————————————————————

📍2024 is a year of transformation and recovery for the crypto industry. After the turmoil of the last cycle, the industry has made significant progress in rebuilding trust, promoting innovation, and developing into a mature financial and technological ecosystem. This article will narrate 24 years of crypto in four aspects:

1) Geopolitical macro analysis

2) Macro analysis of the crypto market

3) Policies and regulations

4) Organizational layout

5) Is 2024 the year of SOL?

6) The Prospect of MEME

1) Geopolitical macro analysis🔻

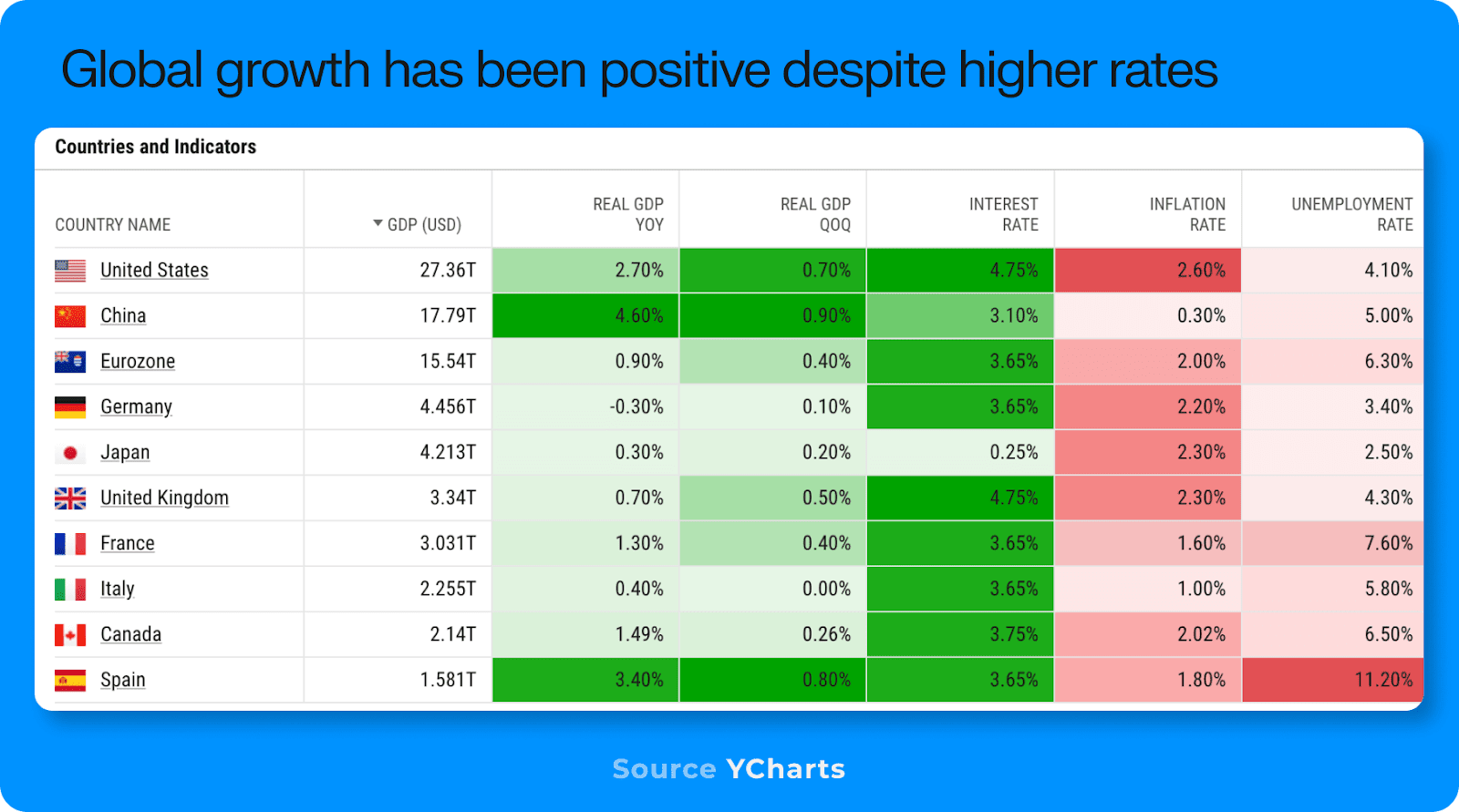

There are signs that the global economy will enter a recession in 2024, but the Federal Reserve has managed to control this situation by cutting interest rates in a timely manner. The market is pricing in the potential for AI to improve productivity and believes that companies that adopt AI will receive higher future returns.

