Finance Association December 2 News (Editor Xiaoxiang) In the just-passed November U.S. election month, it seems that politics - especially the policy impact of former President Trump, who is about to return to the White House, is the only factor driving global market trends. Investors are looking forward to marking the end of another brilliant year for the U.S. stock market: the S&P 500 index has risen by more than 25% in the first 11 months of this year.

The rise of the 'Trump trade' has further propelled the rally in U.S. stocks over the past month. However, in the coming week, people may need to prepare for a severe reality check during a challenging 'super week':

This week's U.S. labor market data, including the crucial November non-farm employment report to be released on Friday, will have a significant impact on the Federal Reserve's rate cut plans. At the same time, this will also become a major test that stock market investors, bond traders, and all other participants in the financial markets must face. In the same week that the heavy data is released, many Federal Reserve officials, including Chairman Powell, will also sequentially deliver speeches, which will be particularly critical in the context of the recent expectation that the Federal Reserve's rate cuts will 'increase in the near term and decrease in the long term'...

In recent weeks, many investors may have focused on the various economic policies of the newly elected U.S. President Trump, especially the highly impactful tariff policies. However, the changes in expectations for Federal Reserve rate cuts also seem quite subtle.

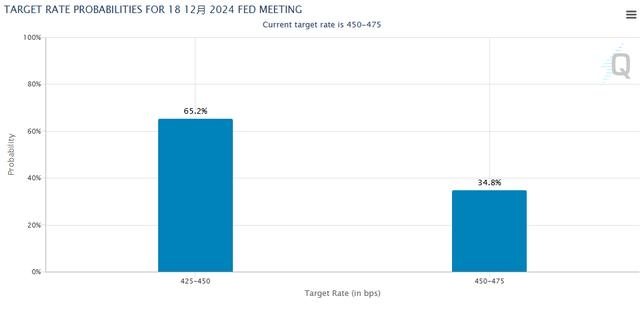

On one hand, expectations for a Federal Reserve rate cut in December have actually warmed up recently. According to the Federal Reserve watch tool from the Chicago Mercantile Exchange, as of last Friday, the market estimated a 65% chance that the Federal Reserve will cut rates at its final meeting of the year on December 18, significantly higher than about 50% a week ago.

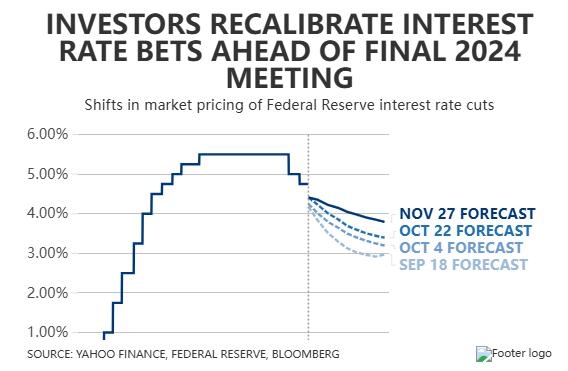

On the other hand, in the long term, investors are increasingly convinced that the Federal Reserve's upcoming easing path will be fraught with difficulties. Expectations in the interest rate futures market indicate that due to a growing pessimism about the inflation outlook, market traders currently expect the Federal Reserve will only cut rates twice next year, far fewer than the four rate cuts implied by the Federal Reserve's September dot plot.

The expectation for Federal Reserve rate cuts to 'increase in the near term and decrease in the long term' largely reflects concerns about the current health of the U.S. economy and labor market, as well as anxieties about a resurgence of inflation under Trump's administration in the future. The key economic data and speeches from Federal Reserve officials this week are likely to further amplify or dissipate the impact of related monetary policy expectations.

Brent Schutte, Chief Investment Officer of Northwestern Mutual Wealth Management, said, 'I think in terms of Friday's non-farm employment data, the market hopes to see something positive, but also does not want the data to perform too well. If the data is very optimistic, it will raise questions about whether the Federal Reserve will really cut rates further.'

