Japan's new Prime Minister candidate "Shigeru Ishiba" won the election vote. Due to the market's uncertainty about his future economic policies, the Nikkei 225 index futures fell rapidly in a short period of time, with the maximum drop reaching 5.68%!

Why should you pay attention to the Japanese stock market and economy when trading cryptocurrencies? (Long warning)

Let me give you a hint:

If you have heard of "Abenomics" but don't know what this economics is about, let me explain it in the most popular language:

Since the Japanese economy has been in a state of "deflation" for a long time, the government has been thinking about how to stimulate the economy almost every year. How to completely get rid of the vicious cycle of deflation?

Therefore, the Japanese government first took the lead in inventing QE (quantitative easing). Yes, the Japanese were the first to use QE. Then they lowered the interest rate to 0 for a long time. This move was also invented by the Japanese. All these moves were to stimulate the economy.

But the effect has not been particularly good, so Abe packaged together various strong stimulus monetary policies and injected all kinds of drastic measures into the Japanese economy in one go!

It even invented the unprecedented negative interest rate!

In the final analysis, we hope that the Japanese people can increase consumption, investment and revitalize the domestic economy, get out of deflation and enter an era of inflation;

But the problem is that Japan's economic deflation is not simply due to people's lack of consumer confidence, but is largely related to its serious aging population structure. After all, young people love to consume and the elderly love to save money, not to mention that many elderly people are still working...

Japan is currently one of the countries with the most serious aging population in the world;

This has resulted in Japan's anti-deflation process not progressing smoothly, but the Japanese government has no other choice, so it has been stimulating and flooding the market with money!

This policy path of going all the way to the end has become an outlier in the global interest rate hike cycle after 2022, but it has also become a feast for global international capital!

Due to the low interest rate environment in Japan and the high interest rate environment outside, carry trade and arbitrage trade became a low-risk, high-return option;

This caused a large amount of money released by the Bank of Japan to flow to the whole world, mainly to the United States. A large part of the rest seemed to flow to South America, but in fact it all went to the "Cayman Islands"... you know...

With a large amount of liquidity, the stock markets of major economies around the world (except China) quickly stopped falling even during the interest rate hike cycle and reached new highs in the high interest rate environment;

Doesn’t this cheap Japanese yen liquidity have any cost?

