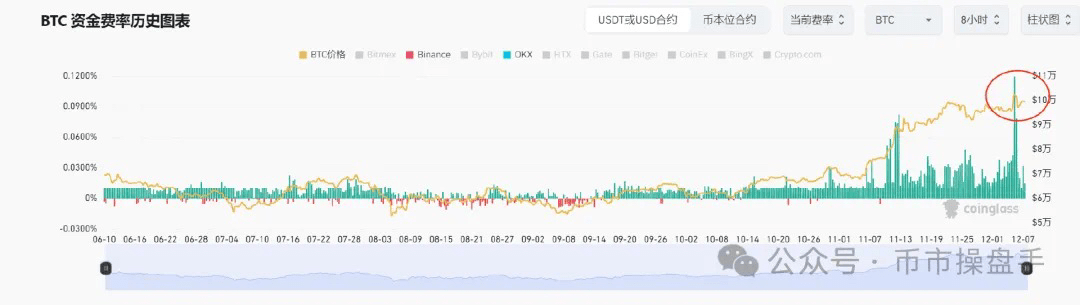

On December 5, as Bitcoin broke through $100,000, market bullish sentiment reached a peak. According to Coinglass data, the annualized weighted average funding rates for OKX and Binance reached 116% that day, setting a new high in nearly three years. Subsequently, Bitcoin corrected from $104,000 to $90,500 within 12 hours, a drop of up to 13%, leading to nearly $700 million in long positions being liquidated. This massive shake-up has been interpreted by many as a signal of peak sentiment and loosening positions. So, is a sharp decline coming?

#

#

From a trading perspective, the adjustment on December 5 is still considered a technical adjustment within the bull market process for two main reasons: First, Bitcoin only stayed in the $95,000-$90,500 range for 5 minutes, and the main purpose of the spike was to flush out leveraged long positions, which aligns with the characteristic of 'gradual rises and sharp falls' in a bull market; second, during Bitcoin's adjustment, altcoins remained active, with ETH even reaching a new peak, and the market's profit-making effect continued to spread, indicating that risk appetite did not cool off due to Bitcoin's adjustment. However, despite the lack of continuous downward momentum in the short term, the market still requires some time to digest profit-taking. Therefore, Bitcoin is likely to continue oscillating in the range of $88,000-$105,000. Even if there is a short-term breakout (or drop below) this range, it will quickly be pulled back.

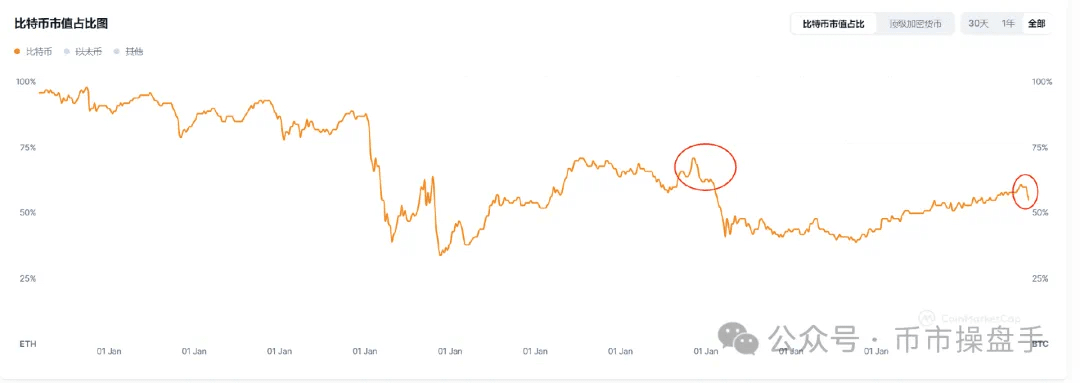

Since November 5, Bitcoin's market share has declined from 59.3% to 53.7%, while the market capitalization share of altcoins has risen from 8.67% to 12.45%, and their trading share has increased from 23% to 41%. This change indicates that capital is shifting from pursuing absolute value to focusing on price elasticity. Notably, during the previous cycle when this phenomenon occurred, altcoins initiated a frenzied market that lasted more than a month. For example, from March to April 2021, Bitcoin entered a phase of oscillation, its market share peaked and declined, while many tokens in sectors like distributed storage, the metaverse, and Layer2 saw monthly increases exceeding tenfold. Interestingly, the last sector that ignited altcoin season was the 'bull market flag bearer' DeFi, which bears a striking resemblance to the surging tokens like HYPE, UNI, SUSHI, and CRV today.

