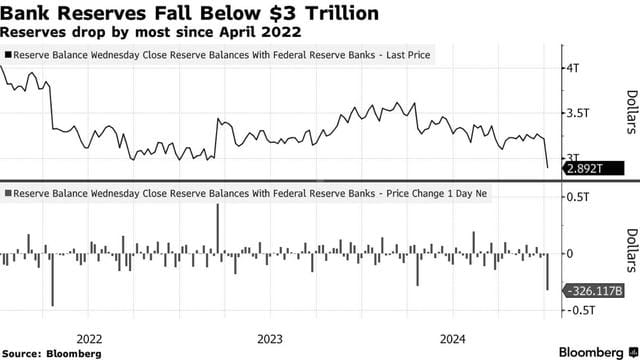

Zhitong Finance APP learned that the reserves of the U.S. banking system have fallen to the lowest level since October 2020, falling below the $3 trillion mark, which has an impact on the Federal Reserve's decision to continue to reduce its balance sheet. As of January 1, bank reserves fell by $326 billion to $2.89 trillion, the largest weekly drop in two and a half years.

The decline was related to banks reducing balance sheet-intensive activities such as repurchase agreement transactions at the end of the year to strengthen their regulatory books, resulting in cash flows to the central bank's overnight reverse repurchase facility (RRP), thereby reducing liquidity in other liabilities on the Fed's books. RRP balances increased by $375 billion between December 20 and December 31, and then decreased by $234 billion on Thursday.

As the Fed continues to purge excess cash from the financial system through its quantitative tightening program and institutions continue to repay bank Term Funding Program loans, Wall Street strategists are closely watching the minimum reserve level, estimating that including the buffer, the reserve level should be between $3 trillion and $3.25 trillion.

Last month, the Fed said it would continue to shrink its balance sheet and adjust the interest rate on its RRP facility to ease downward pressure on short-term interest rates, which could temporarily ease the reserve shortage problem.

Discussions are intensifying about how long the Fed can continue its quantitative tightening policy without triggering memories of September 2019, when reserves in the banking system became too scarce as the Fed was shrinking its balance sheet, a shortage that led to a surge in the key lending rate, the federal funds rate. The central bank had to intervene to stabilize markets.

Although the Fed in June lowered the limit on the amount of Treasury bonds it can allow to mature without being reinvested, there is no clear end date for the quantitative tightening program.

The recently reinstated debt ceiling could make it harder for policymakers to judge the ideal level of reserves, as measures taken by the Treasury to maintain the ceiling could artificially increase liquidity in the financial system and mask indicators of reserve scarcity. According to a New York Federal Reserve Bank survey of primary dealers and market participants, two-thirds of respondents expect quantitative tightening to end in the first or second quarter of 2025.