In an October interview with Unchained Crypto, Solana co-founder Anatoly stated that by observing multiple key indicators such as active address count, TVL, DeFi segment, meme frenzy, and developer ecosystem, he noticed that Base is gaining momentum and becoming the strongest L2 within the Ethereum ecosystem.

In late November, Dan, the founder of Little Fox, simultaneously launched the meme coin $CONSENT on both Base and Solana, further drawing comparisons between the two in the crypto market.

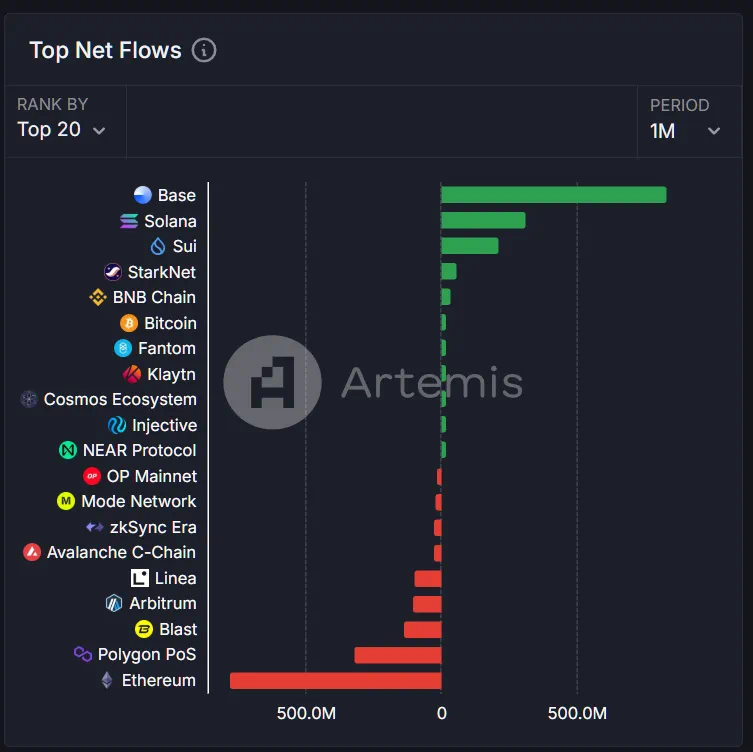

According to Artemis data, last month, the net inflow of funds into Base was $835 million, ranking first among all public chains, while Solana recorded $313 million, less than half of Base.

The sensitivity of fund flow is at its peak; where there are more opportunities, more funds will gather. As the popularity of Solana MEME declines, the next choice for funds will undoubtedly be the Base chain.

Unlike many other L2 projects, Base has clearly stated that it does not plan to issue a native token. This move stands in stark contrast to those past projects that attracted funds through token issuance. Base's growth entirely depends on the inherent value of its platform and ecological construction, with its intrinsic value reflecting more in the leading ecological projects on its chain.

Leading derivatives project SynFutures

As the leading derivatives protocol in the DeFi space, SynFutures is about to airdrop and conduct TGE. Doing the right thing at the right time will bring more attention and adoption to SynFutures from the heat of the Base ecosystem, and SynFutures will contribute to the rapid growth of Base, forming a positive feedback loop. Its token F will also carry more value and potential brought by the Base ecosystem.

Since its launch in 2021, SynFutures has processed over $200 billion in trading volume. Its products have iterated to V3, where V3 Oyster AMM is the first unified AMM and permissionless on-chain order book among similar products.