Data showing high demand for gold reserves by central banks in China, India and Turkey was the main driver of gold prices. Despite global tensions due to an oversupply of crude oil produced in the United States, energy costs remained stable

China has now shifted to an accommodative monetary policy, lowering interest rates and increasing lending programs to boost market development.

2) Crypto market macro analysis🔻

In August 2024, due to the German government's selling of BTC and the distribution of compensation for the Mt. Gox incident, Tether was suspected of being investigated by the Department of Justice and the SEC's malicious lawsuit against OG (metamask, uniswap, kraken, etc.), the market faced strong resistance before the third quarter, which was also the main reason why BTC fell to $49,000 in August.

The subsequent election of Trump in the US election became a catalyst to break the consolidation and pushed the market into a bull market track.

3) Policies and regulations

2024 is a turning point for crypto policy, laying the foundation for transformative development in 2025. 👇🏻 Below is a summary of important policies and regulations for the crypto industry in 2024:

⏩Gensler resigned after criticism after Trump won the election

⏩Key bill debates:

A sweeping market structure bill, FIT-21, passed the House of Representatives with surprising bipartisan support, signaling a growing recognition of the need for tailored rules for digital assets.

The (Payments Stablecoin Transparency Act) also passed the House of Representatives, indicating bipartisan interest in establishing a regulatory framework for stablecoins

The House of Representatives also passed a resolution to repeal SAB-121, an accounting rule of the U.S. Securities and Exchange Commission that prevented banks from custodying digital assets, but President Biden ultimately vetoed the resolution.

⏩Centralized stablecoins such as USDC/USDT are favored. The future of DAI is unclear

⏩ Self-custody is gaining attention, privacy issues remain unsolved, DeFi is still unregulated, and basic research will begin in 2025

⏩Trump’s cryptocurrency stance is risky and could be reversed if it challenges the dollar’s status as the world’s reserve currency. In short, government-controlled stablecoins are good, but decentralized currencies are risky.

⏩The most ambitious cryptocurrency policy is expected to be introduced in 2025-26.

