Suppressing circulation is beneficial to these projects, which makes price manipulation easier.

Author: Mosi

Compiled by: TechFlow

In the token world, perception is everything. Like Plato’s Allegory of the Cave, many investors are trapped in the shadows — misled by distorted projections of value by bad actors. In this article, I will reveal how some venture capital (VC) funded projects systematically manipulate the price of their tokens by:

Keep the false float of the token as high as possible.

Keep the real float of the token as low as possible (to make it easier to increase the token price).

Taking advantage of the fact that the actual circulation is extremely low to push up the token price.

Shifting from a “low float/high FDV (fully diluted valuation)” model to a “false float/high FDV” model

Picture: No! I am not a low float/high FDV coin! I am a community first!

Picture: No! I am not a low float/high FDV coin! I am a community first!

Earlier this year, memecoins surged in popularity, pushing many VC-backed tokens out of the mainstream spotlight. These tokens are called “low circulation/high FDV” tokens. However, with the launch of Hyperliquid, many VC-backed tokens have become difficult to invest in. Faced with this situation, rather than fixing their flawed token economics models and focusing on developing real products, some projects have chosen to double down on their efforts by artificially depressing circulating supply while publicly claiming the opposite.

Suppressing circulation is beneficial to these projects because it makes price manipulation easier. Capital efficiency can be significantly improved through behind-the-scenes transactions—for example, the foundation sells locked tokens for cash and then buys them back on the open market. Additionally, this practice poses significant risks to short sellers and leveraged traders, as low true circulation makes these tokens extremely susceptible to price pumps and dumps.

Next, let’s look at some practical examples. This is by no means an exhaustive list:

