Huma Finance has recently sparked heated discussions in the cryptocurrency circle due to the launch of its 2.0 PayFi (payment financing) model. Some users question whether its operations differ from traditional P2P lending, worrying that its capital pool may contain high risks. On the other hand, supporters emphasize that Huma only serves licensed financial institutions, has a robust risk control mechanism, and is fundamentally different from P2P.

(From straight lines to curves, how Huma Finance 2.0 combines revenue incentives to create cross-border payment solutions)

P2P rebranding? Analyzing Huma's PayFi business model.

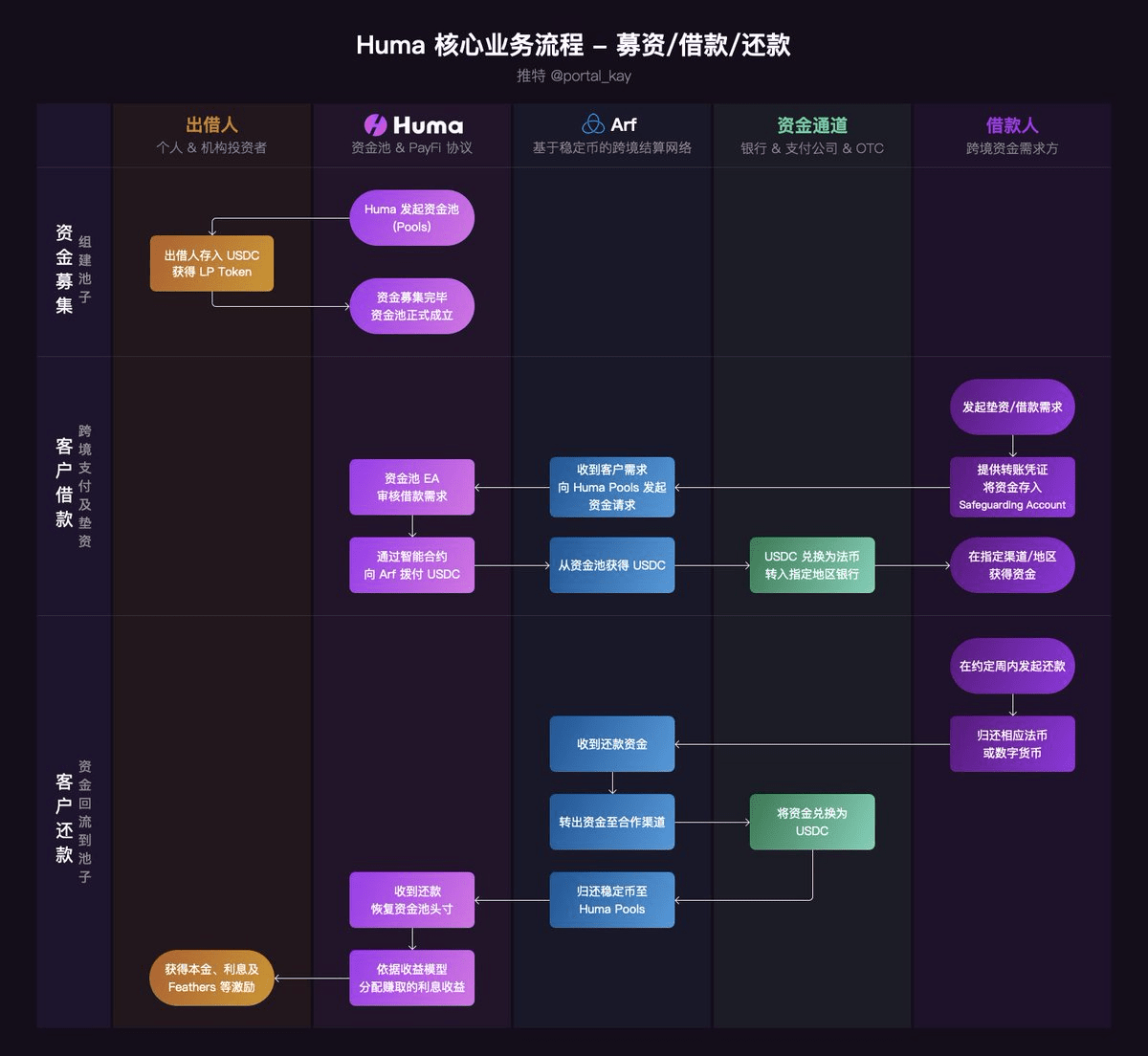

Huma Finance claims to be the first PayFi protocol, dedicated to providing immediate liquidity for global cross-border payments. PayFi researcher @portal_kay explains its operation as follows:

