CC found that many friends still encountered freezing or the bank called to say abnormal... They didn't know how to deal with it, and even heard this and began to be unable to extricate themselves from the pit. The following is the most complete withdrawal and deposit rules, please take a look! !

What behaviors caused the bank to close down?

●Dozens of people from all over the country transfer money to you every day, and after you receive it, you transfer it out again. (The payment card triggers decentralized transfers in, and centralized transfers out risk control)

●You received a large remittance and transferred it to dozens of people in different parts of the country within a few minutes. (Payment cards trigger centralized transfers and decentralized transfers)

● You're afraid of freezing, so every time before receiving money, you send a small red envelope to test the card. (Triggering small transactions before large ones to test risk control)

● Online gambling deposits, purchasing virtual currency. (If the other party's account has case-related risks, you will be warned in reverse)

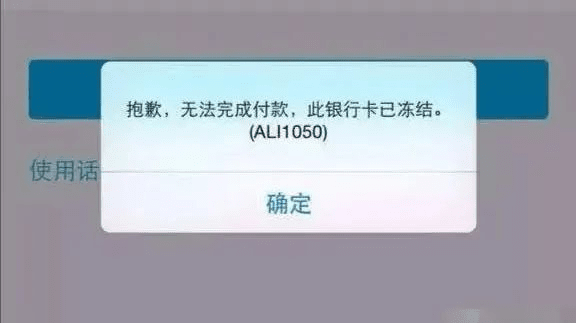

● Received unknown funds, judicial freeze for three days (bank high-risk list)

● There are 5 cards under your name listed on the authority's investigation platform. (Listed on the bank's high-risk list)

● Frequent large cash withdrawals (such as late-night withdrawals)

● Frequent quick in and out...

The highest risk behavior with a bank card is receiving funds from strangers: keep this in mind and you definitely won't face risk control or card freezing.

If frozen, you can see my previous article on the steps for unfreezing: https://app.binance.com/uni-qr/cart/17058592135410?r=1011176604&l=zh-CN&uco=8qUggAMDint8_SyNDc_tVQ&uc=app_square_share_link&us=copylink

You must make sure to follow these points to prevent your card from being controlled. Key points:

1: Try not to make deposits or withdrawals too early or too late, avoid frequent quick transactions; if you're not in a hurry after the deposit, you must leave it overnight to count as valid flow (very important);

2: Don't have large amounts of deposits and withdrawals on the same card. If you have several cards, use them separately to reduce the usage frequency of a single card.

3: If you need to repay loans or credit cards, try to use your own account for repayments (the bank restricts repayments from different names);

4: Bind your savings card to WeChat, Alipay, JD.com, etc., for quick consumption. Use them when possible to increase diversified consumption (the bank likes this);

5: Use WeChat Wallet and Alipay's Yu'e Bao (enable scheduled transfer function), transfer about 10-100 yuan daily with a savings card. If you have multiple cards, set different cards for transfers each day (increase diversified consumption), or use the fixed investment function, so you won't need to test which bank card is frozen. You'll know the status of each card every day. This operation is generally done by currency merchants, also avoiding small tests before large deposits.

6: Make sure to write notes for each income or expenditure and keep corresponding proof. Absolutely do not accept funds from strangers. If transferring money to strangers, make sure to write a note.

7: Salary cards, mortgage cards (important cards) absolutely must not be linked to other cards or bound to any unknown apps.

How to handle the aftermath of unfreezing a bank card?

Sometimes, the deputy bank president or risk control manager can be very arrogant. They might ignore you and send you directly to the anti-fraud center for a stamp. Many people don’t understand and foolishly run to the anti-fraud center, only to find they can't even get in. The anti-fraud center doesn’t accept private business; this is the bank passing the buck.