1. ABOUT

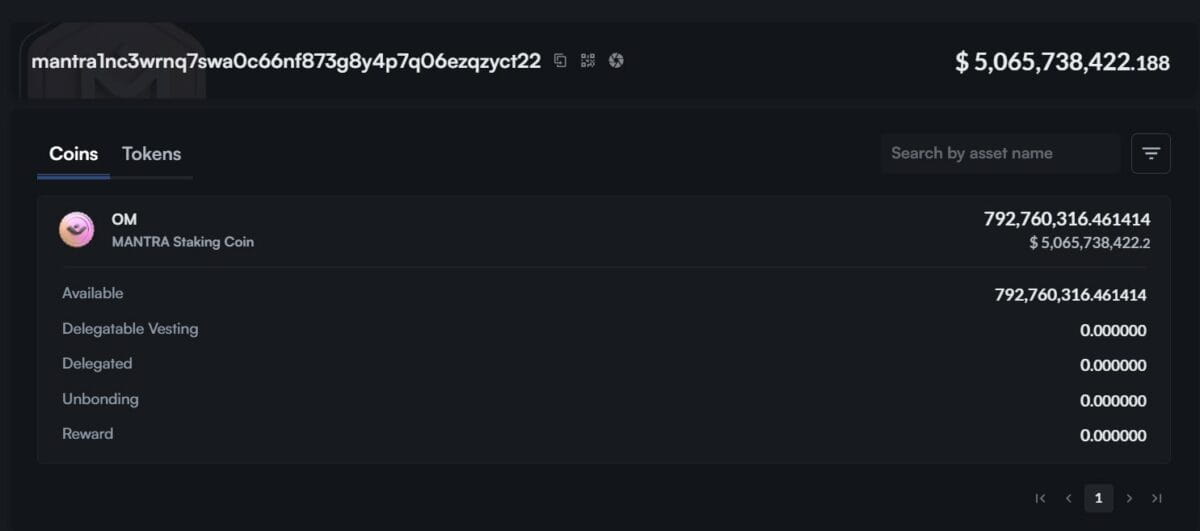

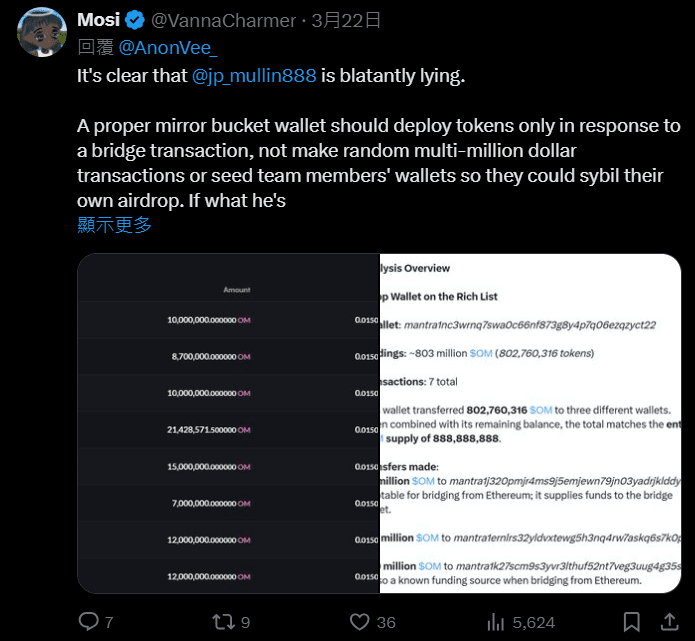

@MANTRA_Chain This is the most obvious example. For those wondering how a project with only $4M in total value locked (TVL) can have a fully diluted valuation (FDV) of over $10B, the answer is very simple: they control the majority of $OM in circulation. Mantra holds 792M $OM (i.e. 90% of the supply) in a single wallet. It’s not complicated — they didn’t even bother to spread the supply across multiple wallets.

When I asked @jp_mullin888 about this, he claimed that this is a “mirror storage wallet”. This is complete nonsense.

So, how do we know the real float of Mantra?

We can calculate this through the following calculation:

980M (circulating supply) – 792M $OM (team controlled supply) = 188M $OM

However, this 188M $OM figure may not be accurate. The team still controls a significant portion of $OM, which they use to perform a sybil attack on their own airdrop, further squeeze exit liquidity, and continue to control the circulating supply. They deployed about 100M $OM to Sybil attack their own airdrop, so we also need to deduct this part of the tokens from the actual circulation. More relevant information can be found here:

Finally, we get the actual circulating supply to be… boom boom… only 88M $OM! (Assuming the team does not control a greater supply, but this assumption is obviously not reliable). This makes Mantra’s actual circulation only $5.26 million, a huge gap from the $6.3 billion shown on CoinMarketCap.

The low real float makes it easy to manipulate the price of $OM and liquidate any short positions. Traders should be terrified of shorting $OM because the team controls the majority of the circulating supply and can pump or dump the price at will. This situation is like trying to gamble with @DWFLabs on some shitcoin. I suspect that Tritaurian Capital — which borrowed $1.5 million from @SOMA_finance (@jp_mullin888 is a co-founder of SOMA, while Tritaurian is owned by Jim Preissler, JPM’s boss at Trade.io) — and some funds and market makers in the Middle East may be behind the current price action. These operations further compress the true circulation, making it more difficult to calculate.

This may also explain their reluctance to release the airdrop and their decision to implement a lock-up period. If they actually did an airdrop, the true circulating supply would increase significantly, likely causing a significant drop in price.

This isn’t some sophisticated financial engineering, but it does look like an intentional plan to reduce the true circulation of tokens and drive up the price of $OM.