Investors deposit USDC stablecoins into the Huma capital pool → The cross-border settlement network Arf borrows funds from the capital pool and advances them to licensed financial institutions needing cross-border payments → The financial institution completes the payment and repays within an agreed timeframe → Funds flow back to the capital pool, distributing profits to investors based on the revenue model.

Huma emphasizes that its clients are all compliant licensed financial institutions, not ordinary individual borrowers, with the goal of creating a high-transparent and sustainable global financial ecosystem.

User discussion focus: Is this really 'new finance'?

Controversial viewpoint: Is this just rebranded P2P?

A few days ago, X platform user @0x0xFeng pointed out: 'Huma is just rebranded P2P; high interest rates can only attract low-quality clients, posing extreme risks and will eventually blow up.'

He emphasized that its 'capital pool' is essentially similar to past Chinese P2P models, questioning its sustainability.

Supporters respond: Borrowers are trustworthy, not P2P.

In contrast, supporters like @portal_kay and @jcmeowjc believe that Huma's borrowers are licensed financial institutions, not individuals or SMEs; and they have undergone KYC or KYB reviews with appropriate structured risk control mechanisms.

Huma and traditional P2P: Five key differences.

Analysis of the capital pool's security: Can data and risk control persuade the market?

Additionally, @portal_kay has also analyzed from a data perspective, delving into what advantages and risks Huma has.

Advantages: Strict risk control discipline, transparent data.

Arf has processed approximately $3.914 billion in funds, a massive amount.

Operating for 883 days without any bad debts, with a default rate of 0%.

Introducing 'First Loss Cover' and 'Tranches' risk control designs.

Potential risks: non-principal guaranteed, financial institutions still face default risks.

Non-bank deposits, thus no government guarantee.

In the unfortunate event of default, the maximum compensation amount is only '100 USD.'

The potential risk of partner financial institutions or banks going bankrupt still exists.

The founder personally addresses the differences between PayFi and traditional financing.

In response to external doubts, Huma's founder also personally replied, emphasizing that its product belongs to 'payment transaction financing,' fundamentally different from traditional financing.

He emphasized that 'the essence of Invoice Financing is accounts receivable; the counterparty may have accounts but not necessarily cash. There is uncertainty about whether the borrower will make timely payments, which poses a higher risk; what we do is Payment Transaction Financing.'

The money has already entered the financial system; it just hasn't 'reached its destination' yet, and the risk is relatively lower.

The founder describes its service as 'email' replacing traditional mail, 'simplifying the payment process that originally required multiple layers of bank clearing systems to directly reach the destination via on-chain USDC, achieving real-time settlement.'

We only need to ensure that the funds from the remitter are locked in safeguarding or other custodian accounts; with our legal claim, we can safely complete this payment.

This risk control approach keeps risks at a level where 'fiat currency already exists, only the speed of channels is lacking,' which somewhat reduces systemic risk and highlights its different foundational logic from traditional P2P.

Is it a revolution or a risk? The market will provide the answer.

In summary, Huma Finance's PayFi model has key differences from traditional P2P, especially in terms of the target clientele and risk control mechanisms, which are becoming more institutionalized and professional. However, its 'capital pool + non-guaranteed' characteristics still evoke memories of the historical shadows of Chinese P2P. Whether it can achieve global payment financing innovation in the future remains to be tested by the market and time.

As @portal_kay said: 'Whether to invest depends on whether you can accept the volatility of medium-low risk products and regulatory gray areas.'

This article on Huma Finance has gone viral and sparked controversy: is the new PayFi model merely a rebranded P2P? It first appeared in Chain News ABMedia.