The international exchange rate market has always been the main battlefield of the China-U.S. financial war. If the A-shares in recent years have made investors worldwide take notice, then the performance of the offshore RMB exchange rate market has been somewhat disappointing.

However, regarding whether this round of RMB depreciation is passive or active, there is a huge divide in the market, with everyone having different views. For foreign exchange speculators, betting unilaterally on long-term depreciation or appreciation of the RMB is unwise. However, for the country and foreign trade enterprises, the depreciation of the RMB can indeed offset the negative impact of tariffs.

So, does the decline in the RMB exchange rate mean that the U.S. has once again gained the upper hand in this financial war? What profound impact does the depreciation of the RMB have on the prices of Chinese assets?

The stronger the dollar, the sooner the recession comes.

On December 2, Federal Reserve Governor Waller stated at a seminar that he personally prefers the Federal Reserve to continue cutting interest rates in December, as the current monetary policy is sufficiently restrictive and can bring downward pressure on inflation.

In other words, even if the Federal Reserve cuts interest rates by 25 basis points in December, the overall interest rate level remains high, and such a high rate can still drive U.S. inflation data to continue declining.

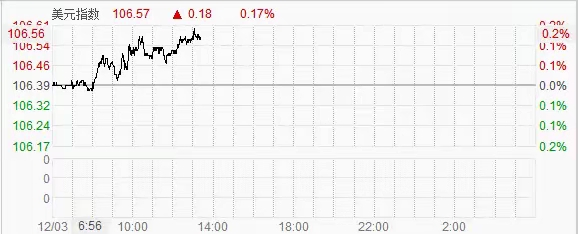

Faced with the interest rate cut expectations released by the Federal Reserve, the foreign exchange market clearly did not take the speech seriously, and the dollar index continued to perform strongly after the market opened in China. The active depreciation of the dollar directly caused the RMB exchange rate to fall below the key level of 7.3.

It is clear that Federal Reserve Governor Waller's speech yesterday was intentionally aimed at cooling the strong dollar, as investors trading on Wall Street for the past two months have been betting that Trump's return will restore the dollar to a strong position.

A strong dollar market is what the Federal Reserve wants to see, but if it is too strong, it is not a result that any central bank wants to see.

But it is obvious that since Trump won the election, the Federal Reserve's influence on the financial market has been relatively weak. The market's main focus is still on what Trump said, whom he will impose tariffs on, and what tweets he sends out at night.

The trading front is trying not to miss any opportunity to trade Trump’s policies.

But what kind of monetary environment does Trump need? It seems even Trump himself hasn't figured it out. Regardless, a strong dollar is not favorable for U.S. exports, and in addition, a high-interest-rate monetary policy is also not conducive to the recovery of U.S. manufacturing.

In summary, the current market reaction seems to be trading on the success of Trump’s policies, but it is actually adding difficulty to the implementation of Trump’s policies.

The strength of the dollar is essentially superficial; it is fundamentally guided by policy expectations and interest rate hike expectations that attract global hot money into the U.S. market, promoting the appreciation of the dollar.

However, in the trade settlement market, the stronger the dollar, the greater the risk of holding dollars. The return and resurgence of U.S. manufacturing is even more out of the question, and hollowing out will become increasingly serious.

For the capital market, since holding dollars and placing money in U.S. banks allows for effortless earnings, why go to great lengths to invest in real industries?

Federal Reserve losses expand.