2. MOVE

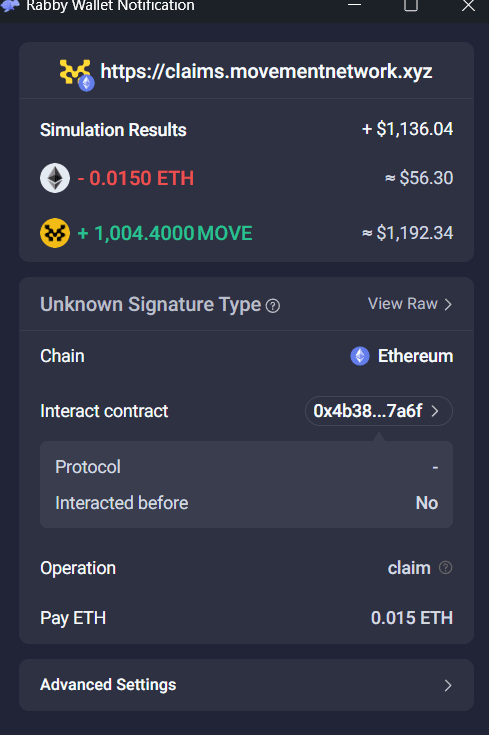

@movementlabsxyz: During the airdrop claiming process, Movement allows users to choose one of two methods: claim the airdrop on the Ethereum mainnet (ETH Mainnet); or claim the airdrop on their yet-to-be-launched chain in order to receive a small reward. However, just a few hours after the collection was opened, they took a series of actions:

A fee of 0.015 ETH (about $56 at the time) plus Ethereum’s gas fee was added to all users who received their funds on the Ethereum mainnet, which discouraged many testnet users with small balances;

Reduced Ethereum mainnet allocation by over 80% while still retaining the above fees;

The collection process has been stopped;

Limit collection time to a very short period.

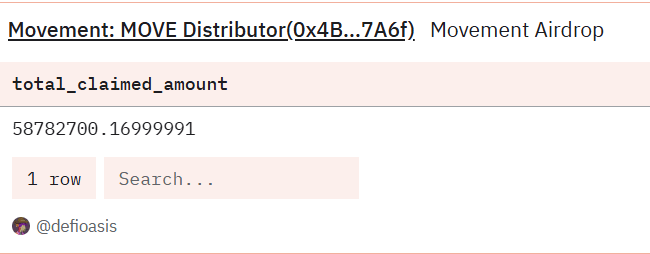

The result is obvious, only 58.7 million MOVE were claimed. That is to say, out of the 1 billion MOVE originally planned to be distributed, only 5% was successfully received.

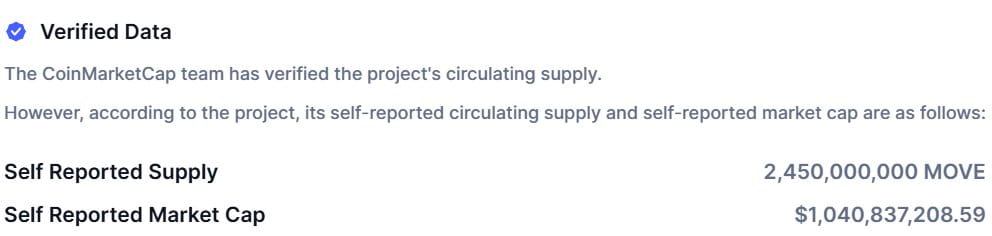

Next, let’s perform the same calculations for MOVE as we did for Mantra. According to CoinMarketCap, MOVE has a self-reported circulating supply of 2.45 billion (2,450,000,000).