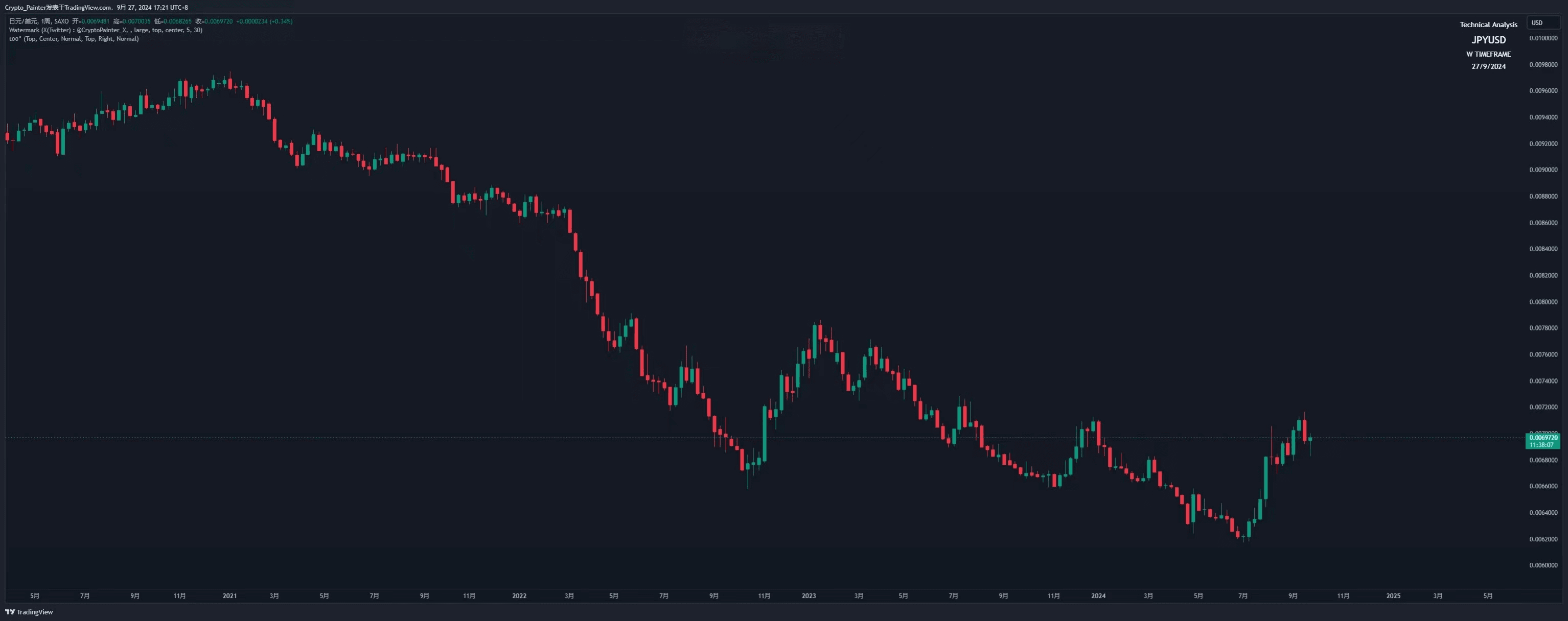

Of course there is, that is based on the fluctuation of the Japanese yen exchange rate. In the past two years or so, the Japanese yen has really depreciated all the way, and the short-selling of the Japanese yen can be regarded as the "best transaction of the year";

But sooner or later you will have to pay for what you have done!

From the first end of the "negative interest rate" era by the Bank of Japan in 2024 to the recent two rate hikes, the yen's downward trend has now ended;

The biggest risk to the massive outflow of cheap liquidity from Japan is the appreciation of the yen, especially against the dollar;

Not long after the Bank of Japan announced the latest rate hike to 0.25%, the global flash crash on August 5, which everyone remembers vividly, was largely due to the liquidation of arbitrage positions of a large amount of yen liquidity that had originally flowed out;

Fortunately, the Bank of Japan stepped on the brakes in time and announced that it would not raise interest rates for the time being, so the situation did not deteriorate further...

Since then, whether the yen will continue to appreciate and whether the Bank of Japan will continue to raise interest rates has become a machete hanging over the head of the financial market. Although it is far away from the neck, the back of the neck always itches, just like when someone points a gun at you, you always feel uncomfortable...

And just today, the new Japanese Prime Minister Shigeru Ishiba won the election!

Because his economic views are conservative, that is, he believes that government debt should be controlled, and he is cautious about the Bank of Japan's ultra-loose monetary policy and believes that normal monetary policy should be gradually restored;

So, after the news came out, the Japanese yen soared and the Nikkei plummeted!

=============Dividing line=============

After introducing the background, let’s talk about why Japan has such an intricate relationship with the cryptocurrency market?