4) Institutional analysis

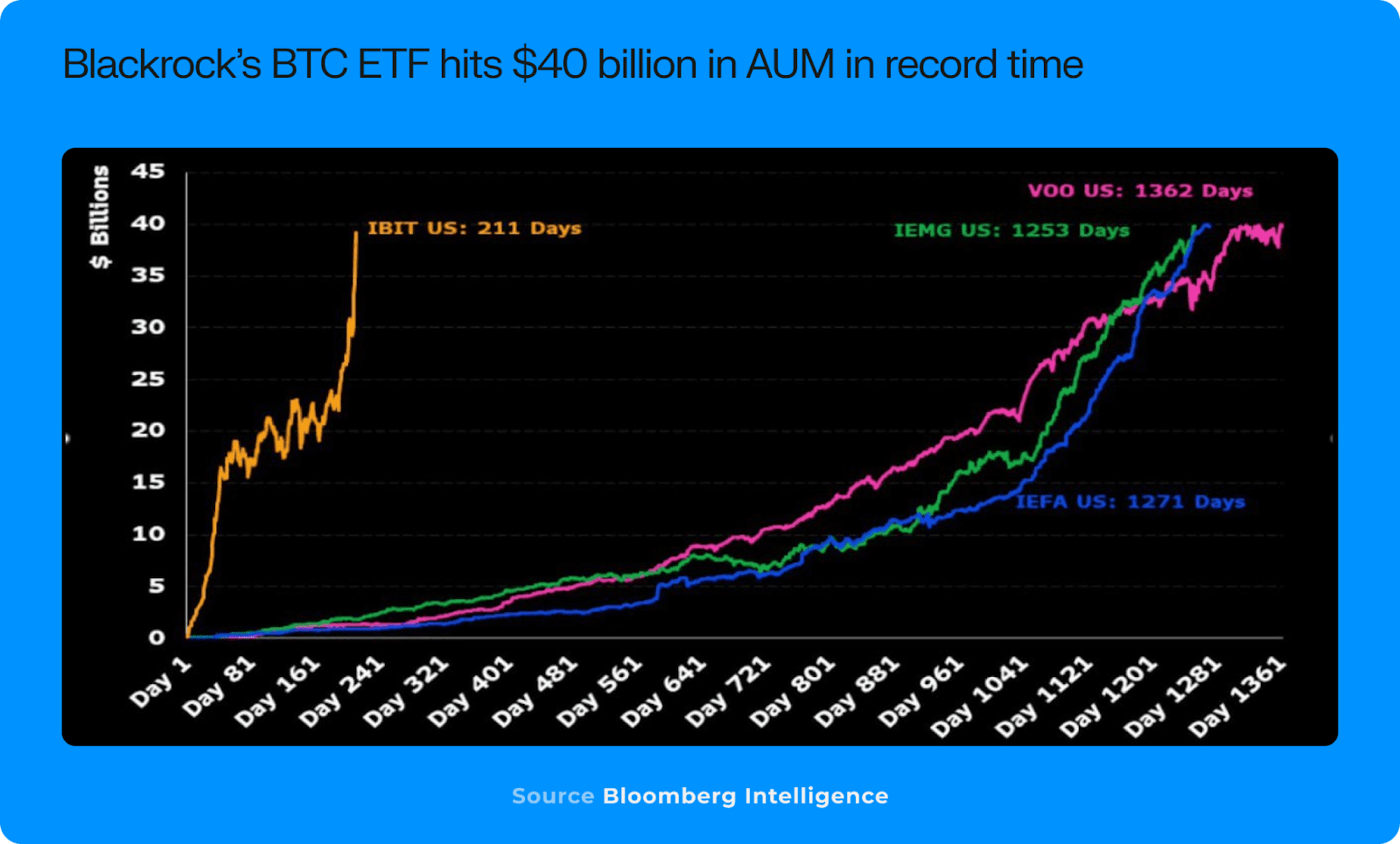

BlackRock’s IBIT garnered $40 billion in AUM within 200 days of launch, setting a record for traditional markets

Blue chip institutions are beginning to study tokenization, stablecoins and research beyond small portfolio allocations

TradFi firms see increased appeal in instant real-time settlement, greater liquidity outside of normal trading hours, and fractional ownership for investor accessibility

📍Other institutional highlights this year besides ETFs include:

——JPM expands its own blockchain platform Kinexys (formerly Onyx) for cross-border payments and tokenization

Goldman Sachs plans to spin off its digital asset platform into a separate entity to expand its product offerings

—Robinhood is launching a cryptocurrency transfer service in Europe and recently expanded its list of tradable assets

Revolut expands its standalone crypto exchange Revolut X to 30 new markets and plans to launch its own MiCa-compliant stablecoin

— Stripe made its largest acquisition to date in crypto, buying stablecoin orchestration company Bridge for $1.1 billion

Visa partnered with Coinbase to enable Coinbase customers to deposit funds in real time using debit cards; it also conducted a live pilot between partners on Solana and Ethereum, transferring large amounts of USDC

——Coinbase has also just launched Apple Pay as its fiat-to-crypto onramp

5) Is 2024 the year of SOL? 🔻

In many ways, 2024 has been the year of Solana, with the SOL token having appreciated by around 120% year to date, while its market cap relative to Ethereum has grown from around 16% to over 25% by year end. Initially, Solana’s rise was largely driven by speculation surrounding its potential to develop into a competing blockchain ecosystem, but by year end, its fundamentals began to bear out that outlook.

