Note: This may not be correct, please correct me. It does not represent any investment advice.

——I don’t like vague positions, but I also doubt overly certain answers (Xu Zhiyuan)

Follow us on Twitter @deepbluuest

Concepts to know

AMM: Automated Market Maker

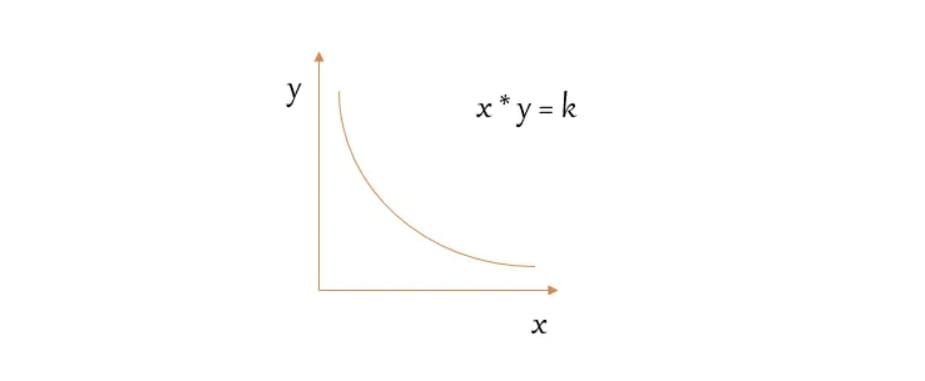

xy=k: Constant product algorithm

Liquidity pool: The pool of assets where tokens are stored. Pool is a figurative explanation, similar to a capital pool.

LP liquidity provider: a user who puts tokens into the liquidity pool to increase the liquidity of the pool, and the reward is part of the transaction fee

Uniswap V1 and the first generation of AMMs

The core of the first generation AMM is x*y=k. Keep k unchanged. x and y are two different assets, that is, the total asset size of the pool remains unchanged.

🔵Now assume that the liquidity of a pool is 20AVAX and 2000USDT, and the price of AVAX is 100USDT

🔵k=200*2000=40000

🔵When liquidity does not change, the k value remains unchanged

🔵When we need to sell 5 AVAX, y=k/x, then y=AVAX in the pool will become 20+5=25

🔵If k remains unchanged, then x=k/y, which is 40000/25=1600USDT

🔵Currently, we sold 5 AVAX and we received 400USDT

🔵The pool originally had 20 AVAX and 2000 USDT, and now there are 25 AVAX and 1600 USDT left

But originally we found that the price of the pool was 1:1, so what’s the problem?

The problem is actually the impact of price. When we sold the first AVAX, the price changed.

Another problem is that liquidity is actually distributed overall among all parts, but the reality is that the extreme prices at both ends are almost never reached, which actually reduces the liquidity in the correct trading price area. Reduced liquidity means greater price volatility and slippage, wasting liquidity.

Summarize:

1. It will never happen that one asset x or y is completely depleted, but it will approach 0

2. Liquidity is evenly distributed, resulting in waste at both ends

3. Price impact is strictly related to pool depth

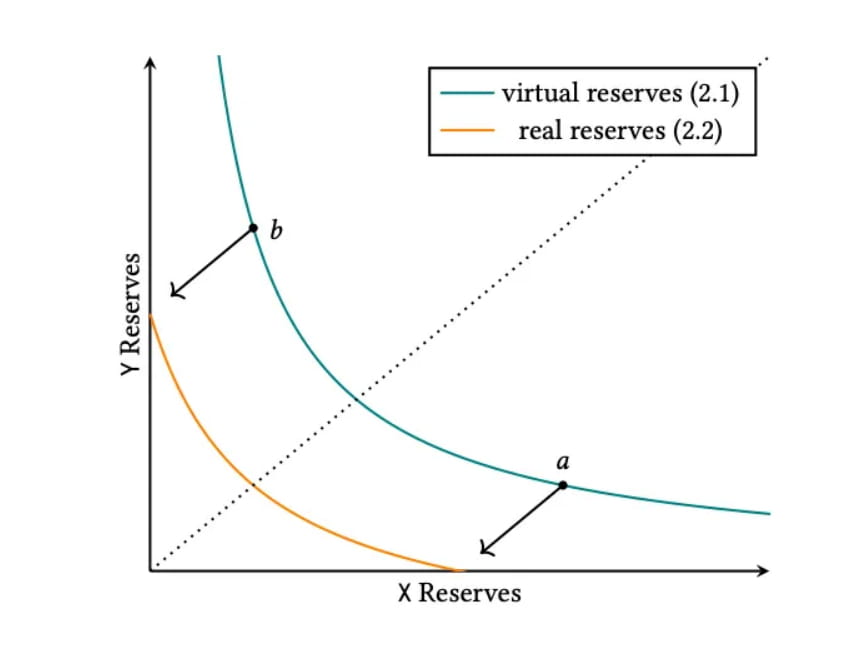

Uniswap V3

The main idea of Uniswap V3 is to pool liquidity.

