It has fallen below 2,800. Many people forwarded a screenshot of Hu Xijin's speech at an offline event, saying that he would jump off a building if it fell below 2,800. In fact, this content is spliced together. The original words said that if his 500,000 fell to 50,000, he might jump off a building. He never said that he would jump off a building if it fell below 2,800. Even if he doesn't understand the stock market, he should be able to feel that 2,800 is not safe, and it is impossible for him to make such a harsh statement at this point.

I have communicated with Lao Hu before. His holdings are mainly blue-chip stocks and white horse stocks. If they all fall to 50,000 (-90%), then A-shares and even the country will probably be in turmoil.

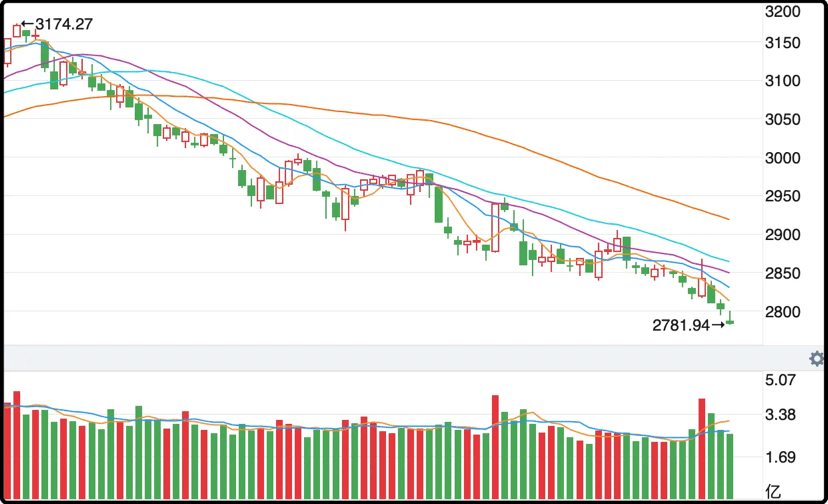

2800 would have been considered a very low and scary position in the past, but this time, with the support of the national team, it took three and a half months to fall from 3174 points to 2784 points. This is the real version of boiling a frog in warm water. I would like to ask all the frog brothers, how does it feel in the pot? Is the water hot?

Looking at the K-line, there have been several positive line rebounds in the middle, but this step and three look back can easily lure people in, and also give some hesitant people hope. My suggestion is not to buy the bottom when it falls, and try again when it falls to the point where ghosts cry and wolves howl and the whole audience curses the sky and the earth.

Maybe with the intervention of the national team, such a scene will never happen. Maybe the subsequent script will also be a downward trend and a boiling frog. Well, never mind. If you miss it, you miss it. There is nothing to regret.

The Federal Reserve will cut interest rates in half a month, and China may follow suit, but it is hard to say how much stimulus this will have on A-shares. I have seen various analyses in the past two days saying that trillions of funds will return to A-shares, which seems a bit too optimistic. The capital market is all about expectations. If trillions of funds are about to return, then at least hundreds of billions of funds will be waiting in ambush now, and it will not be as bad as it is now.

Many readers asked where the decline would stop. Usually there is psychological support near the previous low point, but due to the partial rescue of the national team, the rhythm of each sector is different. The Science and Technology Innovation Board, ChiNext and small and medium-cap stocks have fallen to the low point in February, but the Shanghai Composite Index is still 5% away, which makes the situation difficult to judge.

……

Today, Bloomberg updated the news of the decline in domestic existing mortgage rates with more details, saying that financial regulators have proposed a two-step reduction of 80 basis points, or 0.8%, in interest rates. The first step may take place in the next few weeks, and the second step will take effect early next year. This reduction plan is valid for both the first and second sets.

I mentioned last night that last year's round of interest rate cut was 0.73%. What we need now is a round of cut of comparable magnitude to last year. The figure of 0.8% seems more reasonable.

The reason why the plan was not implemented immediately was to protect the banks' net interest margin. As of the end of June, the net interest margin of China's banking industry had dropped to a historic low of 1.54%, while maintaining reasonable profitability requires 1.8%.

That's basically it. I think it's very credible because we have both the objective conditions and the objective demand to lower interest rates. If the government doesn't lower them, the market will use all sorts of crooked ways to lower them, or else there will be a continuous wave of loan repayments. The best financial products of banks now only have a 2.5% return. How can you expect ordinary people to endure a 4-5% mortgage rate? If you have money but don't pay it back, you're just a fool.

On the other hand, an early reduction in interest rates will also help stabilize housing prices. As mentioned before, the rental-to-sale ratio and mortgage interest rates are moving in both directions. Now, after two years of decline, the rental-to-sale ratio of many houses is 2%. On the other hand, mortgage interest rates have also fallen to 2.8%. Therefore, as long as both sides work harder, they may successfully meet at around 2.4-2.5%.

……

1. Antitrust investigations have been upgraded, and Nvidia has received a subpoena from the U.S. Department of Justice. Affected by this, its stock price plummeted 9% yesterday, and nearly $300 billion in market value evaporated. Last night, a reader left a message asking if it was safe to buy Nvidia. If you dare to buy a stock as volatile as Nvidia, don’t worry about safety. Fortune and wealth are sought in danger.

2. Four shareholders sued Xu Xiang and Xu Changjiang, the former actual controllers of Wenfeng Shares, and demanded that they bear joint and several liability for compensation because Xu Xiang was previously arrested for manipulating the stock price, which led to the stock price falling. The most surprising thing about this incident was that Xu Xiang did not attend the trial, did not submit a defense opinion, and did not hire a lawyer. Therefore, the court made a judgment in absentia, and naturally Xu Xiang lost. With Xu Xiang's financial resources, it was not a big deal to hire a lawyer to deal with it. Of course, it may also be that he did not care about any verdict, after all, he was fined 11 billion when he was sentenced before.

3. Reuters reported during the day that the top 10 fund companies’ executives requested to return five years of excess compensation, but it seemed to be a wrong report. At night, I saw the media saying that the statistical caliber of deferred compensation was misreported. The money of the public fund industry is now deferred, that is, this year’s bonus will be paid in batches in the next few years. Faced with the wave of salary withdrawals in the past two years, many executives’ deferred money has been lost. In the past two years, the income of all financial industries has declined, including banks, insurance funds, trusts, and securities. No one can escape.

That's all. Oh, by the way, I saw Jiangsu also promote consumption subsidies this afternoon. It is estimated that the coastal provinces with more developed economies will also introduce similar policies. Some people say why there are no inland areas, it is unfair, why don't we wait and see? Of course, from a practical point of view, China's economic engine is in the coastal areas and some super cities, so it is useful to stimulate these areas. Inland areas originally rely on fiscal transfer payments, and the effect of issuing consumption coupons is also average. As for cash, forget it. Consumption coupons can drive consumption with a leverage of 5 times. The cash is sent back and deposited in the bank.

Deposits are the least favored now. If the interest rate drops, deposits will be bleed again.