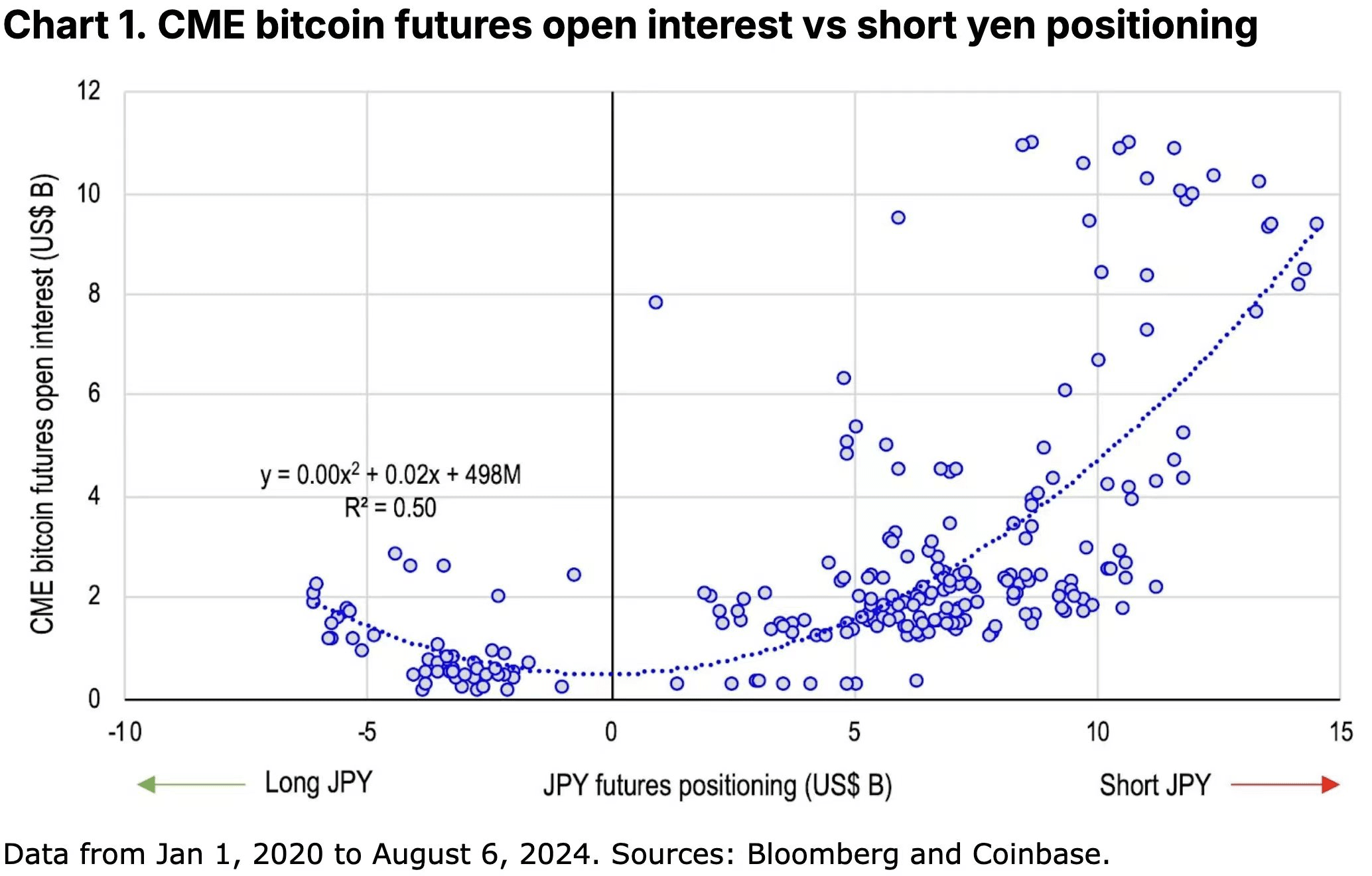

If you see the chart in the quote, you must be curious why the Nikkei index has such a similar overall trend to BTC since August?

First throw the data (chart from Coinbase: David Duong):

The horizontal axis in the figure represents the distribution of short and long positions in the Japanese yen, while the vertical axis corresponds to the distribution of total open interest in CME BTC futures contracts;

You can clearly see that as the short positions of Japanese yen increase, the futures contract positions of BTC on CME will also increase significantly, which suggests that the funds for BTC in the CME futures market, which is dominated by institutions, may very likely come from Japanese yen liquidity or related derivative transactions;

The popular explanation is that some institutions have lent a large amount of Japanese yen to conduct arbitrage transactions on CME's BTC futures contracts;

So who are these people and how do they make money?

I made a preliminary judgment in this article earlier.

x.com/CryptoPainter_…

The general process is: institutions lend Japanese yen → short Japanese yen in the process of converting into US dollars → use US dollars to arbitrage on CME's BTC futures contracts → hedge futures and spot through the purchase of BTC spot ETFs → achieve an annualized low-risk return of about 12.7% (without leverage)

However, we can learn from Morgan’s report that the leverage ratio of this part of funds ranges from 2 to 14 times. Calculated at an average of 5 to 8 times, the annualized return of the above process can easily reach more than 60%!

Considering the long-term low yen situation, the risk is very small and the reward is very large!