For example, for a stablecoin liquidity pool like USDC/USDT, the price is most efficient at around 1:1, so the rest can be said to be a waste.

V3 therefore introduced the concept of liquidity range, which allows us to provide liquidity within any range.

The formula is as follows, but there is actually no need to understand the formula, just look at the picture.

The blue line is the curve of the first-generation AMM, and the yellow line represents the liquidity situation in the price range [a,b].

We can see a situation where there is a single asset of 0 in the yellow line, where it connects with the coordinate system.

But there are two things to note when providing liquidity:

1. LP can only choose two price levels (ticks) when depositing liquidity, and assets can only be evenly distributed

2. Liquidity provision certificates are provided in the form of NFT

In general, the centralized liquidity solution brought by V3 is great and can greatly solve the liquidity problem, but the problems that still exist are active management and composability. Since more currencies are not traded between stablecoins, it is still difficult for ordinary users to determine a suitable price. This has led to the birth of many protocols that make a living from this, such as Arrakis. Another aspect is that NFT as a voucher has caused the composability between Defi to lose some of its function.

By the way, let me mention DYDX's order book system. The order book brings an operating experience close to that of CEX and can support stop-loss and take-profit orders. But at the same time, since all requests on the chain need to be signed by the wallet, DYDX hands this part off-chain. In other words, the assets are transferred to the dydx address in advance. In the blockchain, every additional step of asset custody brings an additional step of risk.