In 2024, Token Extensions introduced a new SPL standard, providing greater flexibility to developers. These extensions were released in Q1 and have been widely adopted, marking a major step forward for institutional use cases. Paypal’s adoption of PYUSD stood out, leveraging the standard for confidential transfers and demonstrating how institutional players can leverage Solana’s infrastructure for advanced token functionality. This development highlights the growing alignment between Solana’s technological advancements and institutional needs.

The phased rollout of Firedancer, as well as innovations such as ZK Compression for cost-effective on-chain storage, further bolstered Solana’s technical reputation. These upgrades not only improved performance, but also attracted widespread attention, solidifying Solana’s position as a true competitor to Ethereum.

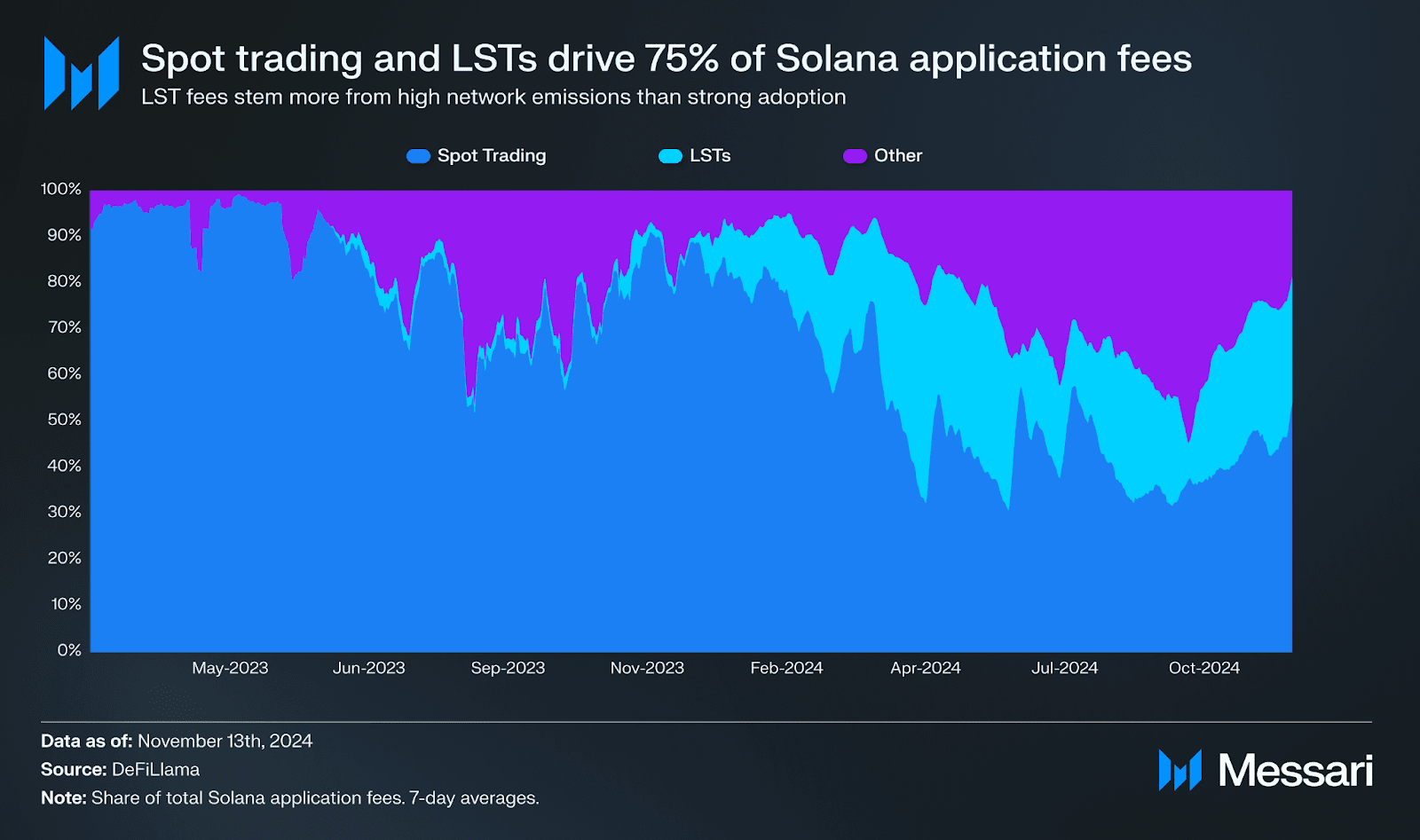

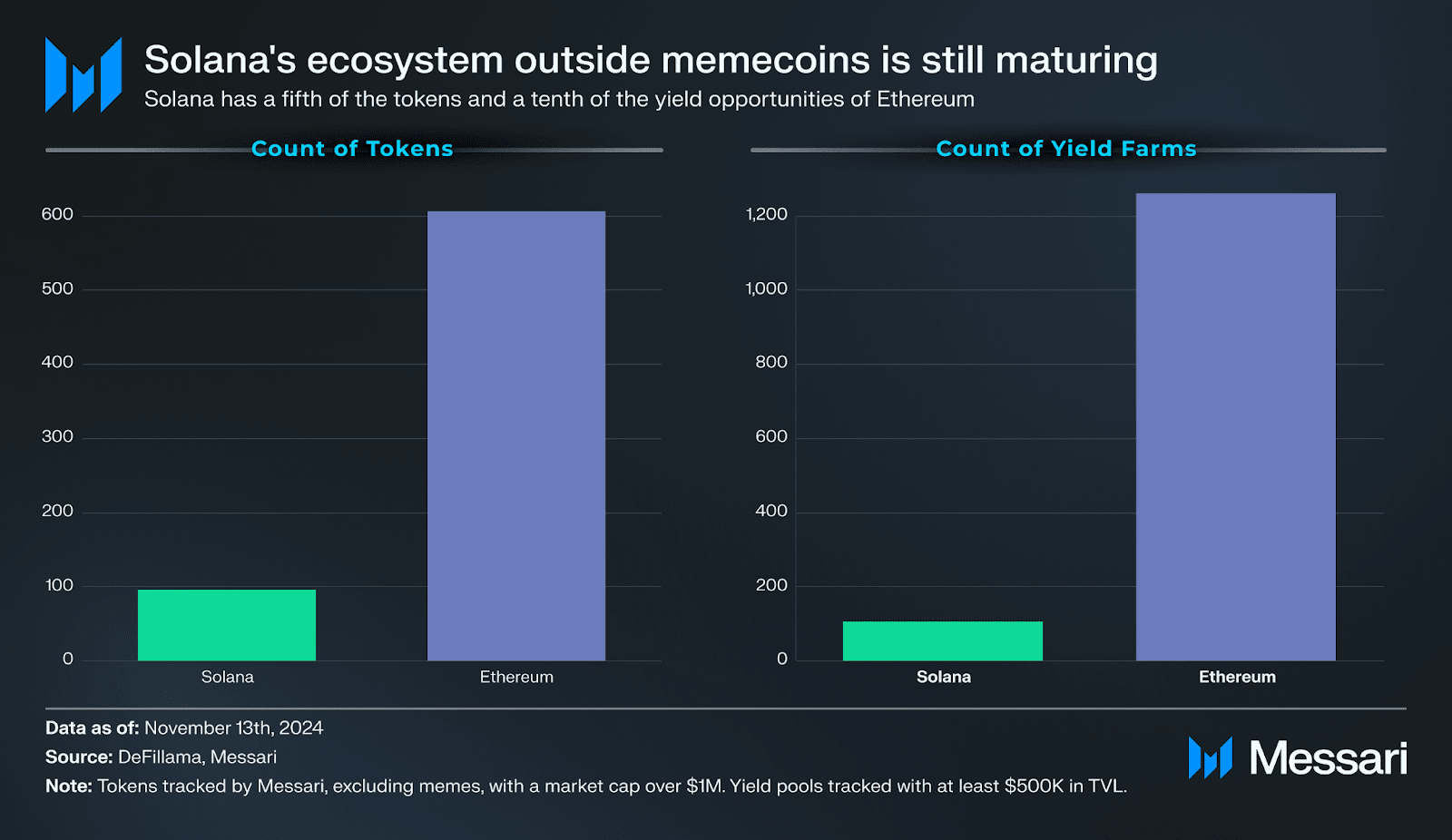

The combination of low-cost, high-throughput transactions and a growing narrative has fueled the expansion of the Solana application ecosystem. Total fees generated by Solana applications exceeded those on Ethereum, with Solana applications contributing over $500 million, or more than half of all on-chain application fees during the period. At first glance, this suggests an ecosystem that is as diverse as Ethereum. However, a closer look at the distribution of fees shows a more concentrated picture.

