There is no doubt that the price of BTC will depend on the macroeconomic situation and the changes in the macro situation within the crypto market. Therefore, for BTC, interest rates and market share will be important factors. Interest rates affect earnings expectations, while market share affects market capitalization.

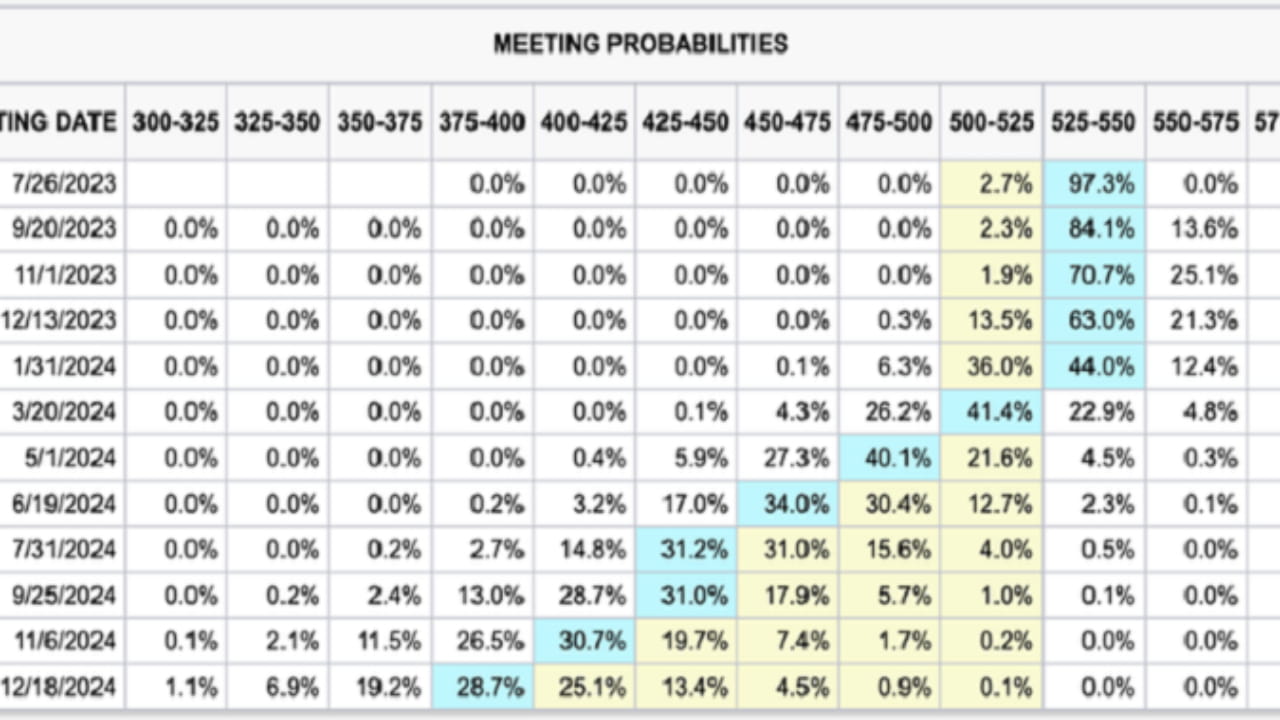

From the interest rate market, the Federal Reserve will not cut interest rates in the next six months; the European Central Bank will not show weakness under the threat of high inflation. The above situation means that high interest rates will continue to suppress BTC's performance. However, some potential positive factors are also supporting the price of BTC, such as the possible listing of BTC spot ETF.

In addition, the internal distribution of liquidity in the crypto market will also affect the price and market value of BTC. From the beginning of 2021 to the end of 2022, affected by the bull market and the "copycat season", BTC's market share gradually dropped from more than 60% to between 40% and 45%. Subsequently, benefiting from the institutional buying wave and the return of liquidity, BTC's market share began to rebound from January 2023. By July 2023, BTC's market share is about 50%.

Considering that the Federal Reserve is not expected to adopt the unlimited quantitative easing policy of 2020-2021 in the next few years, the change in the total market value of the crypto market due to expected changes will not exceed US$1 trillion.

Considering the current lack of external liquidity entering the crypto market, we assume that the future price of BTC depends entirely on changes in interest rates and market expectations, and is reflected in changes in market share.

With the high interest rate of 5.25% continuing and the lack of external liquidity, it will be difficult for the total market value of the crypto market to rise significantly before January 2024. Even if "expectations come first", under the most optimistic scenario, the expected increase in the internal market value of the crypto market will not exceed US$500 billion.

The total supply of BTC is approximately 19.43 million, and the total supply will not change significantly by more than 5% within a year.

Consider three simple cases

1. Investors have no more expectations, and the market value growth within the crypto market is limited. The total market value of the crypto market will stabilize between 1.2 trillion and 1.4 trillion US dollars, and BTC's market share will not change much, remaining at around 50%. This means that BTC's market value will fluctuate between 600 billion and 700 billion US dollars, and the price will fluctuate between 30,880 and 36,026 US dollars;

2. The BTC spot ETF was approved, bringing good expectations to investors. The market value of the crypto market rebounded to around 1.5 trillion to 1.6 trillion US dollars.