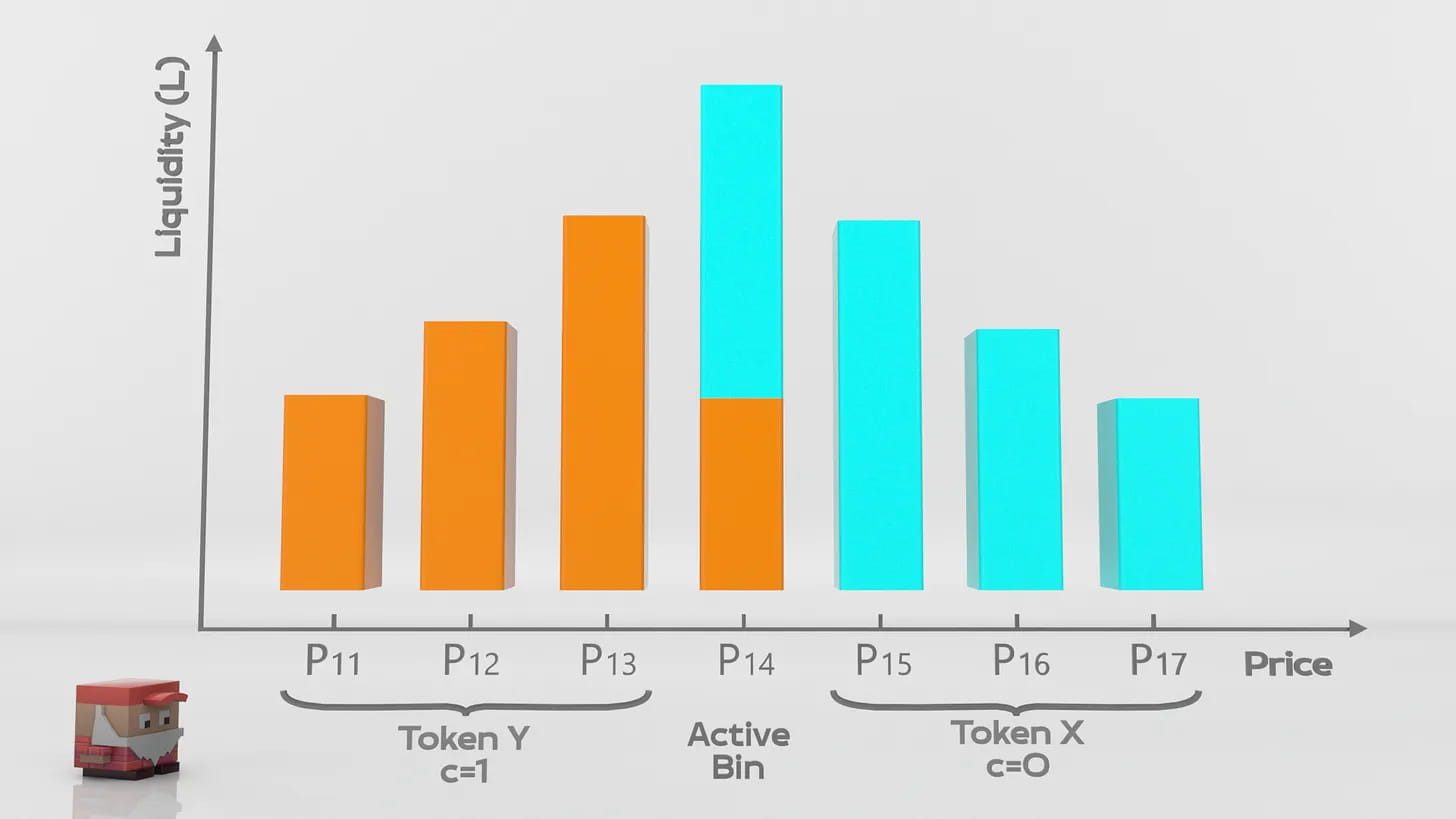

JOE is a spot DEX on Avalanche, and later launched NFT trading, Launchpad, lending, etc. Recently, JOE announced that it will bring a new liquidity method, Liquidity book.

Liquidity Book

Liquidity Book is translated as Liquidity Book, which sounds like a combination of liquidity mechanism and order book system, but it is actually quite different. (hereinafter referred to as LB)

However, LB has brought several new changes compared to V3.

1. The price range is more vertical

2. Defi can be combined and strengthened

3. Determine fees by measuring price fluctuations

In LB, LP deposits liquidity into different price bins, each of which has a specific fixed price. LP can provide liquidity to multiple price bins at the same time.

LP receives FT instead of NFT. The advantage of FT is that it has higher liquidity and can be combined with more DeFi protocols.

LB aggregates each liquidity warehouse to form a large liquidity pool. Individually, a small liquidity warehouse can also be understood as a separate liquidity pool.

In the liquidity warehouse, the transaction prices are fixed, that is to say.

Assuming the current liquidity warehouse pricing is 1AVAX = 100USDT, the total liquidity is 1000U: 100AVAX

Then within the range, 900 USDT can be exchanged for 90 AVAX without any price fluctuations.

When the liquidity of the latest position is exhausted, the next position will automatically fill it, which means that price fluctuations only occur when positions are switched.

Surge Pricing

Generally, AMM charges a uniform fee for transactions.

LB has enabled dynamic fee deconstruction, similar to ETH's EIP 1559 proposal, which divides the handling fee into basic fee and dynamic fee. The basic fee is the minimum handling fee, and the dynamic fee is determined according to market volatility. The higher the volatility, the higher the dynamic fee.

In stablecoin exchanges, due to the small volatility, the transaction slippage caused by LB should be very low.

Impermanent loss problem

In general AMMs, once the asset prices in the liquidity pool deviate, impermanent losses will occur.

Impermanent loss is essentially the cost of price discovery, that is, the cost incurred by the market to determine the price of the token.

From this perspective, the higher the market volatility, the higher the impermanent loss because the market needs to consume more to determine the price.

LB's impermanent loss benefits from the dynamic fee structure. The greater the volatility, the higher the dynamic fee, which is equivalent to charging additional fees to compensate LP's impermanent loss.

VA Volatility Accumulator

VA is a mechanism that does not rely on any oracle and can calculate the instantaneous volatility of each liquidity pool. The dynamic fee is determined by the value of VA. Simply put, VA is equivalent to calculating the number of changes between each position, because LB is essentially composed of liquidity warehouses, and the price in a single liquidity warehouse remains unchanged, so calculating the change in the liquidity warehouse can determine the volatility.

Summarize:

JOE's LB mechanism is based on Uniswap V3, which optimizes the freedom of choice of LP market making, regulates the problem of impermanent loss through dynamic pricing, and issues LP certificates in FT mode. For V3, these are not revolutionary innovations, because the market is aware of most of the problems and has provided solutions, but they are not direct and efficient enough.

To see how much change it can bring, we need to verify it by looking at some data after JOE goes online.