I haven't recovered from my illness yet. I was groggy in bed all day today. I thought it was time to go to work at night, so I took some antipyretic medicine to wake up. The human body is really a precision instrument. When the temperature was 37.5 degrees, I felt fine. When the temperature reached 38.2, I was completely depressed and everything was wrong. It was just less than 1 degree, and the whole person was in two completely different states. So carbon-based life is really fragile, with such poor adaptability, how far can it go if it leaves the greenhouse of the earth...

Yesterday a reader left a message asking whether I lost money on the house I bought since Beijing’s housing prices have fallen.

I bought it in May 2016, the total price was 1400, various taxes and fees + balcony enclosure were about 100, the loan was 900, the interest rate was 15% off, about 4.16%. When the housing market was good, the same apartment in the community was sold for about 2000, but the latest transaction has dropped to 1600-1700.

If you only look at the house price, you haven't lost money, but I paid monthly installments for 7 years, of which the interest alone was around 250, so my actual cost was 1,750, so it's a loss by this calculation.

But then again, our family moved in in 2018 and have lived here for 6 years. The rent for these 6 years is about 180,000. If you add this in, you might even make a little profit.

Therefore, the most scientific calculation method for this account is: house price (including taxes and fees) + interest in previous monthly payments - market rent price over the years = actual financial cost.

According to my estimation, people who bought houses between 2015 and 2016 are generally making a small profit or breaking even, which means they are not making any money. If the current trend continues to fall for another year, those who bought houses between 2013 and 2014 will not be able to smile anymore.

A very important factor here is that the rental-to-sale ratio of real estate in China's big cities is very low. The annual rent is only about 1.5% of the house price, while the mortgage interest rate is 4-5%, so your annual financial costs continue to grow, and the accumulated amount over 5 or 10 years is not a small number. For example, my family paid 250 yuan in interest to the bank. In the past, when the house price rose, we didn't care, but now when the house price falls, we will find that the interest expenditure is very painful.

Therefore, banks must reduce mortgage loans. If they do not reduce the price, no one will buy new houses, and if the existing stock does not reduce, the loan will be repaid in advance.

I am also waiting for policy adjustments. If there is no satisfactory explanation by the end of the year, I will repay the loan in advance at the beginning of next year. You may not know that the current trust investment with a starting price of 300 yuan can only yield 4.4-4.5% after 1-2 years of lock-in. The underlying assets are various municipal bonds. Instead of earning this kind of money in fear, I might as well repay the loan in advance. The interest saved is close to 4%.

Banks should not think that they can take advantage of the high-interest loans they have been holding in the past few years. People are not stupid. As I said before: mortgage loans used to be the cheapest money people could borrow, but now early repayment is the most profitable financial management for people.

……

I told my wife to look at houses last night if she is free. Maybe it is time to change houses. The current house is OK for a family of 6, but it will be a bit crowded when the two children grow up.

There were two reasons why I didn't think about changing houses in the past few years. First, I felt that mortgage loans were cost-effective at the time. If I changed houses, the discount would have to be changed from 15% to an increase of 20-30%, and I would lose several million in total. Second, the policy was extremely unfriendly to house changing at that time. For example, in Beijing, if you sell a house and buy another one, it will be considered a second house, and the down payment must be 80%. Why change houses?

I used to think that I would live in this house for more than 20 years, until my children grow up, but now the national property market has taken a sharp turn for the worse, and the two factors that prevented me from changing houses no longer exist. So I’ll just wait and see, and consider changing houses if I find a suitable one.

I told my wife that we don’t have to stick to Beijing, Suzhou and Hangzhou are also fine. Many netizens have said that families like mine don’t have to live in Beijing. It’s true. My mindset has been opened. I originally thought about my children’s education, but after the recommendations and suggestions of friends around me in recent years, and some things have also changed my mind, I have an open attitude towards the path of my children’s education. Once I think about this, the choices in life become freer.

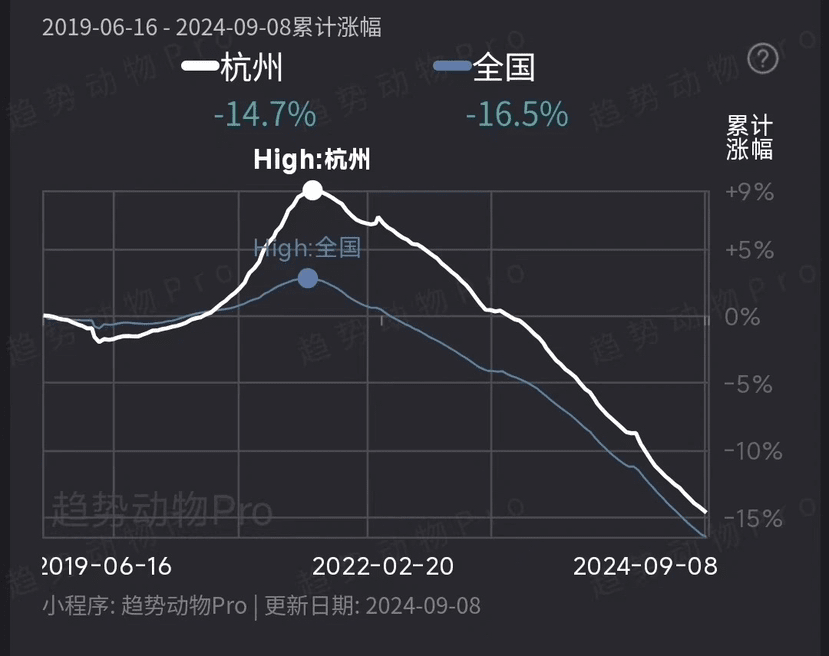

My wife just went to Hangzhou and had a very good impression of it. She spent the whole day today looking at houses there online and gave me feedback on a few houses she thought were good. Uh... a little expensive, I said there's no rush, it will be worthwhile to wait another 1-2 years in Hangzhou

It is said that the stock market and the real estate market are the two major wealth pools for Chinese people, but in fact, the stock market and the real estate market are very different. Generally, the larger the scale of a person's wealth, the higher the proportion of his wealth in the stock market. For example, for those with a net worth of tens of billions, basically 70% to 80% of their wealth is in stocks. But for middle-class families with a net worth of millions or tens of millions, real estate is usually the bulk of the family's wealth, and the stock market is just a small game for idle funds.

Therefore, even if the stock market slumps for 10 or 20 years, it will not affect social consumption, but if housing prices fall for three years, Chinese consumption will not be able to recover. This is because the rise in housing prices will greatly affect the financial security of the majority of middle-class families, and thus affect their consumption confidence.