Liquidation & Insurance Funds: How They Work and Why They Are Important to Crypto-Derivatives (Part 2)

Key Takeaways:

Binance Futures is the fastest-growing crypto-derivatives platform in terms of trading volume.

It has an insurance fund that is used to prevent auto-deleverage liquidations.

Unlike other insurance funds, the Binance Futures insurance fund is used for what it was intended.

In our previous article, we gave an overview of how liquidation works and the basics of an insurance fund. But in this continuation, we analyze the current state of insurance funds across various crypto-exchanges

We are going to compare the Binance Futures insurance fund model and discuss why it differs from others. Lastly, we will highlights the key considerations on the state of insurance funds on the whole.

Breaking Down the Binance Futures Insurance Fund

Binance Futures is the fastest-growing crypto-derivatives platform in terms of trading volume, boasting an insurance fund worth 11.5 million USDT, as of January 13, 2020. Binance has self-funded the majority of its insurance fund, which has steadily grown by 15% from its initial 10 million USDT.

Chart 1 - Binance Insurance Fund in USDT

Source: Binance Futures, Data from October 11th, 2019, to January 13th, 2020

Let’s begin with an examination of how the Binance Futures Insurance Fund works:

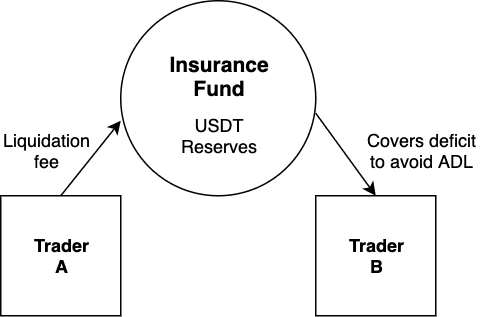

In the varying market conditions, this scenario illustrates how an insurance fund is used to prevent auto-deleverage liquidations. Consider two traders, Trader A and Trader B, who entered a long position on BTC/USDT perpetual futures at the same price.

The following events unfold on Trader A's account:

Trader A goes long BTC/USDT at $8,000, with a liquidation price of $7,700 and a bankruptcy price of $7,600.

As BTC prices plunged beyond $7,700, Trader A enters liquidation and the liquidation engine places an immediate order to sell above $7,600 (the bankruptcy price).

The liquidation order is filled at $7,650, a liquidation fee of 0.3% is charged to Trader A.

The liquidation fee is transferred to the insurance fund.

Meanwhile, the following events play out in Trader B's account:

Trader B goes long at $8,000 with a liquidation price of $7,700 and a bankruptcy price of $7,600.

Due to a sudden jump in volatility, the market price is now at $7,550, below the bankruptcy price.

Binance Futures takes over the remaining positions from the bankrupt trader whose account is in negative equity.

Through its insurance fund, Binance Futures offloads them onto the market progressively.

The liquidation engine places an immediate order to sell and fills the order at $7,500.

As Trader B is already in negative equity, Binance Futures’ insurance fund covers the deficit. As a result, ADL has been avoided.

Diagram 4 - Illustration of how contributions from Trader A prevented Auto-Deleverage Liquidations (ADLs) on Trader B

Source: Binance Futures

In situations where the insurance fund is unable to accept positions from the liquidations, auto-deleveraging will occur.

The State of Insurance Funds in the Crypto-Derivatives Industry

BitMEX has one of the largest insurance funds in the industry, worth approximately $280 million. In 2019, the fund grew 62.8% from 20,700 to 33,700 XBT by Dec 31. In the last quarter of 2019, BitMEX’s insurance fund did not experience any significant drawdown, despite the volatility in BTC prices.

While BitMEX may argue that its large fund is necessary to cover losses during periods of high volatility,, it actually added 730 BTC from liquidations or an increase of 2% on November 22th, as BTC prices plunged more than 15% in two days. In most instances, the fund's outflows were in the lower single digits.

Despite the fund’s significant growth over the year, BitMEX’s trading volume did not increase correspondingly, in fact, its monthly volume has consecutively declined since July 2019. Traditionally, an insurance fund grows along with trading volumes. This disparity has led to scrutiny and criticisms of BitMEX’s risk management and liquidation practices, which suggests that its insurance fund has outgrown its purpose.

Chart 2 - Daily net change of BitMEX’s insurance fund

Source: Binance Futures, Data from October 12th, 2019, to January 13th, 2020

Since the $500 million liquidation debacle, OKex has significantly built up its insurance fund to prevent future occurrences. In 2019, Okex’s insurance fund grew more than 1,000% from 156 to 2,000 BTC. The exponential increase in the size of its fund corresponded with growth in trading volumes. In the last quarter, the fund has taken a significant loss on one occasion with net outflows of 310 BTC, after volatile trading in BTC futures.

