By Lawrence Lee, Researcher at Mint Ventures

1. Introduction

Hyperliquid can be considered one of the biggest highlights in the crypto market recently, aside from AI and Meme trends. Its market-catching strategies—rejecting VC funding, allocating 70% of its tokens to the community, and redistributing all platform revenue back to its users—have drawn widespread attention. Additionally, by using its revenue directly to buy back HYPE tokens, Hyperliquid propelled HYPE’s circulating market cap to quickly surpass UNI, earning a spot among the top 25 cryptocurrencies. At the same time, this approach has driven the explosive growth of the platform’s business metrics across the board.

The purpose of this article is to describe Hyperliquid’s current state of development, analyze its economic model, and assess the current valuation of HYPE, aiming to provide an answer to the question, “Is HYPE overpriced?”

This article represents the author’s perspective at the time of publication. Future developments may lead to updates or changes in views. The opinions expressed here are highly subjective and may contain factual, data-related, or logical errors. Readers and industry peers are encouraged to critique and discuss further. However, the article does not constitute any investment advice.

A significant portion of the content presented here draws reference from the Hyperliquid report published by ASXN in September. This report, in the author’s view, is the most comprehensive and insightful analysis of Hyperliquid to date. Readers interested in a deeper dive into Hyperliquid’s mechanisms are encouraged to consult that report.

The main content of the article follows below.

2. Overview of Hyperliquid’s Business

Hyperliquid’s current business primarily consists of two segments: a derivatives exchange and a spot exchange. They also have plans to launch a general-purpose EVM in the future—HyperEVM.

Hyperliquid Architecture Source: ASXN

2.1 Derivatives Exchange

The derivatives exchange is the first product launched by Hyperliquid and serves as its flagship product, holding a central position within its entire product ecosystem.

At the core product mechanism level for derivatives, Hyperliquid has not adopted alternative innovative product logic (such as GMX or SNX) despite on-chain performance bottlenecks. Instead, it has chosen to stick with the Central Limit Order Book (CLOB), a mechanism widely used by exchanges globally and familiar to both trading users and market makers. Hyperliquid has focused its efforts on improving performance within this familiar framework.

The decentralized derivatives exchange they have built operates on Hyperliquid L1, a PoS blockchain composed of the consensus layer HyperBFT and the execution layer RustVM.

HyperBFT is a consensus algorithm modified by the Hyperliquid team based on the LibraBFT originally developed by Meta’s former blockchain team. It can theoretically support up to 2 million TPS. Supported by this robust underlying performance, Hyperliquid has brought core components of a derivatives exchange, such as the order book and clearing house, on-chain, ultimately forming its decentralized derivatives exchange architecture.

For end users, Hyperliquid’s experience is almost identical to that of centralized exchanges like Binance—not only in terms of trading experience and product structure but also in trading fees and discount rules. The only key difference is that Hyperliquid does not require KYC.

Fee Structure of Hyperliquid

In addition to its trading products, Hyperliquid has offered a Vault feature since the very beginning of its product development. Similar to the “copy trading” feature in centralized exchanges, anyone can allocate their funds into any Vault, where the Vault manager handles investments. 10% of the profits are allocated to the Vault manager as compensation. To ensure alignment of interests, the manager is required to maintain at least a 5% stake in the Vault.

Source: Hyperliquid Official Website

However, based on the current TVL (Total Value Locked), 95% of the TVL is concentrated in the platform’s official Vault HLP.

Unlike typical Vaults, HLP, being the official Vault, serves as the counterparty for a significant portion of trades on the platform. This means HLP earns a share of various platform fees, including trading fees, funding fees, and liquidation fees. From this perspective, HLP is somewhat similar to GMX’s GLP. The key difference lies in the nature of their strategies: GLP acts as the counterparty for all platform trades with a passive and transparent strategy, while HLP’s strategy is non-public. On Hyperliquid, the counterparty for a user’s trade could be either HLP or other users, and HLP’s strategy can be adjusted at any time.

Since its launch in July 2023, HLP has consistently held a net short position, providing liquidity for retail trading. This net short position has allowed HLP to remain profitable during a prolonged bull market. As of now, HLP has a TVL of 350 million and a PNL of 50 million. Based on the overall PNL curve of HLP and the PNL from the three strategy-related addresses, it is evident that the Hyperliquid team is utilizing fees to maintain a relatively positive APR (Annual Percentage Rate) for HLP.

Source: Hyperliquid Official Website

Judging from trading volume and open interest, Hyperliquid has been developing rapidly, especially over the past two months. With the $HYPE airdrop and its price continuously climbing, the platform’s various metrics reached their peak between December 17th and 20th.

Hyperliquid’s trading volume, open interest, and number of traders since 2024

Source: Hyperliquid Official Website

In the decentralized derivatives market, Hyperliquid has maintained a leading position in terms of trading volume since June of this year. Over the past two months, the gap between Hyperliquid and other decentralized derivatives exchanges has widened further, reaching a significant magnitude.

Decentralized Derivatives Exchange Trading Volume Share

Source: Dune

7-day Trading Volume Ranking of Decentralized Derivatives Exchanges

Source: DeFiLlama

From the perspective of valuation and trading volume, Hyperliquid’s most comparable counterparts are currently centralized exchanges.