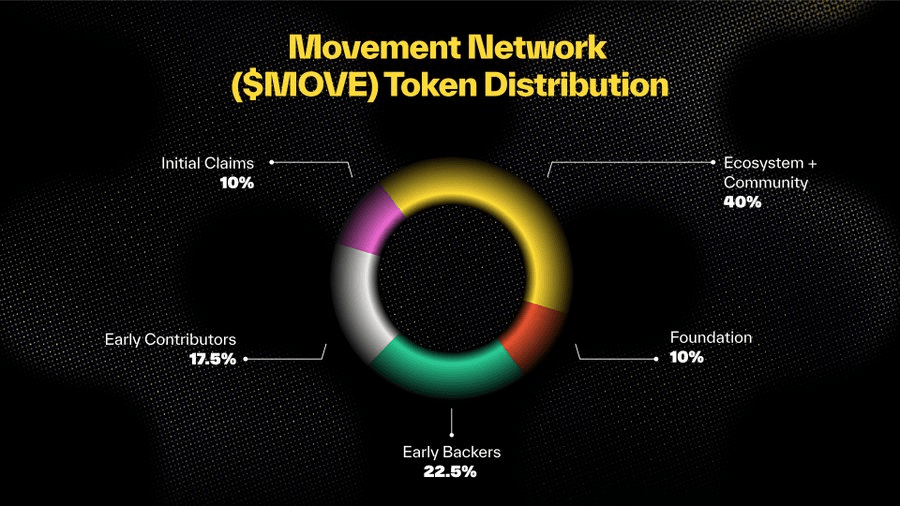

However, according to Move’s pie chart data, there should only be 2 billion (2B, foundation + initial collection) tokens in circulation after the airdrop. So, suspicious activity is already starting to appear here, as 450 million (450,000,000) MOVEs cannot be accounted for.

The calculation is as follows:

2,450,000,000 MOVE (reported circulating supply) – 1,000,000,000 MOVE (foundation allocation) – 941,000,000 MOVE (unclaimed supply) = 509 million (509,000,000 MOVE, or $203 million in REAL float).

This means that the true circulating supply is only 20% of the self-reported circulating supply! Additionally, I find it hard to believe that every one of these 509 million MOVE is in the hands of users, but leaving that aside for now, let’s assume that this is the actual true circulation.

So, what happened during this period of extremely low true circulation?

Movement pays WLFI a fee for purchasing MOVE tokens.

Movement paid REX-Osprey a fee to file an ETF for MOVE.

Rushi (the person in charge) went to the New York Stock Exchange (NYSE).

Movement engaged in a complex series of operations with funds and market makers, selling locked tokens to them in exchange for cash, allowing these institutions to bid and drive up prices.

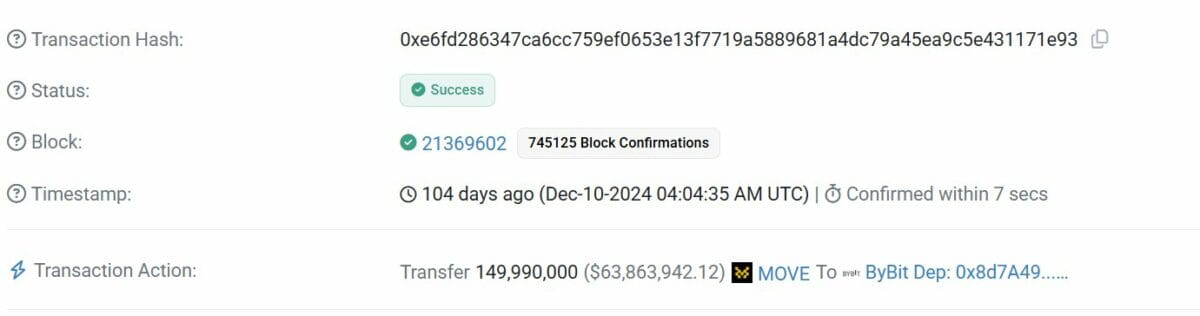

The team deposited 150,000,000 (150,000,000) MOVE tokens at the peak of the price on the Bybit platform. They probably started selling from the peak as the price has been falling since then.

Around the time of the Token Generation Event (TGE), the team paid $700,000 per month to a Chinese KOL (Key Opinion Leader) marketing agency in order to be listed on Binance and thereby gain more exit liquidity in the Asian market.

Is this a coincidence? I don't think so.

As Rushi puts it:

Kaito

Kaito

@Kaitoai is the only project on this list that has a real product. However, they have also adopted similar behavior in their current airdrop campaign.