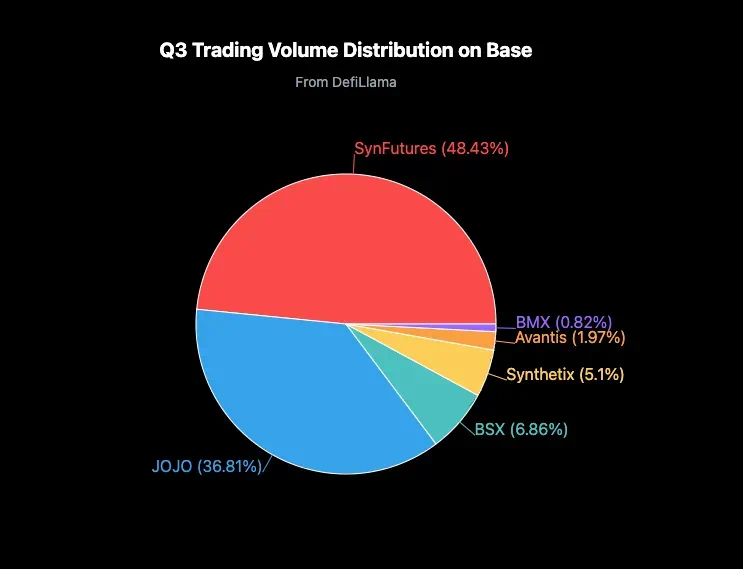

After integrating with the Base chain in July, thanks to its mature products, large community, and strong cooperative resources, it quickly became the leading derivatives protocol by trading volume on the Base chain. It took only 10 days after going live on Base to surpass $100 million in trading volume, with Q3 trading volume accounting for nearly 50% of the Base network.

