went to the bank to withdraw money and talked to the lobby manager about his idea. However, the lobby manager said that his way of thinking was a bit problematic.

After some explanation from the lobby manager, Uncle Liu finally understood the significance of bank cards and how to handle them according to his needs at different times.

Do you know what to do with a bank card with no money in it? Should you cancel it directly or keep it?

1. Bank Card Overview

We live in a modern society where almost everyone comes into contact with and uses bank cards, especially adults.

Because everything we do in our daily lives, including food, clothing, housing and transportation, requires the use of bank cards or the functions of bank cards.

Bank cards themselves have functions such as transfer settlement, cash deposit and withdrawal, consumer credit, etc. Therefore, in general, we will make functional subdivisions of bank cards.

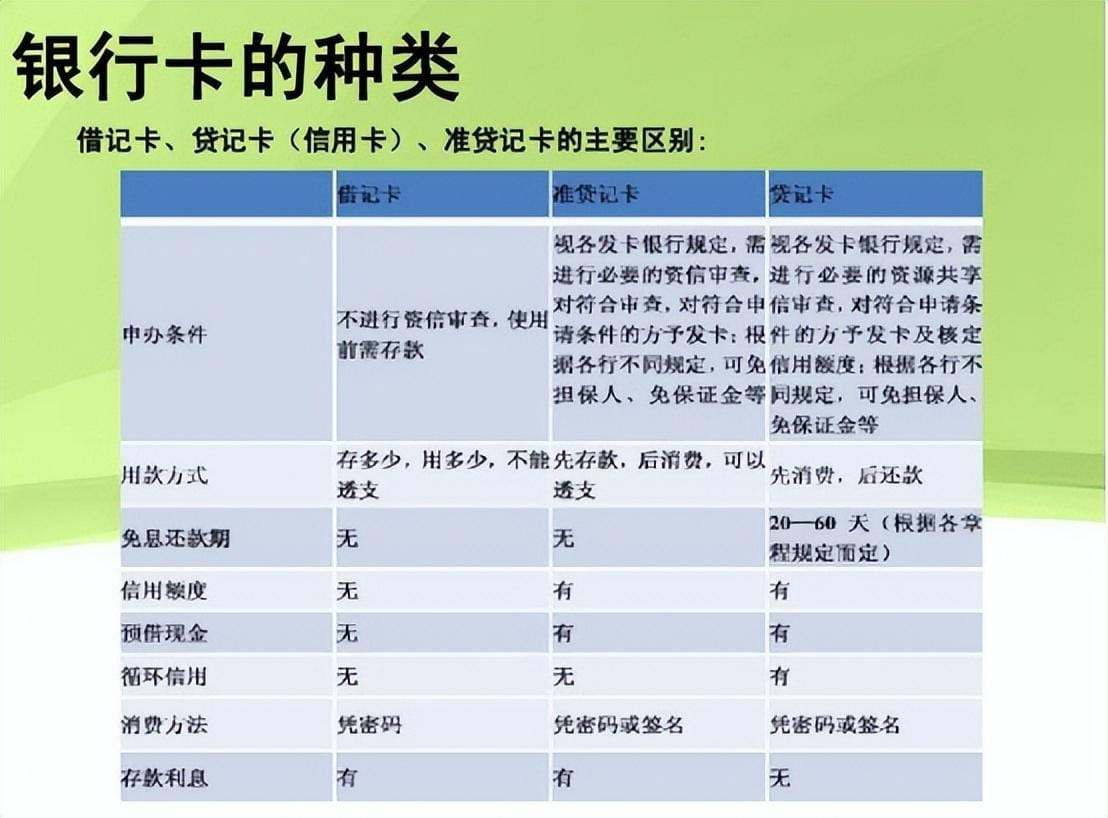

For example, depending on whether the cardholder has a credit limit, it is divided into debit cards and credit cards.

A debit card is what we often call a bank card. Generally speaking, it has the functions of storing value and transferring money, as well as depositing and withdrawing cash and making purchases.

Debit card purchases can be made online or at bank ATMs or POS machines, but there is no overdraft function.

The functions of credit cards complement those of debit cards. Credit cards are divided into credit cards and quasi-credit cards.

A debit card is what we often call a credit card. You can only make purchases within the credit limit granted by the bank and then make repayments.

One feature of a credit card is that it has a minimum repayment amount, which means that you do not need to pay off all your purchases at once, but can pay them off in installments.