However, despite the substantial fermentation space for altcoin markets, indiscriminate buying has essentially ended the phase of widespread price increases that eliminates low-priced assets. First, as of December 8, about 60% of the top 150 cryptocurrencies by market capitalization have rebounded to near their highs from March this year, indicating that the pressure of profit-taking in the short term will become more evident. Secondly, the annualized funding rates for most altcoins have reached their highest levels in nearly three years, with bullish sentiment at its peak. According to the experience from the last bull market, when sentiment-driven markets reach a climax, they usually enter a phase of consolidation, during which fundamental narratives are likely to stand out during differentiation.

In addition to the shift in market risk appetite, favorable news for altcoins has frequently emerged at the policy level. On December 6, U.S. President-elect Trump announced the appointment of David Sacks as the White House Director of Artificial Intelligence and Cryptocurrency. Trump stated that Sacks would be responsible for developing the legal framework for the cryptocurrency industry, which means his value propositions will have a profound impact on the future of U.S. cryptocurrency policy. It is worth noting that David Sacks has not only publicly expressed support for Bitcoin multiple times but has also invested in several cryptocurrency projects through his venture capital fund, Craft Ventures, including dYdX, Lightning Labs, and River Financial. Additionally, he is a staunch supporter of SOL. From his past viewpoints, we can summarize three core propositions:

1. Bitcoin is a highly liquid and non-seizable store of value, with its potential value lying in hedging against the depreciation risk of fiat currencies. For Bitcoin to become a global reserve currency, it may need to undergo a significant fiat currency crisis.

2. Cryptocurrencies are changing traditional financing and incentive models, and many cryptocurrencies have practical application scenarios in the ecosystem, thus they should not be classified as securities. Asset class tokens are considered securities and need to be issued through legal and compliant means.

3. In the future, almost all illiquid assets may be blockchainized and tokenized, which will significantly enhance market liquidity and price discovery efficiency. Even traditional liquid assets like stocks may shift to this platform due to the advantages of blockchain technology.

First, David Sacks clearly affirms the value and long-term growth potential of Bitcoin as a decentralized store of value, but he believes that for Bitcoin to become a global reserve currency, a crisis is needed as a catalyst. Therefore, after the 'crypto czar' joined the White House think tank, Polymarket did not raise the probability of the U.S. designating Bitcoin as a national reserve (remaining around 30%). Thus, investors betting on Bitcoin becoming a national reserve may need to lower their expectations.

Secondly, the identification of cryptocurrency attributes should be more flexible. Many tokens with application scenarios should not be classified as securities. This will facilitate the reclassification of tokens that were previously deemed securities by the SEC.

Finally, Sacks believes that asset tokenization will enhance asset liquidity and price discovery efficiency, and it may even disrupt existing asset issuance models and trading platforms. This also explains why recent institutions like BlackRock, Franklin Templeton, Tether, and Visa are all laying out plans for asset tokenization.

As mentioned by a16z's policy director Brian Quintenz, regulatory director Michele Korver, and chief legal counsel Miles Jennings in a joint article: The channel for constructive engagement with regulatory and legislative bodies has now been opened. As regulatory frameworks gradually clarify, project teams exploring blockchain services and token issuance have become possible. Therefore, after Trump took office, RWA may become the new narrative main line.

Operationally, the main narrative of the altcoin market has been repeatedly reinforced, and once a trend is formed, it will not easily end. If a sharp drop occurs in the short term, it will certainly be an opportunity for bargain hunting. After entering the differentiation phase, adhering to the logic of 'the strong get stronger' (the largest gains and the smallest adjustments) will help traders minimize mistakes in the second phase of the altcoin market.