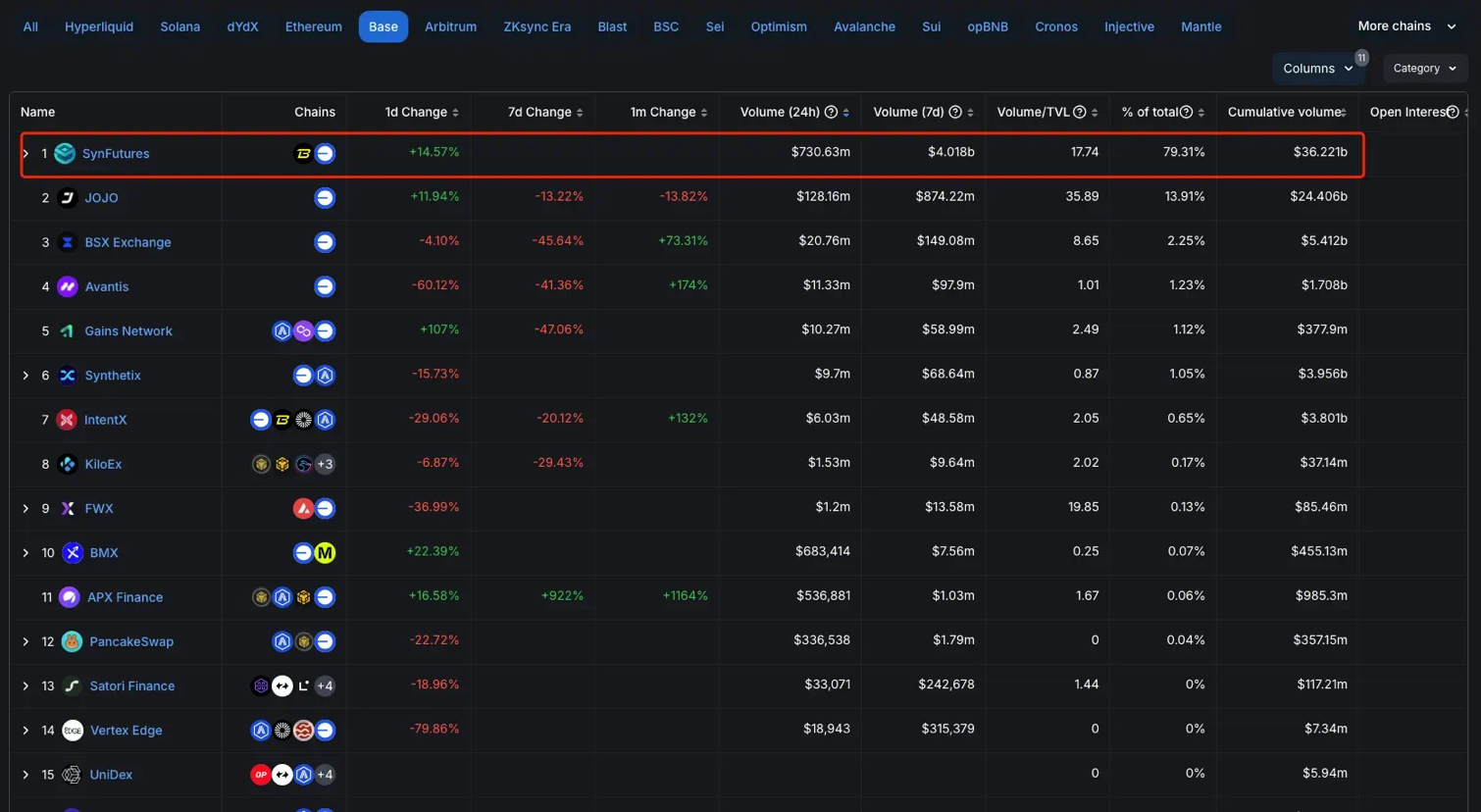

With a cumulative trading volume exceeding $35 billion, an average daily trading volume of over $200 million, and a single-day trading volume surpassing $910 million on November 12, currently accounting for over 70% of the daily derivatives trading volume on the Base chain, which is six times that of the second-ranked project.

With only contract trading, SynFutures has already exceeded $3.3 million in fee revenue over the past 30 days, ranking third in the protocol (the third place being the Sequencer of the Base network). Its strong profitability is also the foundation for SynFutures to operate healthily in the long term and continuously innovate and iterate.

Mechanisms and innovations of SynFutures V3

The Oyster AMM model of SynFutures V3 allows for liquidity to be added within a specified price range, combined with leverage to improve capital efficiency. Unlike the spot market liquidity model of Uniswap V3, Oyster AMM employs a margin management and liquidation framework tailored for derivatives trading, ensuring the safety of LPs and the protocol.

A very important point of the Oyster AMM model is the introduction of bilateral liquidity, allowing liquidity to be added using only one token, without the need to provide bilateral assets at a 1:1 ratio. Liquidity providers can list any trading pair, such as pairing meme coins with each other or pairing any assets. This mechanism brings more flexibility and options to the ecosystem.

oAMM itself is an open-source smart contract deployed on-chain, with the characteristic of being permissionless. There is no need for complex communication and review before listing tokens; anyone can add any trading pair at any time. Whether it's the project party or holders, they can create trading pairs for their own tokens on SynFutures, adding liquidity in 30 seconds. This brings more options to the ecosystem and enhances responsiveness.

By supporting users to provide liquidity at specified price points, SynFutures has realized on-chain limit orders that simulate order book trading behavior, significantly improving capital efficiency. This model aligns more with the habits of market makers on centralized trading platforms, attracting more active market makers to participate, thereby enhancing trading depth and efficiency, providing a trading experience close to CEX.

Unlike off-chain order books like dYdX, the oAMM is deployed on-chain, with all data being public, transparent, and verifiable, completely decentralized, eliminating concerns about dark operations or fake trades.

Compared to GMX's Vault model and dYdX's application chain model, SynFutures compensates for the shortcomings of both while maintaining efficiency and high performance, and seamlessly integrates into the underlying public chain's asset ecosystem. This advantage will further expand with technological iterations.

Perp Launchpad injects new vitality into on-chain asset issuance.

In the past year, asset issuance has become the most attractive track, evidenced by the popularity of runes, inscriptions, and Pump.fun, all proving the powerful appeal of 'innovative gameplay + wealth effect'. The Base chain has performed outstandingly in token issuance platforms, showing significant development potential.

Under the mature framework of SynFutures V3, the launch of the industry's first perpetual contract Perp Launchpad opens up new avenues for on-chain asset issuance and trading, injecting more vitality into the DeFi market and helping Base maintain its lead in the fierce public chain competition!

For example, if a MEME project uses its tokens to create a contract market on SynFutures, it can not only provide more trading methods and choices but also drive arbitrage funds into the market through the price difference between spot and contract, increasing token visibility and holder numbers, amplifying the wealth effect. More importantly, the dominance of the contract market is in the hands of the community, allowing project parties and supporters to profit by providing liquidity, breaking free from reliance on centralized exchanges, and forming a healthier ecological cycle.