Chart 3 - Daily net change of OKex’s insurance fund

Source: Binance Futures, Data from October 12th, 2019, to January 13th, 2020

Similar to OKex, Huobi’s insurance fund had grown multi-fold in 2019. The fund has seen steady inflows since November 2019. This is due to a lull trading period in BTC markets where range-bound price movements have little effect on liquidation prices. Typically, high volatility and slippage tend to impact liquidations.

Chart 4 - Daily net change of Huobi’s insurance fund

Source: Binance Futures, Data from October 12th, 2019, to January 13th, 2020

Can Insurance Funds Outgrow Its Own Purpose?

Insurance funds can grow uncontrollably, especially when exchanges are too punitive on bankrupt traders. As explained in Part 1, exchanges are incentivized to liquidate positions better than the liquidation price, consequently generating larger inflows into the insurance fund.

Although a sizeable insurance fund adds a layer of safety, excessive insurance funds can be a sign of an aggressive liquidation mechanism. As a fund grows to a significant size, some exchanges may view it as an asset to be monetized, rather than a protection mechanism for traders.

Chart 5 compares the size of insurance funds across various exchanges against their open interest. Among all, BitMEX has the largest ratio of insurance fund to open interest, which is approximately one-third the size of its open interest. This is 3 times larger than OKex, whose fund is only one-tenth of the size of its open interest. Other insurance funds like Binance Futures are much smaller in size but have done a commendable job in protecting bankrupt accounts.

Although there is no ideal range for this metric, a high multiple suggests that an exchange is too punitive on its bankrupt traders. In contrast, a low multiple indicates that the exchange has not established sufficient financial safeguards to protect traders against adverse market movements.

Chart 5 - Insurance fund to open interest ratio

What Makes Binance Futures Insurance Fund Consumer Protection Driven?

Unlike other insurance funds, the Binance Futures insurance fund is used for what it was intended. The fund accepts risk and positions in the event of sizable liquidations to ensure that clients do not receive auto-deleverage liquidations (ADLs).

On several occasions since its inception, the fund has taken significant losses to prevent ADLs, resulting in net outflows of more than 100,000 USDT (refer to chart 6). In the last quarter, the Binance Futures insurance fund is one of the few that has seen significant outflows of more than 1% on several occasions.

Most recently, the fund saw a net outflow of 2% in the first week of January. This suggests that its insurance fund was used to cover deficits on liquidated accounts to protect both profitable and loss-making traders.

Chart 6 - Daily net change in Binance Futures insurance fund in USDT

Source: Binance Futures, Data from October 11th, 2019 to January 13th, 2020.

Traders have expressed their disappointment with system instabilities among other crypto exchanges, such as overloads, lags, clawbacks, ADLs, even complete outages. But on Binance Futures, the system has experienced zero auto-deleverage liquidations(ADLs) events as of January 13th, 2020.

Consumer-Friendly Approach

Binance Futures adopts a consumer-friendly approach. Its insurance fund accumulates contributions from liquidation fees instead of the remaining equity from bankrupt traders. With this approach, the Binance Futures insurance fund grows controllably and at the same time, provides a reasonable level of safety for its users.

As such, the aforementioned points proved to both retail and institutional traders that Binance Futures are the preferred platform for crypto-futures.

Final Thoughts

Although native cryptocurrency exchanges do not have the luxury of established and robust risk management mechanisms like traditional exchanges do, the insurance funds model provides a reasonable level of assurance to protect users.

Unlike traditional exchanges, crypto-derivative markets rely on the exchange to honor liquidations and protect users. As such, it is crucial to maintain the fund as a consumer protection feature and use it as intended.

While a sizeable insurance fund adds a layer of safety, one that is excessively large indicates aggressive liquidation practices. Hence, insurance funds should not be allowed to grow indefinitely, and exchanges must limit their size. Ultimately, the purpose of an insurance fund is to protect users. Thus, exchanges must set clear rules for liquidation in order to avoid aggressive liquidations and prevent monetization of their insurance fund.

Read the following helpful articles for more information about trading responsibly on Binance Futures:

(Support) How to Place Stop Loss Order and Take Profit Order

(Blog) How Binance Takes Responsible Trading Seriously, and You Should Too

(Blog) Crypto Spot vs. Crypto Futures Trading - What’s the Difference?

And many more Binance Futures FAQ topics...

Disclaimer: Crypto assets are volatile products with a high risk of losing money quickly. Prices can fluctuate significantly on any given day. Due to these price fluctuations, your holdings may significantly increase or decrease in value at any given moment, which can result in a loss of all the capital you have invested in a transaction.

Therefore, you should not trade or invest money you cannot afford to lose. It is crucial that you fully understand the risks involved before deciding to trade with us in light of your financial resources, level of experience, and risk appetite. If required, you should seek advice from an independent financial advisor. The actual returns and losses experienced by you will vary depending on many factors, including, but not limited to, market behavior, market movement, and your trade size. Past performance is not a guide to future performance. The value of your investments may go up or down. Learn more here.