The Fed faces a pressing problem: its reliance on data leads to a recency bias that causes excessive market volatility…

Investors appear to have been deceived by the Federal Reserve again. After the market incorrectly predicted seven times that policymakers would turn dovish, the Fed finally cut interest rates sharply last month. Only now bond yields are rising sharply again, and investors are expecting less of a rate cut.

What's going on? The answer can be summed up in one word: data dependency.

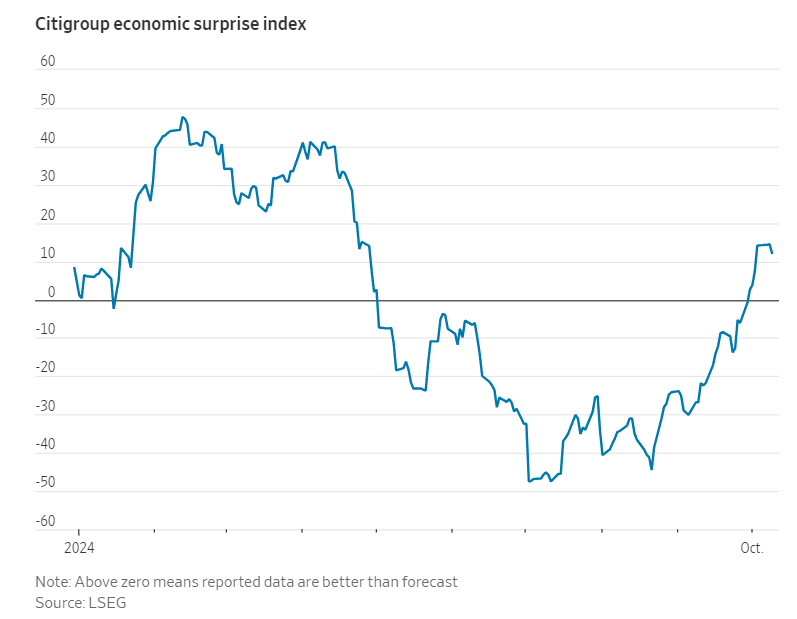

The Fed says it sets policy based on the data it receives, particularly on inflation and employment. But that data is both unreliable and far more volatile than usual, causing investors to bounce back and forth in a fog of data that first points to economic weakness and then (sometimes after revisions) to strength.

Since the Federal Reserve cut interest rates last month, economic data has been much stronger than expected. Weak employment data that prompted the Fed to cut interest rates by 50 basis points last month reversed in this month's report, recording the third-strongest reading so far this year. Both the New York and Atlanta Fed's real-time forecasts for third-quarter economic growth are above 3%, up from 2% at the end of August.

Of course, the Fed should look at the data. But relying on the data means only looking at recent data and ignoring forecasts of the impact of interest rates on the future economy. Reliance on the data creates unnecessary volatility in the bond market.

This summer, data pointed to a slowing job market, suggesting that high interest rates were hurting the economy. But now the economy appears to be doing fine, and inflation may be trickier than thought.

The latest data alone can lead to either short-term pessimism or brief exuberance, generating large swings in expectations for the Federal Reserve’s interest rates, which in turn can affect the bond market.

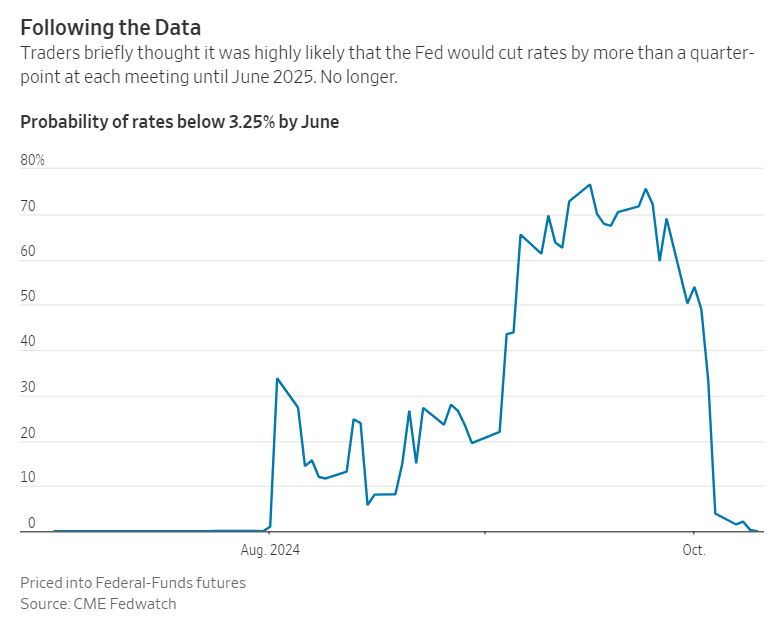

Investors are chasing groupthink rather than expressing the wisdom of the crowd. After the Fed cut interest rates by 50 basis points in September, the federal funds futures rate market is pricing in a 77% chance that the Fed will further cut rates by 175 basis points or more by June next year, according to CME Fedwatch.

Will there really be the equivalent of more than 25 basis points of rate cuts over the next six meetings? No. Traders now think the odds of another big Fed rate cut during that time are back to zero.

The Fed’s data reliance exacerbates what psychologists call the market’s recency bias — the tendency to overestimate recent information and events — by mistaking a few months of employment or inflation data for major trend changes.

When the Fed is extremely worried about inflation, it makes sense to rely on the data. It worries that high inflation will affect consumers and businesses' expectations of future inflation in a self-fulfilling spiral. To break this vicious cycle, the Fed raises interest rates, which will lead to recession forecasts and keep price expectations in check. If reported price increases lead to future price increases through expectations, then it makes sense to focus on reported price increases.

There is also reason to rely on data when interest rates are stuck at zero. For many years after the 2007-09 global financial crisis, the Fed tried to convince investors that it would raise rates slowly, waiting until the economy was running. The goal was to lower long-term rates and prevent the budding economy from being crushed by expectations of rapidly rising rates.

That has changed in post-pandemic inflation, according to a Cleveland Fed study, which found that interest rate futures traders are extremely sensitive to inflation data before each Fed meeting — true data dependence.

But at a time when the Fed is trying to guide the economy to a soft landing, this reliance on short-term data doesn’t make much sense. The Fed can afford to look through the messy month-by-month data and focus on the big picture. The job market may still be hot, but it’s no longer scorching. Inflation is still above target, but it’s no longer scary.

Data aside, the big question is not how much further inflation can be cut, but how quickly and by how much interest rates can be cut. This requires forecasting the interest rate level that the economy can withstand in the long run.

Cynics quite rightly point out that the Fed’s forecasts have been terrible in the past. Skeptics, including (Wall Street Journal) columnist James Mackintosh, point out that Fed policymakers are widely divided over where interest rates will ultimately stay.

Mackintosh believes that guiding a soft landing through the rearview mirror is not an option when interest rate changes take half a year or more to have an impact on employment and inflation. It is time for the Fed to abandon "data dependence" and work to get investors to consider the longer-term outlook.