There are two main directions for Synthetix V3: one is to increase collateral assets in addition to SNX, and the other is to help more assets improve liquidity through the zero-slippage feature of atomic swaps.

Written by Babywhale, Foresight News

With the launch of tokens by Kwenta, the trading platform of Synthetix ecosystem, the projects of Synthetix ecosystem have basically completed the process of decentralization. Synthetix itself mints sUSD and Synths, and Kwenta's spot and perpetual contracts and Lyra's futures market have formed a complete Synthetix synthetic asset ecosystem. Today, the concept of synthetic assets that "peaked at the debut" in the last bull market has almost disappeared. Synthetix, a veteran project born in the first year of DeFi, has almost become the "last glory" in this field.

Atomic Swaps and Liquidity Relays

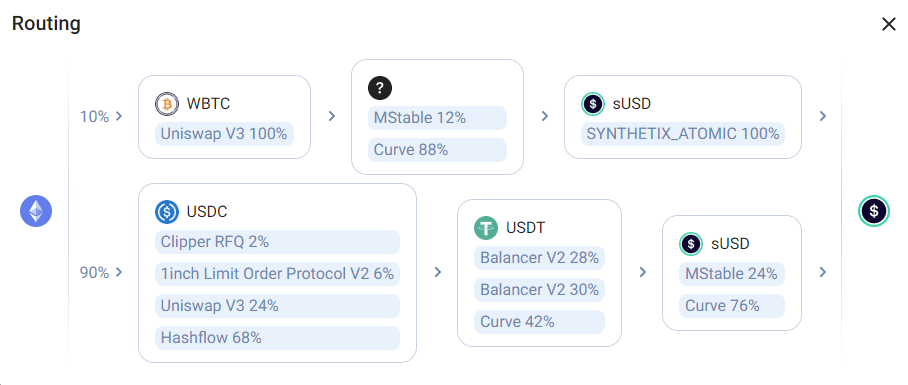

With the improvement of the atomic swap function in May this year (allowing users to price synthetic asset transactions through a combination of Chainlink and DEX oracle price feeds, and automatically perform asset-to-asset transactions at a reasonable fee) and the integration with 1inch, Synthetix has opened up the "zero slippage" narrative for the synthetic asset track, that is, users can trade WBTC, WETH and other assets for sBTC and sETH first, then redeem them for sUSD on Synthetix and trade sUSD for other stablecoins through Curve, etc., which greatly reduces the slippage caused by directly trading the former for stablecoins.

But in fact, the liquidity of sBTC and sETH is not high, with a total value of only $7.82 million and $17.6 million at the time of writing. When using 1inch to trade 1,000 Ethereum for sUSD, only a small part of it is done through atomic swaps.

The reason why this function can be realized is that sBTC and sETH in the Synthetix ecosystem are not backed by actual Bitcoin and Ethereum assets, but are just synthetic assets that represent the prices of the two. In short, this asset is actually "created" by Synthetix out of thin air. It used to circulate only within the Synthetix ecosystem, but now it is the best tool to reduce transaction slippage.

Faced with the question of "trading synthetic assets is not as good as directly trading the assets themselves", when high APY is no longer recognized by users, Synths (i.e. sToken) and sUSD directly rely solely on oracle price feeds to generate zero slippage transactions, which has found a reasonable reason for the existence of synthetic assets.

