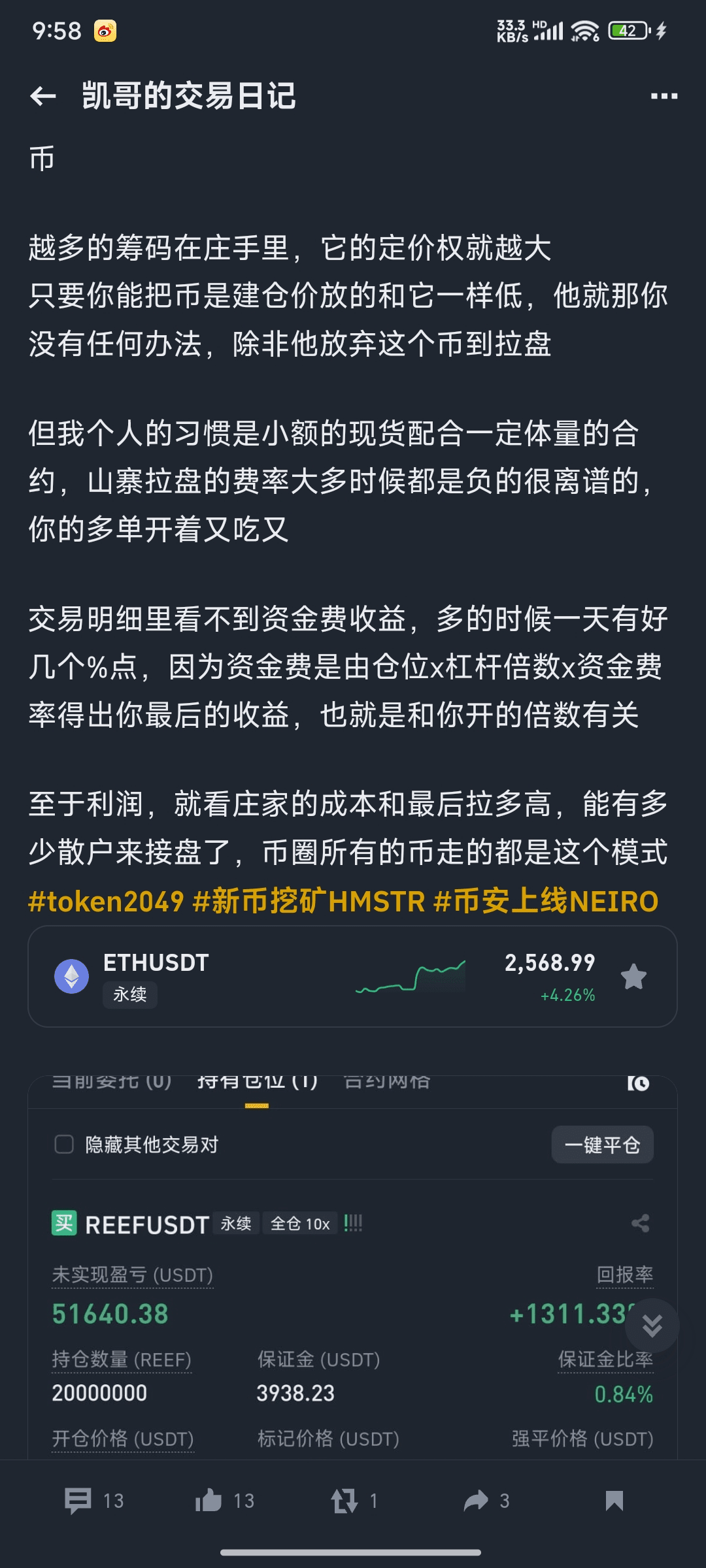

This was my analysis of reef at the time, but I didn’t hold on to it for long.

This is also a mistake. You can read the explanation below. Why is the funding rate negative for a long time? It is because many people do not understand the funding rate well enough.

The gameplay of negative funding rate will be very interesting; negative funding rate generally has to wait until it is full before there will be a better reference value. The funding rate at full capacity will be different for different alts, with the lowest being -1.5%. If the premium continues, it will continue to upgrade to -2%, -2.5%, -3%; the more common situation is that the full capacity negative funding rate of most alts is -2%, but recently because of the obvious manipulation of the market makers in some alts, Binance has adjusted the full capacity negative funding rate of these alts to -3%

Having said so much common sense, how does the full funding rate guide trading? Let's take a look at how the full funding rate is generated and what happened in the market that caused the full funding rate. As mentioned earlier, Binance's funding rate calculation formula is the most reasonable among all exchanges, that is, it is calculated by depth weighting and time weighting. I will post the premium index formula below to facilitate your understanding:

Premium Index = [Max (0, Impact Buyer Bid - Spot Index Price) -Max (0, Spot Index Price - Impact Seller Bid)] / Spot Index Price

First of all, the pull of the copycat must be initiated by the spot market (it is absolutely impossible to be initiated by the contract), and then the contract cooperates, and the dealer will inevitably make arrangements in both the spot market and the contract market; because the spot market requires real coins to buy and sell, while the contract market does not, it only needs to anchor the spot market through the contract system, so once there is a substantial increase, it is basically inevitable that the price in the spot order book will be higher than the price in the contract order book. At this time, the first value in the premium index is:

Max (0, impact bid price - spot index price), it will always be 0, because the impact bid price - spot index price is negative, the value of Max (0, negative number) is zero, then the second value that affects the premium index is: Max (0, spot index price - impact bid price) will take the value of spot index price - impact bid price

I don't know if you have had an epiphany yet. That is, when the funding rate is negative, the calculation of the negative funding rate is completely affected by the market sell orders. At this time, the larger the market sell orders, the faster the funding rate will be negative. But this does not mean that there are few buy orders in the contract market. Many people think that when the funding rate is negative, there are a lot of people shorting. In fact, there will be an equal number of long orders for every short order in the contract market. The negative funding rate does not mean that a large number of people are shorting, but that the spot market and the contract market have a high premium. This high premium is the essential reason for the negative funding rate. It is not because of a large number of people shorting that the full funding rate is caused. If you can fully understand this at this time, congratulations, you have surpassed 90% of the people in the contract market. Now that you know the nature of the full negative funding rate, how can you use this feature to trade? I just mentioned that the essence of the full funding rate is the high premium of the spot market, so how to smooth out this high premium? You can select 10-20 currencies that have reached the full funding rate 1-2 times. You will find that after the full funding rate 1-2 times, more than 90% of the cottage will choose to drop the price sharply to smooth out the high premium, instead of continuing to rise the price to smooth out the high premium. What is the essential reason behind this statistical phenomenon? The real reason should be very complicated, or it is difficult to explain clearly. One reason is that it takes real money to pull the market. Once the market is pulled to a high premium in the spot, the increase is basically very exaggerated. At this time, accompanied by a rapid surge in trading volume and positions, a large number of traders pour in. When too many traders participate, the difficulty and risk of the dealer controlling the market will increase, so at this time, the price will fall sharply for sorting. #Meme浪潮持续,你看好哪一个? #美国大选如何影响加密产业? #BTC突破6W5

#Meme浪潮持续,你看好哪一个? #美国大选如何影响加密产业? #BTC突破6W5