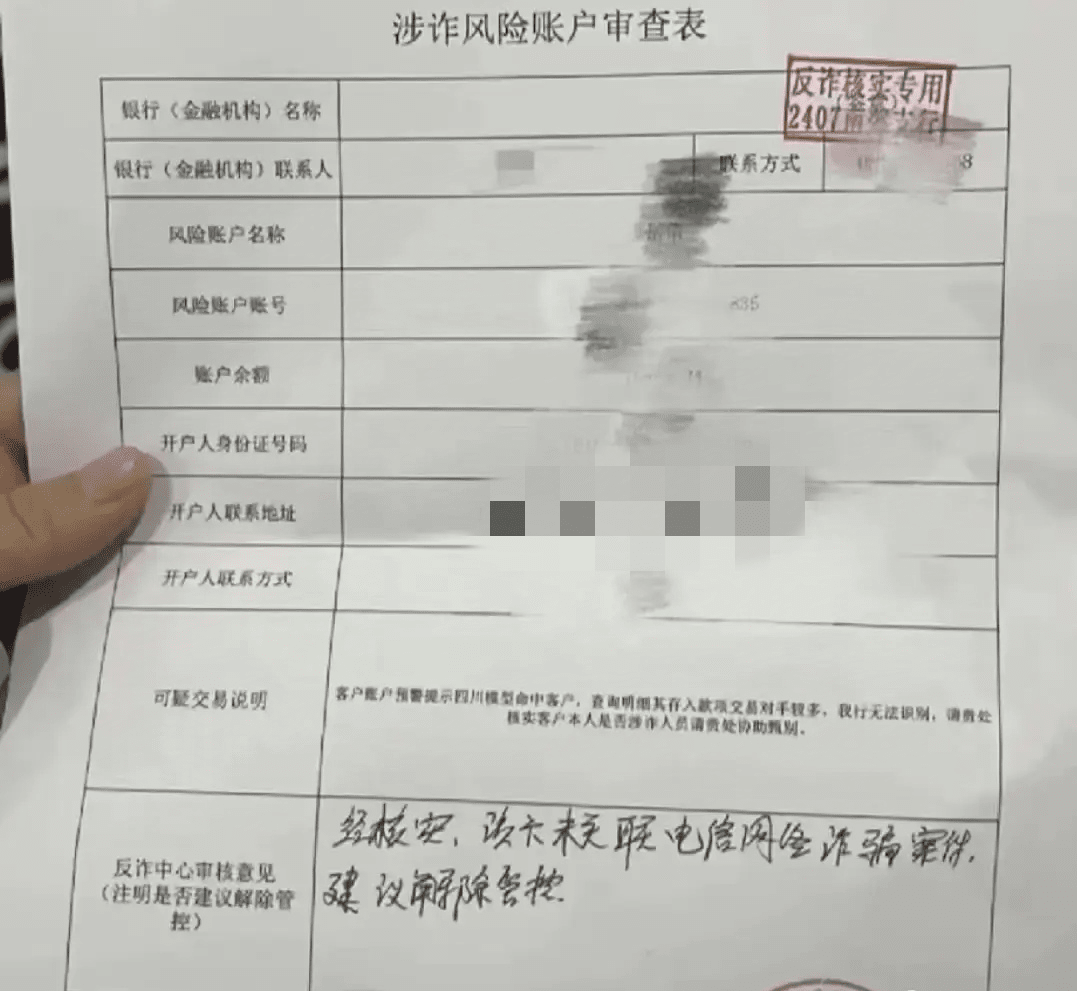

The process for getting a stamp from the anti-fraud center is: you ask the bank to issue (Fraud Risk Account Review Form), which the bank must provide, but they won't give it to you directly. Instead, the bank connects with the anti-fraud staff and sends it to the anti-fraud center in a public-to-public manner or takes you there to deliver it.

So in many cases, we stand tall no matter what we do! If you're timid, whether you have little money or a lot in your account, when you try to lift risk control, the bank staff won't help you withdraw or conduct other transactions, citing things like overall control from the head office to brush you off, impatiently telling you to go find the anti-fraud center for a stamp. This is all about catering to the individual!

Experienced bank staff will tell you: come to the bank to print a transaction history to see if there are any abnormalities. This is their way of breaking the code. If you enter your password to print the transaction history, you have authorized it.

So you need to use your wits; I don’t know what’s abnormal in my transaction history. You tell me where my transaction history is abnormal. If he brings out a transaction slip for you to explain, that’s illegal. (A bank staff or customer service manager speaking to you face to face)

The bank is a commercial institution and does not have the authority to freeze your bank card or prevent you from withdrawing money. There’s a BUG here! A massive BUG! Bank staff cannot view your transaction information without your authorization.

Client card balances and transaction details are classified as privacy levels; no one can view them alone. If viewing is needed, it must be authorized by senior personnel.

So, when your card is abnormal, it definitely has abnormal transaction flows, and if the bank staff directly control you without due diligence, that's the first bug. Why do they dare to control you? Because they privately looked at your transaction history, that's the second violation and the second bug.

So, if he tries to deceive you or act recklessly, you must fight back. How to fight back? First, you need to get evidence that he looked at your transaction history privately. For example, if he asks you about a specific transaction during due diligence, that proves he checked your transaction history privately.

Most bank accounts, once unfrozen, the bank avoids liability. Even if an uncle in another location unfroze it, they will ask you to get a stamp from the anti-fraud uncle before they lift the control; this is actually a violation.

In summary, when the judicial authorities have ruled out any case-related suspicions and unfreeze the bank card, the bank has no reason or legal basis to impose restrictions. 🌰XX Bank illegally restricts citizens' property and freedom to withdraw funds; only judicial authorities have the right to freeze citizens' property, and banks do not have the right to endlessly restrict one's access to funds. The request is to lift this account's bank restrictions for actively handling associated accounts under other case-related accounts❗❗

Will you get beaten up after saying this? Don't worry, the bank will call you, 'Big brother, is there anything to discuss...'

So, when you're out and about, your identity is given by yourself. (If they deceive you, you can also deceive them, saying you'll transfer private bank-level funds next month), that's two different things.

Ever go to the bank to lift controls and no one pays attention to you?

🌰 Go photoshop some assets from another bank to show him, and he’ll definitely grovel to you. Fake banking apps on Taobao only cost a few bucks.

First, apply to open a private bank account; won't he be groveling to you then? In a small community, there aren't many private bank-level clients. Then go to the jurisdiction to handle a business account for payroll; someone will look down on you.

CC hopes this article can help you. Brothers and sisters, give a thumbs up and follow!