Currently, application fees on the SOL are highly concentrated in two main areas:

Liquidity staking and trading activity. Liquidity staking accounts for about 25% of application fees and is driven by network staking rewards, while trading fees (generated by decentralized exchanges, DEX aggregators, and even Telegram bots) account for about 50% of the network's total application fees. This ratio is significantly higher than Ethereum, where transaction fees typically account for 20-30% of total application fees and briefly exceeded 40% during the recent market rally.

The disproportionate share of transaction fees on Solana can largely be attributed to its position as the primary execution platform for memecoin speculation. While the dominance of memecoin transaction volume drives fee growth, it also highlights the relative lack of diversity in the Solana ecosystem. Use cases that are prominent on Ethereum, such as lending, yield farming, and liquidity staking, have yet to gain similar traction on Solana.

If 2024 is indeed the year of Solana as an asset, then 2025 will likely mark the year of Solana as a fully realized ecosystem. While Solana’s fee generation highlights its strong position in spot trading, the broader ecosystem begins to show signs of growth outside of trading in 2024.

The emergence of DePIN (Decentralized Physical Infrastructure Network) applications and emerging AI-driven projects indicate that Solana’s footprint in sectors beyond finance is growing. However, the scale of these developments is still in its early stages, and their ultimate impact on network activity remains uncertain.