Quasi-credit cards are a type of credit card unique to China. This type of card has the functions of depositing and withdrawing cash, transferring and settling accounts, conducting online transactions, and credit consumption.

From these functions, we can see that it is relatively difficult to apply for and own a quasi-credit card. The threshold is high and it is more troublesome to use. Therefore, quasi-credit cards are relatively rare nowadays.

Of course, there are many other different classifications of bank cards. For example, magnetic stripe cards and chip cards are distinguished according to the different information carriers.

There are also different cards used at home and abroad called overseas cards and domestic cards, as well as unit cards that many units will specifically apply for and corresponding personal cards.

There are also RMB cards that are exclusively for use with RMB and foreign currency cards that are for other currencies. There are also dual-currency cards that can be used in both currencies.

These types of cards appear less frequently than the debit and credit cards that we come into contact with most in our daily lives.

So the bank card we are studying is whether it should be cancelled or retained once it is determined that it will not be used for a period of time, so we are referring to the two types of cards: debit cards and credit cards.

2. How to deal with idle bank cards

When we were children, our parents opened a bank card for us to save our “New Year’s money”, and when we graduated from high school, we opened a bank card to deposit and withdraw tuition fees.

Then, after going to college, you can apply for at least one convenient bank card, and after entering the society, you can apply for a salary card, a mortgage and a car loan card...

Chinese people basically have many bank cards in their lifetime, and these bank cards may be used frequently over a period of time.

But most of them will sit quietly in our unused wallets or drawers at home after they have served their purpose.

These idle bank cards are often forgotten by their owners for a long time because the bank does not charge them management fees or other fees, until the next opportunity to use them comes.

Many people keep these idle bank cards for a long time perhaps in order to avoid spending more time and energy when this opportunity comes.

But is this really the right thing to do? In fact, it is not. First of all, if there is no record of using the bank card within a certain period of time, the bank will "soft freeze" the bank card.

That is, the card will be put into dormant mode in the bank system, and basic operations such as transfer and withdrawal will not be possible. If you want to use the card again, you still need to go to the bank to activate it.

Therefore, there is no such thing as keeping the card and waiting to use it directly when you need it one day. It is meaningless to keep the bank card.