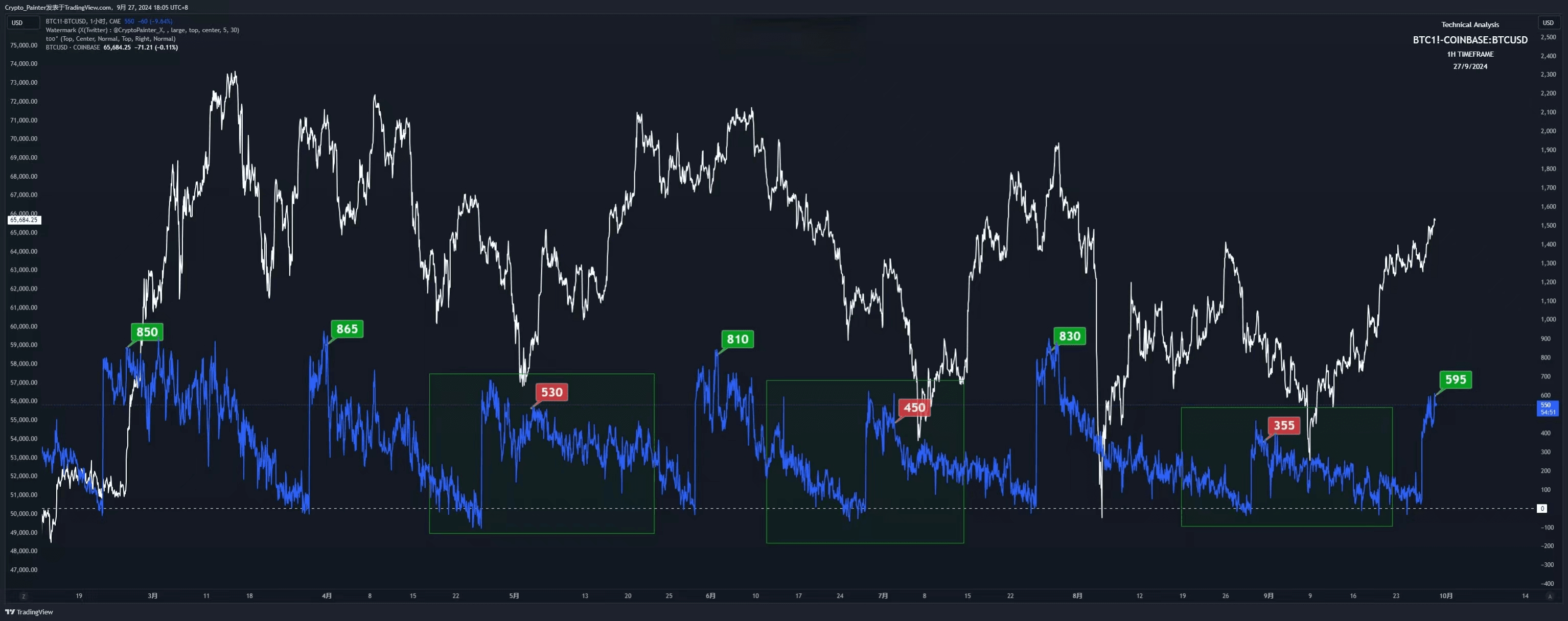

Following the above article, I made a comparison chart of the average premium of CME's BTC futures contracts relative to Coinbase's spot contracts. It can be seen that when the average premium of CME is less than 1%, that is, less than $500 on average, arbitrage transactions for BTC will be greatly reduced, and the price of BTC is also at a relatively low level or in a small-level short trend;

The green box in the figure marks the interval that meets the above two conditions;