As CBB noted above, Kaito distributed their airdrops, but only a tiny percentage of people actually claimed them. This also affects the real float. Let's do the math:

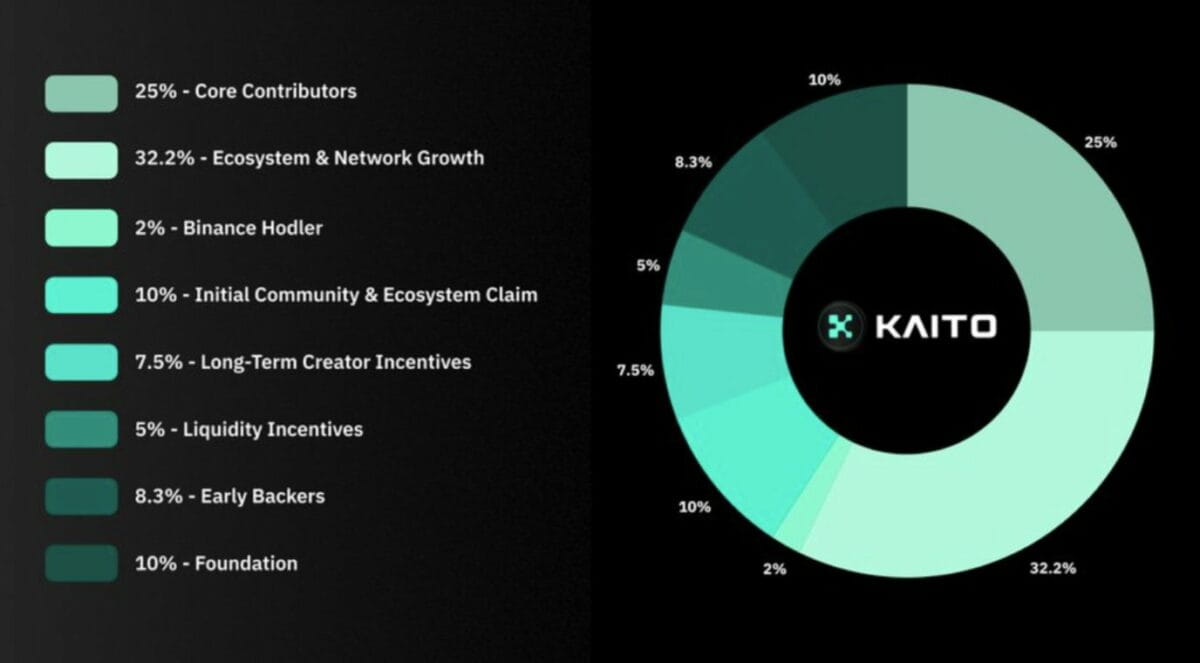

According to CoinMarketCap, Kaito has a circulating supply of 241 million (241,000,000) and a market cap of $314 million. I assume this number includes: Binance coin holders, liquidity incentives, foundation allocations, and initial community and collection shares.

Let’s break down this data and find out the true circulating supply:

Real circulation = 241,000,000 KAITO – 68,000,000 (unclaimed) + 100,000,000 (held by the foundation) = 73 million (73,000,000) KAITO

This means that the actual circulating supply corresponds to a market capitalization of only $94.9 million, which is much lower than the value reported by CMC.

Kaito is the only project on this list that I’m willing to give some credit to, as they at least have a product that generates revenue, and from what I can tell, they haven’t been involved in as many shady practices as the other two teams.

Solution and Conclusion

CMC and Coingecko should list the true circulation of tokens, rather than those unreliable numbers submitted by the teams.

Exchanges like Binance should actively punish this behavior in some way. The current model for listing coins is problematic because you can simply pay a KOL marketing agency to drive engagement in Asia before the TGE, as Movement did.

Prices may have changed by the time I write this, but for reference, I took the prices as: $0.4 for Move, $1.3 for KAITO, and $6 for Mantra.

If you are a trader, stay away from these coins. Because these groups can manipulate prices at will. They control all circulating supply and therefore control the flow of funds and token prices. (Non Financial Advice, NFA)

Text Linking

This article is reproduced with permission from TechFlow

Source