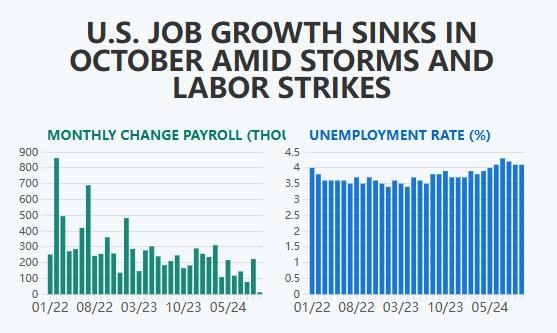

Previously, U.S. non-farm payrolls in October surprisingly plummeted to 12,000, the lowest level since 2020, far below the expected 100,000. While most Wall Street analysts believe the poor data was mainly due to two hurricanes in October and a Boeing strike, some analysts worry that the job market is indeed deteriorating. Therefore, whether the November non-farm data to be released this Friday can return to normal or at least exceed market expectations will be highly scrutinized.

According to the median of an industry media survey, economists generally expect that the non-farm payrolls for November are likely to add 195,000 jobs, a significant increase from the previous month's 12,000. However, a potential downside is that the unemployment rate could rise further to 4.2%, up from the previous month's 4.1%.

The Wells Fargo economic team led by Jay Bryson wrote in a client report, 'Through the monthly fluctuations in non-farm payrolls, we expect the November employment report to reaffirm that while the labor market remains robust in absolute terms, the trend of weakness in employment conditions has not stopped. This message may be conveyed more clearly through the unemployment rate - we expect the unemployment rate to rise to 4.2%.

Edward Jones Senior Investment Strategist Angelo Kourkafas stated that employment data 'will provide a clearer picture of the underlying trends, which is important because there is a lot of debate and uncertainty surrounding the Federal Reserve's interest rate path.'

In addition to non-farm data, the upcoming week will see an extremely busy schedule of speeches from Federal Reserve officials - no fewer than a dozen Federal Reserve officials will make public appearances this week, including the highly watched Federal Reserve Chairman Powell, who will be interviewed at the DealBook/Summit conference hosted by The New York Times at 2:45 AM Beijing time on Thursday.

From the recent statements made by Federal Reserve officials, it appears that despite differences among policymakers on specific details, most officials generally believe that the current rapid pace of interest rate cuts by the Federal Reserve will not continue. Federal Reserve Chairman Powell stated in his last speech in November that there is no need for the Federal Reserve to rush into rate cuts, as the job market remains stable and the inflation rate is still above the 2% target. Powell's latest remarks this week on the prospects for rate cuts in December and next year are undoubtedly likely to attract significant attention from market participants.

Deutsche Bank Chief U.S. Economist Matthew Luzzetti expects the Federal Reserve to cut rates again in December and then pause interest rate adjustments for the entirety of 2025, waiting for more progress on inflation. Luzzetti stated, 'The urgency of rate cuts is much less, and it may make sense to slow the pace of rate cuts earlier than they expect.'

TS Lombard Chief U.S. Economist Steve Blitz stated in a report last week that the problem facing the Federal Reserve is that inserting the current inflation data into the Taylor Rule (a formula used by economists to determine where interest rates should be based on inflation levels and economic growth) indicates that the federal funds rate should remain at current levels.

He said, 'Although I believe the Federal Reserve is still inclined to cut rates, the employment data for November will ultimately be crucial for this data-dependent Federal Open Market Committee.'

Wells Fargo Senior Economist Sarah House stated at a media roundtable last month that 'as we enter 2025, we may see a slowdown in the pace of future rate cuts, with the Federal Reserve possibly cutting rates once every other meeting.' Her team expects the Federal Reserve to cut rates three times in 2025.

(Finance Association Xiaoxiang)