Screenshot Timestamp: 2024-12-28

Source: Coingecko

The recent data for Hyperliquid shows a noticeable decline (with a peak single-day trading volume of 10.4 billion, but recent daily volumes falling below 5 billion). However, its open interest is still 10% of Binance’s, and its trading volume is 6% of Binance’s. Moreover, its open interest and trading volume are approximately 15% of Bitget and Bybit’s levels. During its peak period of popularity (December 17-20), Hyperliquid’s open interest reached 12% of Binance’s, while its trading volume reached 9% of Binance’s. Both open interest and trading volume approached 20% of Bybit and Bitget’s respective figures.

Overall, Hyperliquid has experienced rapid development as a derivatives exchange. Within the decentralized derivatives exchange space, it has already established a relatively solid leading position. Compared to leading centralized exchanges, the gap has shrunk to within 10x.

2.2 Spot Exchange

Hyperliquid’s spot exchange also operates with an order book model, maintaining consistent product architecture and fee structures with the derivatives exchange.

Currently, Hyperliquid’s spot exchange only supports native assets that conform to the HIP-1 standard of Hyperliquid and does not list tokens from other chains.

Top Market Cap Tokens on Hyperliquid Spot Market

HIP-1 (Decentralized Listing Mechanism)

HIP-1 is the token standard of the Hyperliquid network, similar to Ethereum’s ERC-20 or Solana’s SPL-20. However, unlike ERC-20 or SPL-20, creating a HIP-1 token comes with a significantly higher cost. Successfully creating a HIP-1 token also means it qualifies for listing on Hyperliquid’s spot exchange.

The HIP-1 token standard employs a Dutch auction mechanism for token creation. Specifically: Anyone can participate in the auction.The initial auction price starts at twice the final auction price of the previous round and gradually decreases linearly over a period of 31 hours to 10,000 USDC (this value is adjustable; it was previously lower before recently being revised to 10,000 USDC).The first developer who successfully bids wins the right to create a TICKER. This TICKER is then eligible for listing on Hyperliquid’s spot exchange. Auction payments are made exclusively in USDC.

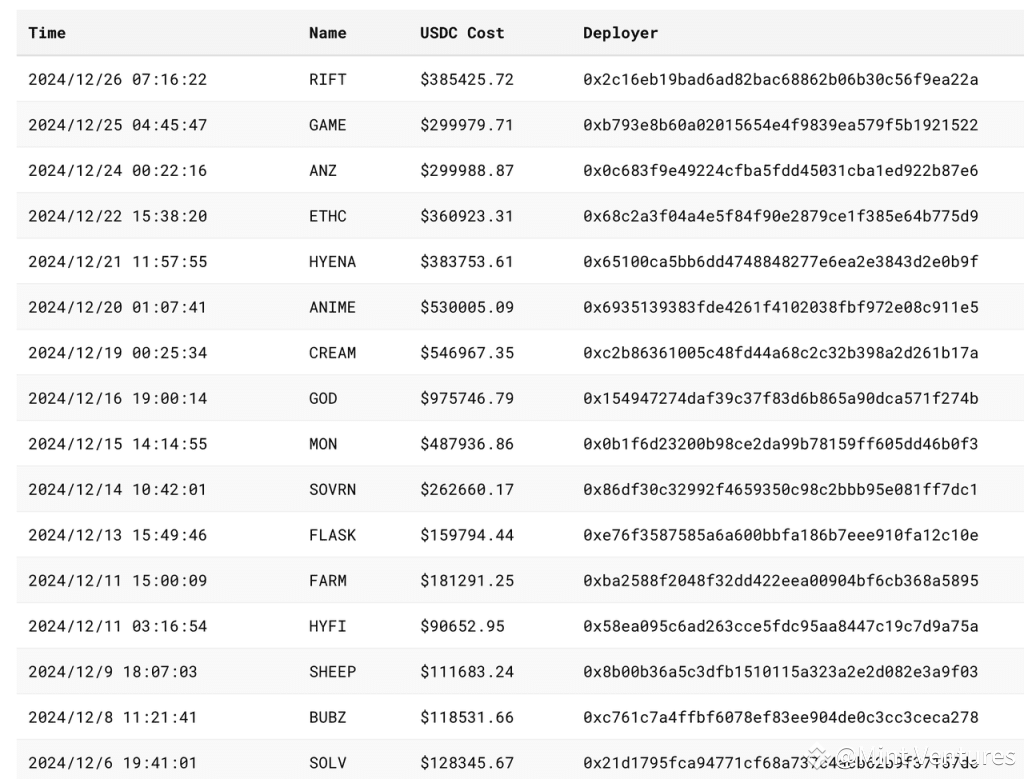

Recent Auction and Winning Prices:

Source: asxn

Among the notable TICKERs that have been created (sorted by auction price in descending order) are:

GOD: A game project invested in by Pantera.

CREAM: The veteran lending platform Cream, which has been troubled by hacks; associated with the Machibigbrother project.

ANIME: The TICKER for Azuki’s token. