1. Unprecedented Tech Bull After the epidemic concerns faded in the second half of 2020, the Federal Reserve still promised to maintain zero interest rates for a long time, quantitative easing continued, and inflation was nowhere to be seen. The world ushered in a financing boom for technology companies. The rapid growth of startup loans and venture capital quotas has accumulated a large amount of cash and deposits in the hands of technology startups, and these deposits have largely flowed into Silicon Valley Bank (hereinafter referred to as SVB), the most important bank in Silicon Valley and one of the top 20 banks in the United States. In the one and a half years from June 2020 to December 2021, SVB's deposits rose from US$76 billion to more than US$190 billion, an increase of nearly 2 times (Figure 1).

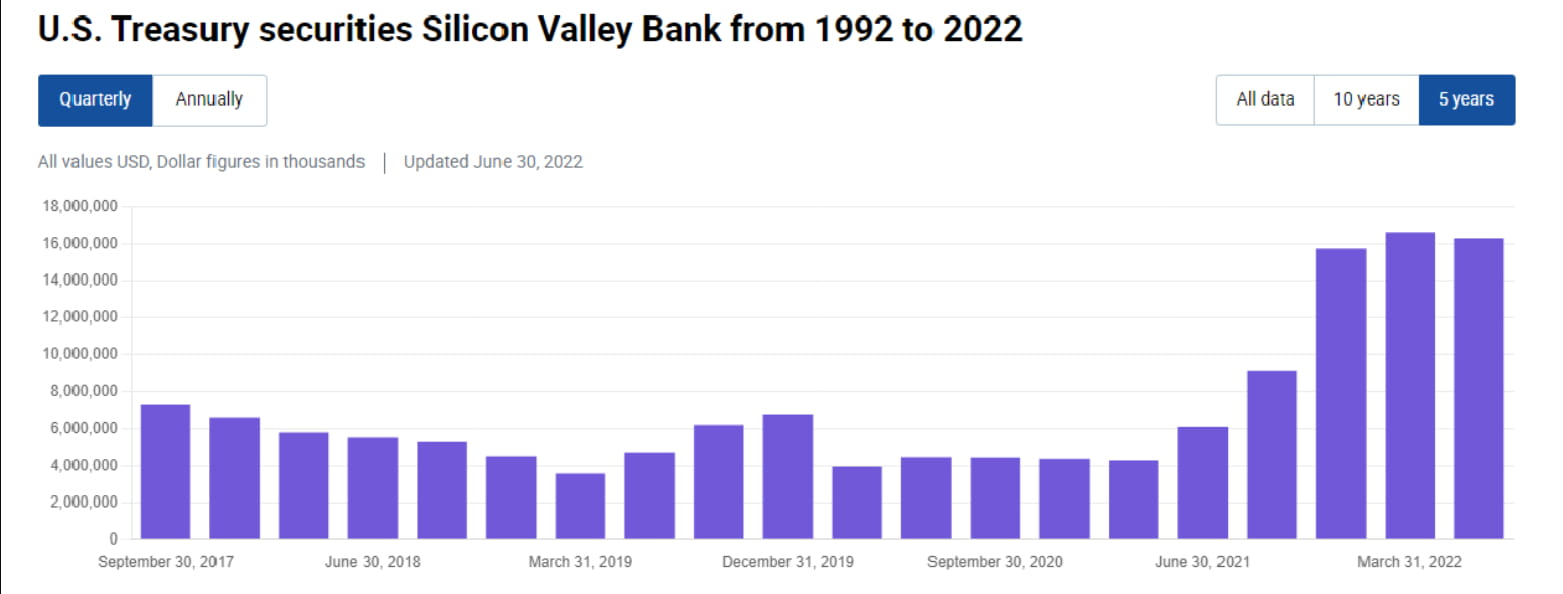

2. "Buy with your eyes closed" Faced with a large inflow of funds on the liability side, SVB's investable funds on the asset side also rose rapidly. The Federal Reserve has not started to raise interest rates in 2020-2021. If the money is left in the Federal Reserve's reserve account, the annualized interest rate is only a pitiful 0.1%. SVB's choice is to buy a large amount of US Treasury bonds and MBS. From its 10-Q, from mid-2020 to the end of 2021, SVB increased its holdings of US Treasury bonds by 12 billion, and its holdings increased from 4 billion to 16 billion (Figure 2). More importantly, SVB increased its holdings of MBS by about 80 billion US dollars, and its holdings increased from more than 20 billion to 100 billion (Figure 3). What does this mean? SVB's total assets are about 200 billion US dollars, which means that half of its assets are allocated to MBS, or it is believed that it has allocated 70% of the more than 110 billion deposits that have flowed in from 2020 to 2021 to MBS. This is almost unbelievable, even ridiculous, for a commercial bank whose main business is lending.

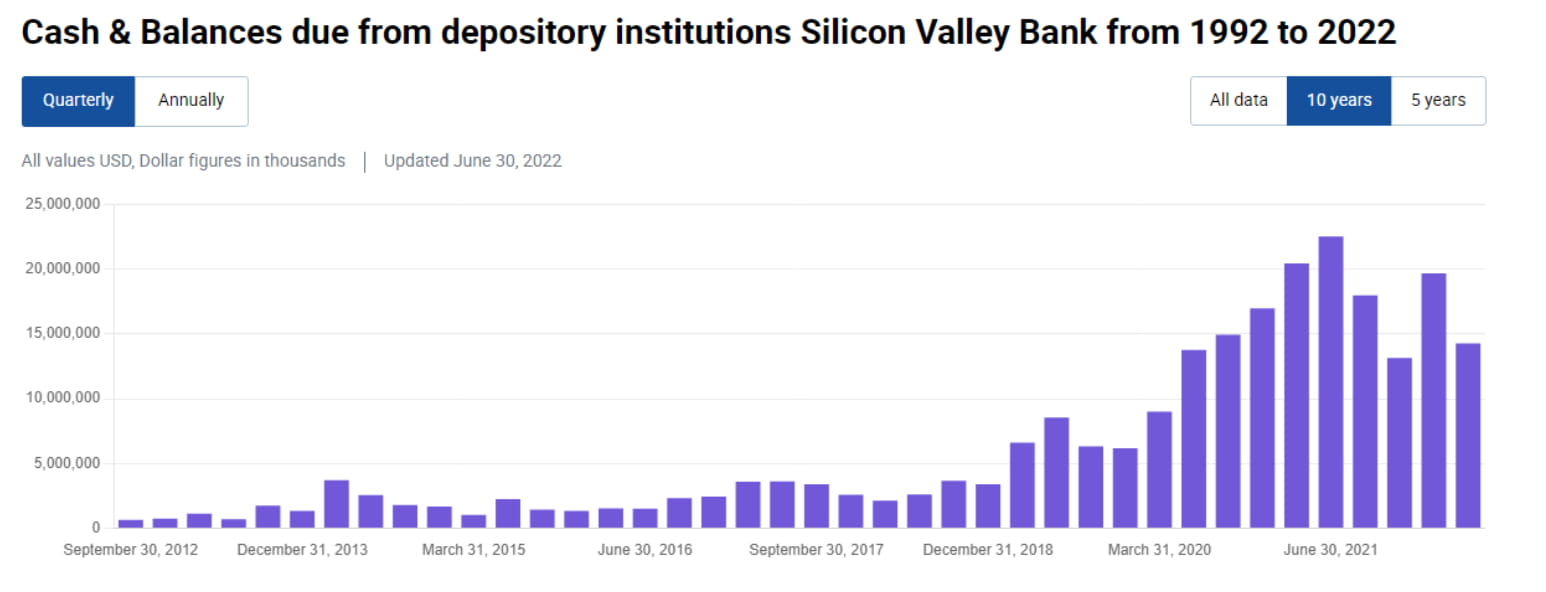

3. "Cash is garbage" Compared with the crazy increase in MBS holdings, the growth of SVB's cash and cash equivalents (including reserves, repurchases, and short-term debt) on hand is not obvious. From mid-2020 to mid-2021, it only increased from 14 billion to 22 billion, and even fell to 13 billion by the end of 2021, even lower than the level in mid-2020 (Figure 4). This reflects that while SVB aggressively allocates long-term assets, it has not reserved sufficient cash in proportion to cope with deposit outflows.

4. "Sound" accounting treatment We know that commercial banks mostly use available for sale (AFS) and held to maturity (HTM) for accounting treatment when buying fixed-income products. SVB is no exception. Its 16 billion U.S. Treasury bonds are fully measured in AFS, while its 100 billion MBS are mainly measured in HTM (Figure 5). The advantage of AFS and HTM is that the fluctuation of asset market value (MTM) will not be directly reflected in profit and loss, and at most it will affect the unrealized gains and losses under other comprehensive income (OCI), and it can be reversed. But the disadvantage is that once forced to sell AFS and HTM, a profit or loss needs to be recognized in the current period.

5. Fed's interest rate hikes and unrealized losses Since SVB's asset purchases were concentrated in the low interest rate period of 2020-2021, the average yields of AFS and HTM assets were very low. From the 10-K, the average yield of its AFS was only 1.49%, and the average yield of HTM was only 1.91% (Figure 6). With the Fed's rapid interest rate hikes in 2022, the AFS assets purchased during these low interest rate periods brought SVB more than $2.5 billion in unrealized losses (Figure 7) in 2022. If the unrealized losses of 100 billion MBS measured in HTM are taken into account, the total unrealized losses are as high as $17.5 billion (HTM unrealized losses are approximately $15 billion, Figure 8).

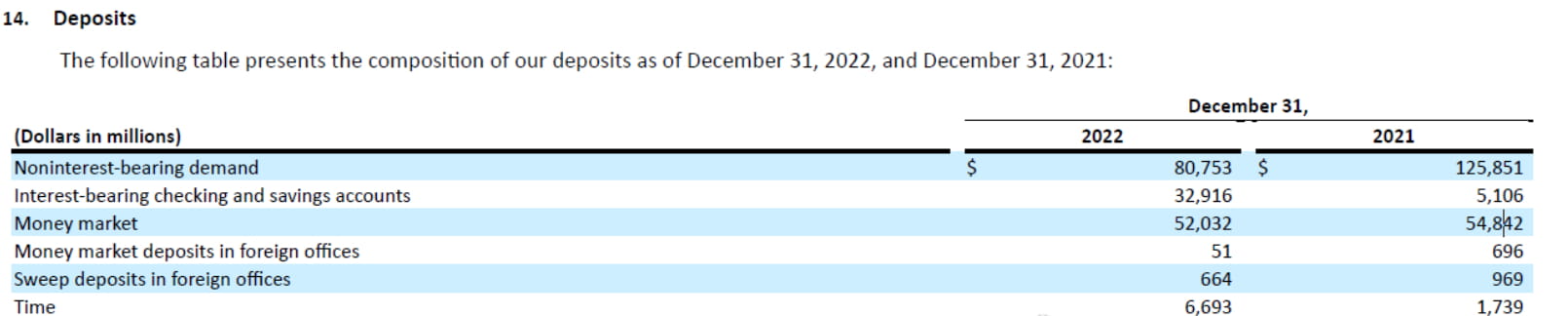

6. Deposit outflow As long as you don't sell these unrealized losses, they will not become losses, so they are often regarded as "floating losses are not losses." The problem is that the rapid interest rate hikes by the Federal Reserve in 2022 have caused a hard time for global technology startups. They cannot raise funds and their stock prices have been falling, but research and development have to continue, so they can only continue to consume their deposits in SVB. Coupled with factors such as the Fed's balance sheet reduction, SVB's deposits have been flowing out since they peaked in March 2022. The total amount of deposits in 2022 fell by 16 billion, accounting for about 10% of the total deposits, especially the interest-free demand deposits dropped sharply from 126 billion to 81 billion, greatly increasing the pressure on interest expenses on the liability side (Figure 9).

7. Negative convexity of MBS In particular, when interest rates rise, residents are willing to slowly change their loans rather than repay them in advance, so the duration of MBS will be extended, which leads to the duration of a large number of HTM MBS held by SVB becoming longer and longer, making it increasingly difficult to cope with the continuous outflow of funds on the liability side. Therefore, since the end of last year, SVB has faced such a situation: there are a lot of floating losses on the asset side MBS, which will not mature for a while, and the cash reserves are not sufficient; deposits on the liability side have been flowing out, and the cost of liabilities continues to rise.

8. Cutting off one's own arm? SVB's management actually has some other options, such as borrowing repo from the interbank market, borrowing advance from FHLBs, or issuing bonds to meet the pressure of deposit outflow. But there are two problems. First, the current interest rate curve is seriously inverted, and the cost of borrowing on the short end is much higher than that on the long end. Instead of borrowing on the short end to maintain the long end until maturity, it is better to cut the position directly and the loss will be smaller. Second, it is unlikely that the deposits of start-ups will flow back after they flow out. Therefore, instead of using short-term loans for emergencies, it is better to cut positions directly to reduce leverage - although this will cause a sharp drop in stock prices in the short term, it is actually the safest behavior in the long run. In this environment, the short-term pain of cutting off one's own arm may be the best choice.

9. Panic When SVB announced that it had sold $21 billion of AFS assets and incurred a loss of $1.8 billion, the market panic was actually reflected in several aspects. First, will the $15 billion unrealized loss corresponding to the $100 billion of HTM assets that have not yet been sold become a real loss? You know, the total market value of SVB's stock is only less than $20 billion. Second, issuing a large number of shares will dilute the rights and interests of existing shareholders, which is itself a negative. Third, most of SVB's customers are technology companies, so they are not covered by deposit insurance and are prone to bank runs. Many executives of technology companies have expressed their intention to withdraw all funds from SVB in the past 12 hours. Fourth, the market is unclear whether other banks with large exposure to technology companies will suffer bank runs, and whether this crisis will spread.

10. Outlook The development of this incident depends on many factors, such as whether SVB will encounter a more serious run or even go bankrupt? In the next few days, we can observe the evolution of the crisis from at least two levels. One is whether the interbank market and repo market will worry about the overall financial situation of small and medium-sized banks? Will there be a local liquidity crunch? Observe whether the levels of EFFR and SOFR 99% will rise sharply in the next few days. Another is to observe how the market will view the risks of loans/assets related to technology companies, such as whether banks with large exposure to technology companies will face a more serious run? 99% of the panic about banks is FUD (blind panic), but the remaining 1% of the panic that comes true often turns into a financial crisis with huge lethality. Let the bullets fly for a while.