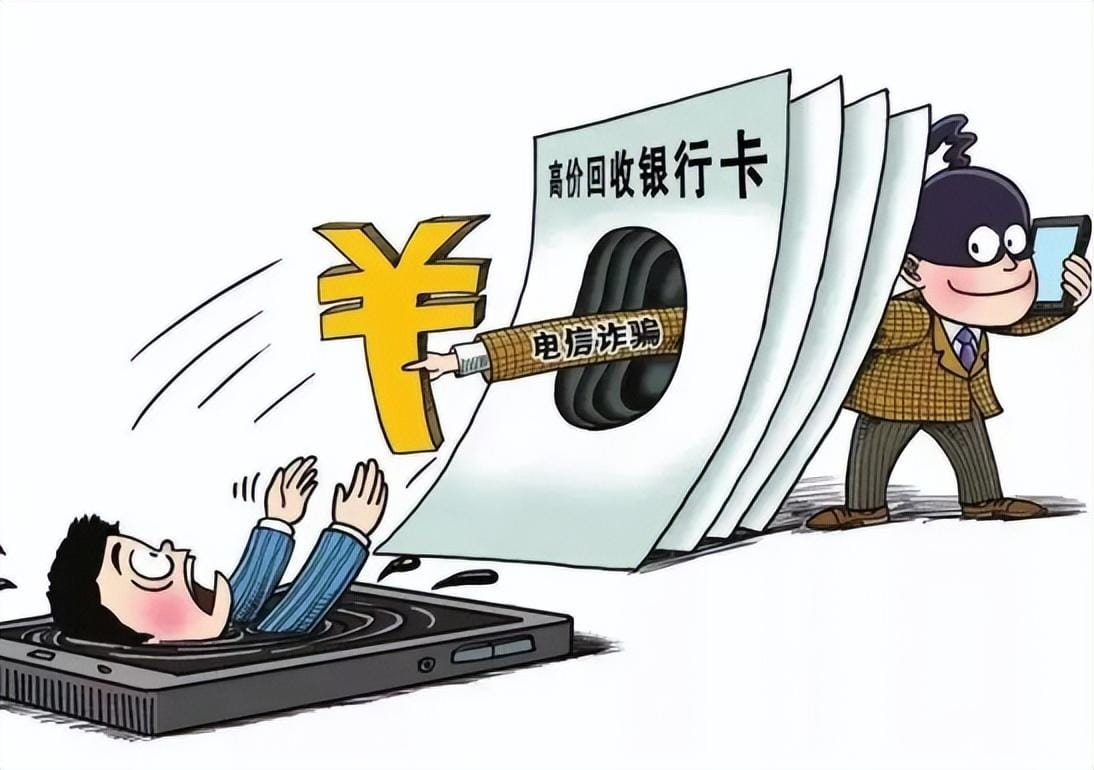

In recent years, there have been many crimes such as telecommunications fraud targeting our people, and these fraudsters need a large number of bank cards.

If we have idle bank cards, they may be used by criminals without our knowledge or if they are lost.

Once criminals obtain the basic information of your idle bank cards, the consequences will be immeasurable.

Some people may say that since bank cards will be put into dormant mode after not being used, criminals will not have any opportunity to take advantage of them, so there is no harm in keeping them.

However, there is a long period of time between the bank's transition to dormant mode and its decision not to use the bank anymore, which may even last for several years.

These years are dangerous, so for the safety of your own information and property, it is best to cancel idle bank cards at the bank in a timely manner.

The above are suggestions for handling debit cards, but what about credit cards?

3. How to deal with idle credit cards

Compared with bank cards, credit cards are actually a little more complicated because credit cards themselves have credit limits.

If the card is not used for a long time or is accidentally lost, some people can use technical means to swipe the money out of the card.

The most direct loss caused by this malicious overdraft behavior is the economic loss of the owner.

If the owner fails to return the maliciously overdrawn amount in time, or forgets to repay the annual fees and other charges incurred by the credit card after not using it for a long time.

In the end, not only will the amount you need to repay increase due to the accumulation of interest, but your personal credit status will also be affected due to failure to comply with the credit card usage agreement.

Credit reporting is a very important credit evaluation system for adults. If credit problems arise due to failure to cancel idle credit cards in a timely manner, it would be too unprofitable.

In general, if a credit card is left idle for a long time and you forget to pay the interest and annual fees regularly, which are fees that will be incurred regardless of whether it is used or not, the consequences will be more serious.

Therefore, once you decide not to use your credit card, it is best to go to the bank where you opened the account to cancel it as soon as possible and ensure that all overdrafts are settled.

IV. Bank Card and Protection of Your Own Interests

Bank cards are very important to us, especially when using them, we need to pay some attention to ensure the safety of our property.

For example, when making deposits or withdrawals at a bank counter or ATM machine, be sure to cover your face when entering your password.

Some ATM machines may be manipulated by criminals in an unusual way in order to obtain information such as the bank card holder's password, so when depositing and withdrawing money, you should choose a regular, large self-service bank.

Try to activate the SMS notification service so that cardholders can keep track of their bank card status at any time and detect any abnormalities as soon as possible.

Do not keep bank cards, ID cards or other identification documents together to avoid unnecessary financial losses if they are lost.

When using a bank card, especially a credit card, make sure the card is always within your sight and confirm the amount when entering your password or signing a bill.

Because there is a chip inside the bank card, be sure to stay away from electrical appliances or other items with strong magnetic fields.

Once you discover that there is a problem with your bank card or credit card, or if there is a sudden change in your account without your knowledge, you must call the bank immediately and ask the bank staff to report the loss.

When taking your bank card out, be sure to put it in a bag that will not be demagnetized to prevent it from being maliciously demagnetized without your knowledge.

Remember, protecting bank cards is protecting the safety of our property, and it is never wrong to be careful with them.

Conclusion

In the past, it was common for each person to hold multiple bank cards, which not only resulted in a waste of resources, but also created many unnecessary security risks.

Therefore, since 2016, our country has issued relevant notices stipulating that each person cannot hold more than 4 bank cards in the same bank.

In recent years, the functions of physical bank cards have gradually been replaced by digital bank cards. I believe that in the near future, we will no longer need so many bank cards.

Therefore, there will no longer be a situation where there are too many idle bank cards at home and you don’t know what to do with them or you are too lazy to deal with them, which eventually leads to adverse consequences.

However, now, if our family or friends and relatives still don’t know how to deal with bank cards with no money, it is best to go to the bank to cancel them.

It should be noted that cancellation refers to the cancellation of the card, not the account. The card is only cancelled so that you can re-apply for it if you need it in the future.