6) Outlook of MEME🔻

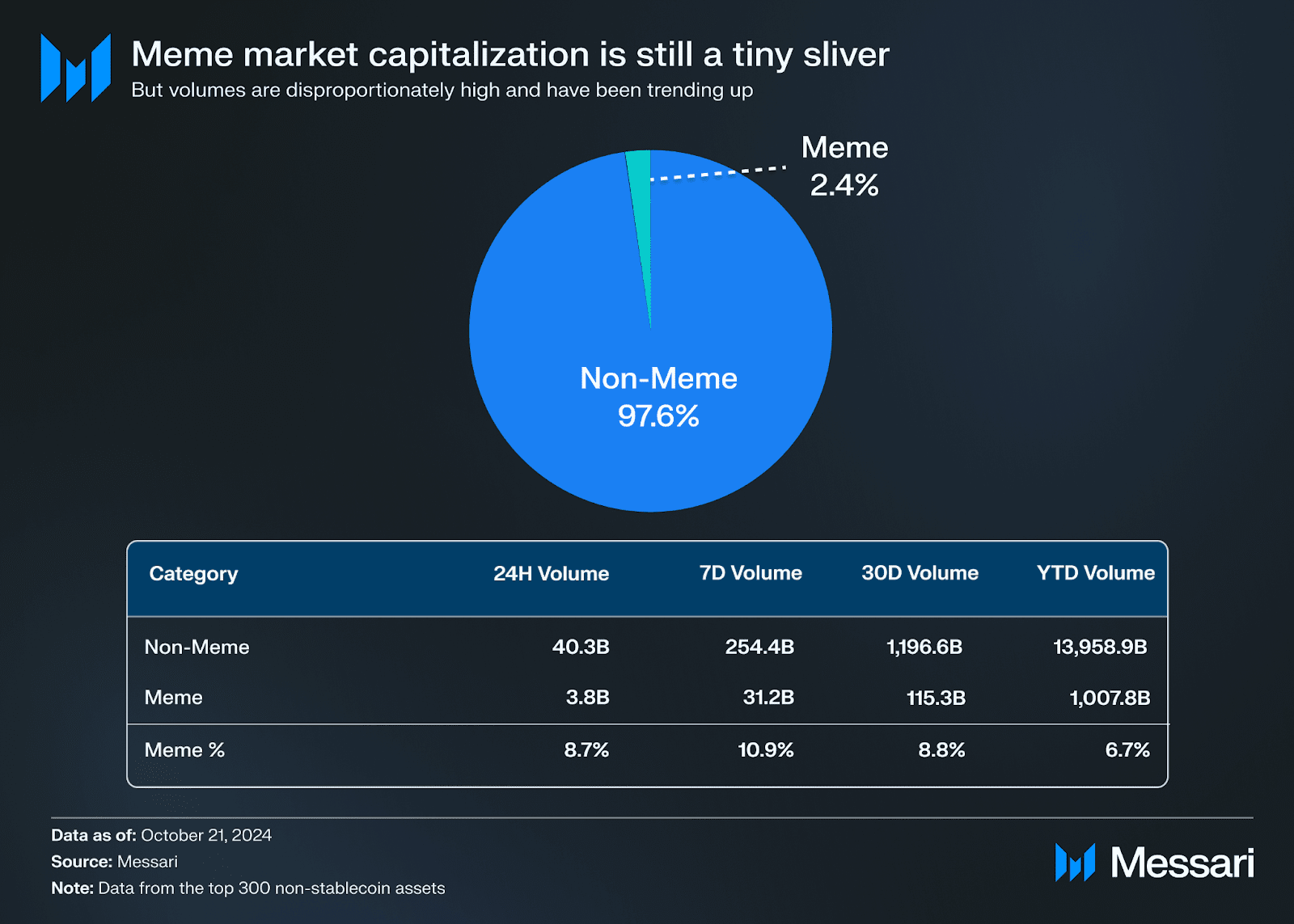

In 2024, memes dominated the cryptocurrency space, and despite accounting for less than 3% of the top 300 cryptocurrencies by market cap (excluding stablecoins), memecoins have consistently accounted for 6-7% of total non-stablecoin trading volume, a figure that has risen to nearly 11% in recent weeks.

While memecoins still make up only a small portion of the market, this large volume highlights the continued interest in speculative assets. The first quarter rally, driven by political memes such as Jeo Boden, marked a recovery in memecoin market share, which subsequently grew from 1.5% to 3%. This was followed by a rally driven by TikTok memes (Moodeng and Chill Guy), and most recently the rise of AI agents triggered by Truth Terminal’s GOAT.

As the broader cryptocurrency market appreciates in 2024, many traders find themselves with excess capital and limited quality investment opportunities. This creates fertile ground for meme coins, which offer high-risk, high-reward potential.

This dynamic is particularly evident on high-throughput networks such as Solana and Base. After strong market performance in late 2023 and early 2024, Solana users found themselves with excess capital and limited deployable opportunities. This is highlighted by Solana’s significantly smaller token count compared to Ethereum, which further pushes users toward the risk curve for memecoins. Solana’s scalability and low transaction costs make it an ideal environment for these speculative assets. A similar pattern has emerged with Base, which launched in 2023, generating surplus capital and available block space, fueling speculation on memecoins.

Meme coins are expected to continue to grow in 2025 thanks to the development of scalable infrastructure (Solana, Base, Injective, Sei, and TON, etc.), low transaction costs, and user-friendly platforms (Moonshot and Pump.fun, etc.).

👇🏻Drivers of growth:

High-throughput blockchains provide ample block space and low fees to facilitate memecoin transactions. User-friendly platforms simplify the transaction process and attract more retail investors to participate. In addition, the high-risk, high-return characteristics of memecoins cater to users' speculative needs, especially in turbulent markets, and may attract users from traditional speculative markets such as sports betting.

Despite their significant growth, memecoins are not expected to capture the largest share of the cryptocurrency market. As the high-throughput on-chain ecosystem matures, new use cases and investment opportunities will emerge. The speculative and social nature of meme coins will ensure their continued existence.

🔹Original link: https://messari.io/report/the-crypto-theses-2025?utm_source=twitter&utm_medium=organic_social&utm_campaign=Theses_2025&destination=Theses_Report