If BTC’s market share does not increase, BTC’s market value will stabilize at around $750 billion to $800 billion, and the highest price may reach $41,173; even if the rebound is not drastic enough, BTC’s price will be higher than $38,500;

If the spot ETF is approved and the market share of BTC rises to 60%, in the best case scenario, the market value of BTC will reach 960 billion US dollars, with a unit price of more than 49,400 US dollars; even if the overall crypto market rebounds not violently enough, the market value of BTC will rise to 900 billion US dollars, with a unit price of 46,300 US dollars.

3. The expectation of interest rate cuts combined with favorable expectations such as spot ETFs and Bitcoin halving have promoted the full return of liquidity in the crypto market, and the market value of the crypto market has rebounded to more than US$1.7 trillion.

- If BTC’s market share does not increase, BTC’s market capitalization will reach over $850 billion and the price will rebound to over $43,700;

-If BTC's market share rises to 60%, BTC's market value will reach more than 1.02 trillion US dollars and the price will reach around 52,500 US dollars.

In short, macro factors are relatively favorable for BTC, and the level that BTC prices can ultimately reach depends on interest rates and market expectations.

ETH: Application layer promotion

Considering that BTC has become the protagonist of the macro narrative, it may be wiser for ETH to focus on applications. Therefore, for ETH, the factors affecting its price mainly come from its own new narrative and whether it can be further widely used in the future. Since these factors will be reflected in the net income of the Ethereum network, we can reverse the possible price changes of ETH based on the changes in the price-to-earnings ratio.

Again, consider three simple cases:

1. The Cancun upgrade significantly increased the speed of Ethereum’s Layer 2 and reduced transaction costs, promoting the explosion of the Ethereum Layer 2 ecosystem. The Ethereum network's profit momentum continues, with quarterly revenue rising by 50% before the Cancun upgrade, and quarterly net income doubling after the Cancun upgrade.

Considering that ETH deflation will cause the total supply of ETH to drop to 120 million, the average price of ETH may exceed US$5,300 at the beginning of 2024 and exceed US$9,700 in the first quarter after the Cancun upgrade.

Assuming that investor expectations are more neutral, causing ETH's P/E ratio to fall back to around 150 (close to the level of comparable companies such as AMZN), in this scenario, the average price of ETH will reach around US$2,670 at the beginning of 2024 and approach US$4,900 in the first quarter after the Cancun upgrade.

2. The Ethereum network is relatively profitable, with revenue increasing by 25% each quarter. Revenue in the first quarter after the Cancun upgrade increased by 50% compared to Q4 2023.

Assuming that the ETH P/E ratio does not change significantly, investors' strong expectations will push the P/E ratio to remain around 300. Net income in Q2 of 2023 will be US$423 million, net income in Q3 will be US$529 million, and net income in Q4 will be US$661 million. Under this scenario, the total revenue of the ETH network in 2023 will reach US$1.739 billion, and the average price of ETH may exceed US$4,300 at the beginning of 2024, and exceed US$6,500 in the first quarter of 2024. If the P/E ratio falls back to around 150, ETH may average around $2,150 at the beginning of 2024 and exceed $3,200 in the first quarter of 2024.

3. The profitability of the Ethereum network has been decreasing marginally, with revenues increasing by 20% and 15% in Q3 and Q4 respectively. The benefits of the Cancun upgrade only curbed the trend of decreasing profitability in the first quarter.

Assuming that the ETH P/E ratio does not change significantly, investors' strong expectations will push the P/E ratio to remain around 300. Net income in Q2 of 2023 will be US$423 million, net income in Q3 will be US$508 million, and net income in Q4 will be US$584 million. Under this scenario, the total revenue of the ETH network in 2023 will reach US$1.641 billion, and the average price of ETH may exceed US$4,100 at the beginning of 2024, and exceed US$5,400 in the first quarter of 2024. If the P/E ratio falls back to around 150, ETH may average around $2,050 at the beginning of 2024 and exceed $2,700 in the first quarter of 2024.

In summary, the development of ETH is highly correlated with its own profitability. The combination of narrative support and sustainable and growing profitability is the key to driving the price of ETH up - which is completely different from BTC.

As the correlation between currencies continues to weaken, the analysis logic and trading strategies that were previously fully or partially reusable are no longer effective. Paired trading no longer shows the ideal correlation regression, and the general investment framework based on market capitalization and track is no longer applicable to some extent - this means that further analysis based on the fundamentals of the project itself becomes more important.

It is time to adopt two or even more completely different logics to look at the crypto market. Crypto 3.0 has arrived; the times are moving forward. Bitcoin will be more closely integrated with the macroeconomy and traditional markets, while Ethereum needs to become a "great company"; other cryptocurrencies must also take their own paths. In the crypto market where both the macro and micro structures are changing rapidly, we need to keep up with the times.

Later, I will bring you analysis of leading projects in other tracks. If you are interested, you can click to follow. I will also organize some cutting-edge consulting and project reviews from time to time. Welcome all like-minded people in the cryptocurrency circle to explore together. If you have any questions, you can comment or send a private message