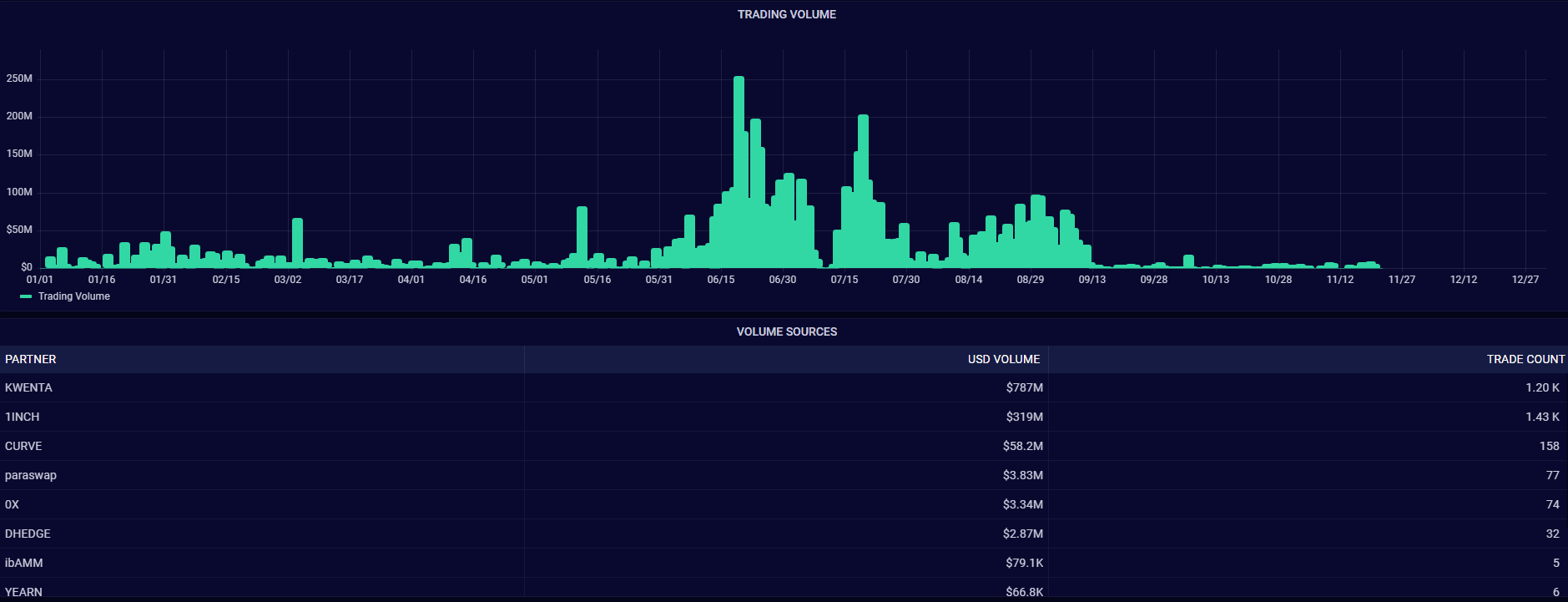

According to data from the Synthetix official website, one month after the atomic swap was perfected, the spot trading volume of Synths assets on the Ethereum mainnet soared to a maximum of US$255 million. So far this year, the total spot trading volume of Synths on the Ethereum mainnet, including Kwenta and 1inch alone, has exceeded US$1 billion, and the price of SNX has also experienced a good rise in the middle of the year.

After finally discovering the "lifeline" of synthetic assets, Synthetix's upcoming V3 plan will continue to rush on the road of liquidity.

Synthetix V3 Key Updates

A few days ago, Noah Litvin, a member of the Synthetix team, posted that the code of Synthetix V3 has entered the audit stage and is expected to start migration in January next year.

According to an article released by Synthetix in July, the focus of the V3 update mainly includes three aspects:

Permissionless asset creation — Any financial derivative can be built on top of Synthetix V3;

Better control over credit — Stakers can pick and choose the assets they want to pledge, which improves the hedging experience and allows new assets to add liquidity without Spartan Committee approval;

“Liquidity as a Service” — Synthetix will not only be a protocol for trading b/c of its debt pools and assets, but will also help users quickly increase liquidity for any financial derivatives on the chain.

To put it simply, there are actually only two main directions for V3: one is to increase collateral assets in addition to SNX, and the other is to help more assets improve liquidity through the zero-slippage feature of atomic swaps.

In the past, the logic behind the appreciation of SNX tokens was that the increase in Synths trading volume increased SNX staking income, thereby attracting more users to buy SNX for staking, thereby generating more liquidity for sUSD and other sTokens, thereby creating a positive cycle.

But in fact, due to the high c-Ratio (currently 400%) of rewards in the process of staking SNX to mint sUSD, users are not very motivated to stake because they are worried that the price of SNX will fall and they will not be able to obtain SNX inflation and fee rewards. After adding other staked assets, SNX is no longer the largest source of sUSD but only a way to obtain income, which may increase users' interest in SNX.

However, if sUSD is minted using Bitcoin or Ethereum’s packaged assets as collateral, and then sUSD is used to mint sBTC and sETH to increase slippage-free liquidity, it is not very clear whether such behavior is necessary and whether the so-called “liquidity as a service” is truly needed by assets other than Bitcoin and Ethereum.

SNX has a limited market value. In order to support the huge market in the future, Synthetix must support more collateral assets to increase the issuance of sUSD, and even gradually make SNX minting sUSD a thing of the past, so that SNX can better represent the value of the Synthetix project itself without being constrained by other factors.

Previously, Kain Warwick, founder of Synthetix, released proposal SIP-276, suggesting that the issuance of SNX be set at 300 million, and that additional issuance be stopped after reaching that number. This proposal has sparked a lot of discussion in the community. Although this is a reasonable change in the long run, it is still opposed by many current stakers. With the arrival of V3, the fees generated by atomic swaps will increase further, and the constant total amount will further increase the appreciation space of SNX. SNX may eventually exist more as a Synthetix governance token, and Synthetix will also change fundamentally, further developing the narrative of synthetic assets as "liquidity relays."