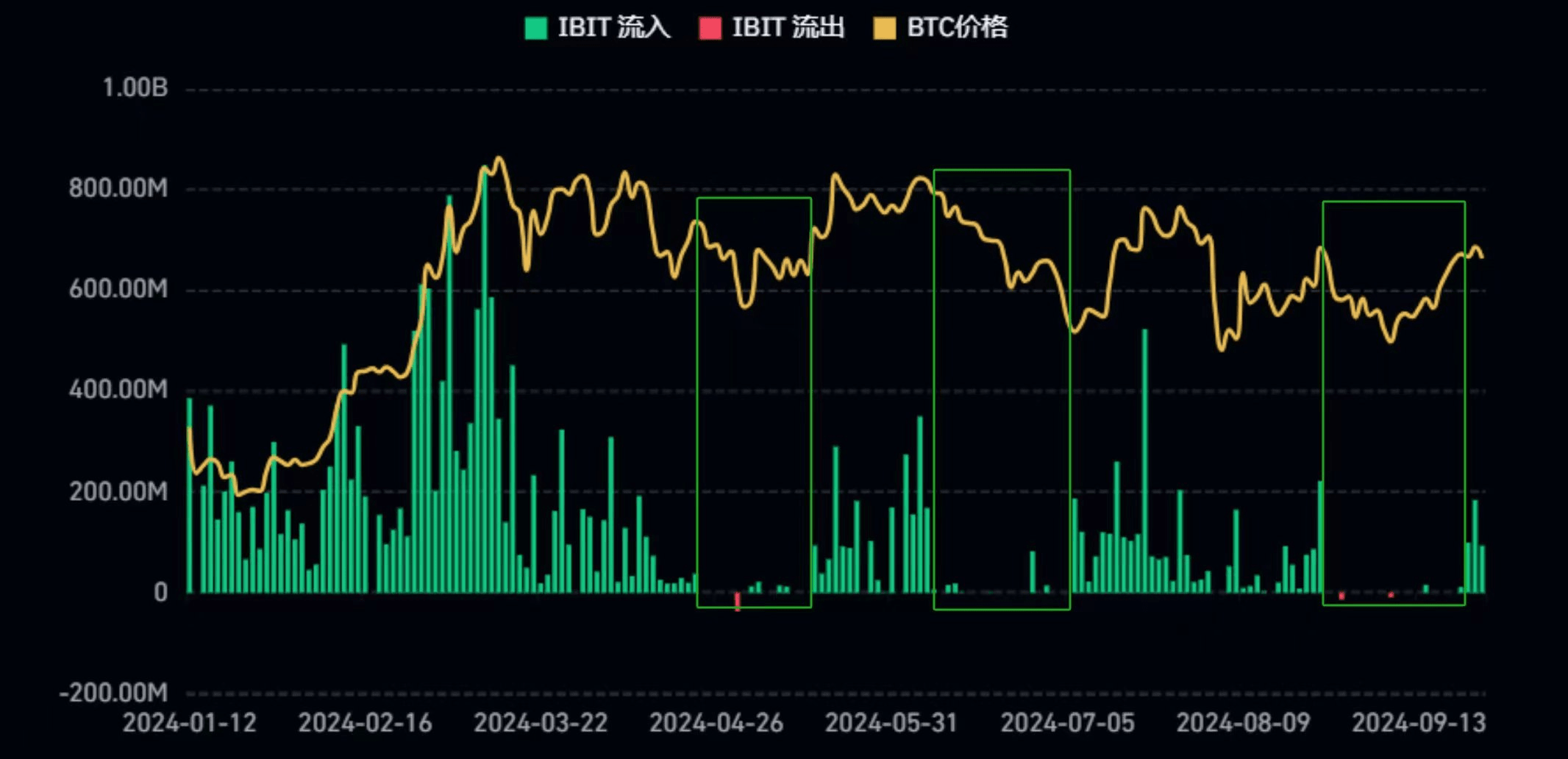

If we turn to the net inflow of IBIT in the BTC spot ETF market, we can find that whenever the above conditions appear, when arbitrage transactions are risky or the profit margin is not high, the net inflow of IBIT will come to an abrupt halt!

Therefore, I have every reason to suspect that the main purpose of BlackRock's so-called institutional investors entering the BTC spot market through ETFs is not to invest in BTC for a long time, but to earn an annualized 60% ultra-low risk return...

This leads to a serious question: in the current BTC spot ETF market, of the more than $18.3 billion in net inflows, how much of the funds are for arbitrage?

If the yen further increases interest rates, causing these funds to withdraw from the market, what impact will it have on prices?

I can't get the answer to this question for now, but the above reasoning process helped me answer several other questions:

Why does BlackRock's IBIT always see large net inflows when BTC prices are high?

A: Because when prices are high, the futures market premium is higher, and arbitrage trading at this time has greater profit margins and less risk of wear and tear;

Why do net inflows into BlackRock’s IBITs seem to have far less impact on market prices than the weightings of Fidelity’s ETFs, and sometimes even no impact at all?

A: Because most of the funds are directly hedged in the CME futures market after they flow in, so whenever there is a large net inflow of IBIT, CME's futures positions will also increase significantly;

If the yen continues to raise interest rates or the yen continues to appreciate, what impact will it have on BTC?

A: We will see that IBIT continues to experience large net outflows in a limited period of time, but there will be no obvious impact on the price;

===============Dividing line================

Summarize:

1. In the current BTC market, or the main source of liquidity in this bull market, a considerable portion of the funds may come from Japanese yen liquidity. It is still important for the U.S. stock market and cryptocurrency market to continue to pay attention to the trend of the Japanese yen in the future;

2. The suspension of the yen's interest rate hike and the rapid rate cut of the US dollar are equivalent to the handover of monetary policy. The tap on the left is closing, but the tap on the right is opening. The time difference between the two is an uncertain variable. If the yen's interest rate hike is accelerated, it is a risk, and if the US dollar's interest rate cut is accelerated, it is a benefit.

3. The victory of the new prime minister may accelerate the closing of the left tap, so we need to see the accelerated opening of the right tap. The next interest rate meeting on November 7 will likely become a fait accompli.

4. In this relay process, the possible risks come from repeated inflation and hot employment. The logic of trading recession has completely faded, and paying attention to employment data and inflation data has once again become the first choice;

5. The sentiment of funds in the cryptocurrency market will become a key force during this relay period. The price fluctuation will not decrease, but is likely to become larger and larger.