In the past few years, the initiative in the spot market has returned to on-chain liquidity pools, and in the future, the dominance of the contract market will also return to the community and on-chain, rewarding the community and holders through SynFutures. These can only be achieved under the V3 model framework, which allows value range settings, supports unilateral liquidity, requires no more than 30 seconds to add liquidity, and operates entirely on-chain with limit order books, providing a unique advantage and moat that is difficult for any other competitor to imitate.

The spot aggregator is planned and may become the Jupiter of the Base chain.

SynFutures and Jupiter have many similarities; both were founded in 2021, have been market-tested, and emerged from the harshest bear markets as profitable leading DeFi protocols. Remarkably, both issued tokens only after long-term stable operations and continuous iterations, using token issuance as a catalyst to enter the next stage of their projects. Token issuance is a node in their long-term strategies, or a new beginning, not just a goal for some projects.

In contrast, Jupiter initially chose to be an on-chain spot aggregator, while SynFutures chose the derivatives track. However, they both aim for the same goal; after issuing tokens, Jupiter began to layout into the derivatives track and achieved notable results. SynFutures will also launch a spot aggregator after TGE, which is precisely what the Base chain lacks: a significant on-chain spot aggregation trading product.

The synergy between on-chain trading volume and asset issuance enables SynFutures not only to provide trading liquidity for Base but also to participate in the asset issuance process, occupying the largest value capture entry on-chain. Once the spot functionality goes live, SynFutures will further consolidate its market position with the dual advantages of spot and derivatives trading.

Track Comparison: What is a reasonable valuation for SynFutures?

SynFutures has announced its tokenomics, with a total supply of 10 billion tokens. Based on its positioning in the ecosystem as 'Jupiter of the Base chain', what is the most reasonable valuation?

The FDV of Raydium, the largest spot DEX on Solana, is $3 billion, while the largest spot DEX on the Base chain currently stands at $2 billion, with a ratio of 3:2.

The Jupiter FDV on CoinGecko shows $11.2 billion, but due to the official announcement of a 30% team share burn, the actual value is $7.84 billion. According to the 3:2 ratio of spot DEX, SynFutures' FDV is approximately $5.22 billion.

However, the spot part of SynFutures has not yet been launched. We can use a multi-dimensional approach to derive a reasonable valuation.

Referring to the FDV when the Jupiter token was just launched, which was possibly $5 billion, a reasonable valuation for SynFutures would be $3.333 billion.

Another well-known derivatives trading platform on Solana, Drift Protocol, has an FDV of $1.36 billion. Simply using the 3:2 ratio would yield a result of $900 million.

However, SynFutures' V3 and Perp Launchpad clearly have greater advantages and growth potential. Averaging the conclusions drawn from comparing Jupiter and Drift, SynFutures' current reasonable valuation is approximately $2.1 billion.

As a project backed by Coinbase, Base has garnered strong support in the market. The likelihood of tokens on the Base chain being listed on Coinbase is much higher than on other chains. If it can go live on Coinbase like Aero, the valuation of F will further increase.

Additionally, with the continued rise of the Base chain and the launch of SynFutures' spot aggregation trading, FDV will also rise significantly, potentially even surpassing Jupiter; after all, Web3 is a place for creating miracles.

Industry prospects and future considerations

From a macro perspective, the development of the Base network has injected new vitality into the on-chain derivatives market, with SynFutures being the most promising project in this field. Its innovative Perp Launchpad model not only promotes the marketization of on-chain assets but also provides users with more diversified trading options. This model may become the mainstream trend in on-chain trading in the future, further consolidating SynFutures' leadership position in the market.

The launch of spot aggregation trading will help SynFutures gradually dominate the two most promising tracks in the Base ecosystem—derivatives trading and spot trading. This dual layout will bring more users and trading volume to SynFutures, thereby driving the platform's long-term sustainable development.

For investors, the launch of the SynFutures token not only reflects its own ecological value but may also indirectly carry the growth dividends of the Base network. The token opportunities in this 'no-coin network' ecosystem may be the most scarce potential explosion point in the current market.