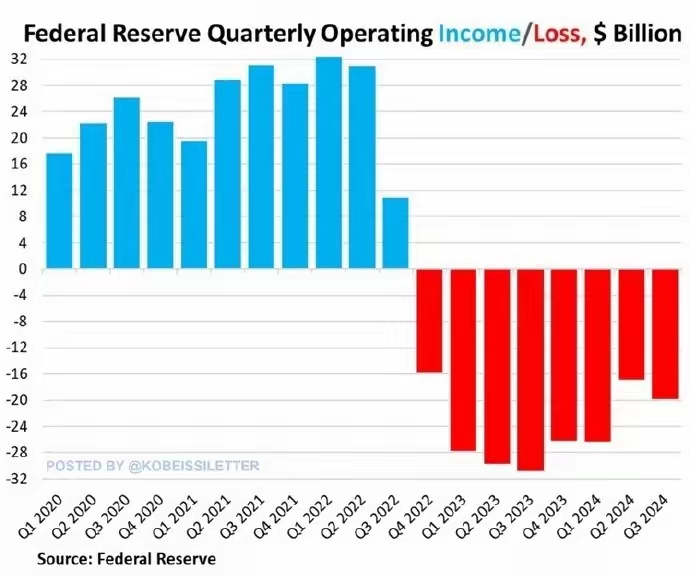

On December 1, the Federal Reserve released a report stating that the U.S. dollar incurred a loss of $19.9 billion in the third quarter of 2024. Compared to a loss of $16.9 billion in the second quarter, the interest rate cuts did not reverse the Federal Reserve's operational situation, and the loss is continuing to expand.

This means that the Federal Reserve has continuously suffered losses for 32 months, with cumulative losses reaching $210 billion. The reason for the losses is that the Federal Reserve has been paying hundreds of billions of dollars in interest to banks and money market funds.

At the same time, the continued decline in U.S. Treasury prices in the third quarter of 2024 is also one of the main reasons for the expansion of the Federal Reserve's losses.

Compared to the weakening of the RMB in the offshore exchange rate market, the problems faced by the Federal Reserve and the dollar are more urgent. Therefore, after Trump's victory, this round of China-U.S. financial war has been so fierce.

In other words, as the dollar market continues to shrink, the decline in U.S. Treasury prices and the losses of the Federal Reserve indicate that time is running out for Trump and the Federal Reserve.

Today, the offshore RMB fell to the warning line of 7.31, setting a new low for the year. Many traders believe that under the inertia of depreciation, the offshore RMB exchange rate may depreciate to around 7.35 in the short term.

In the face of the rapid depreciation of the RMB, although the central bank has not taken significant action, it has also signaled that it does not want the RMB to depreciate too quickly, but the sense of urgency is not very strong.

The main reason is that this round of RMB depreciation is still within a stable range compared to other currencies.

In the foreign exchange market, currencies such as the euro and pound have depreciated more significantly.

Therefore, China does not have a compelling need to intervene; the central price of the RMB exchange rate set today is stronger than the market expectation of 695 points.

In other words, although the offshore foreign exchange market has seen the RMB to USD exchange rate fall below 7.31, foreign trade enterprises still see the official exchange rate pricing remain stable at around 7.2 when the central bank uses dollars to exchange for RMB.

Trade is trade, speculation is speculation.

We can understand this as facing Trump's Tariff 2.0 set to be implemented in 2025, the active depreciation of the RMB helps offset the tariff impacts that the U.S. has on the world.

In short, this round of RMB depreciation will not have a significant impact on China's economy and RMB assets.

The performance of RMB assets in recent years has already shown the market's choice.

Unlike in the past, during this round of RMB depreciation, the A-shares did not experience significant impacts. In other words, the depreciation of the RMB was not caused by a large outflow of domestic capital.

After the release of Trump’s tariff policy, A-shares began trading on bad news, with the Shanghai Composite Index rising from 3200 points to above 3350 points, and this trend has not ended.

In addition, Chinese government bonds have also encountered massive buying, with the price of ten-year Chinese government bonds rising significantly, and the yield falling below 2% yesterday.

According to media reports, there will be important economic meetings held from December 11 to 12, during which China will announce more economic policies and monetary policies.

From December 17 to 18, the Federal Reserve will hold a monetary policy meeting, and afterward, it will announce the latest monetary interest rate policy.

These important meetings will determine the global economic direction for 2025; the market is trading or pricing in expectations of the economic impact of policies.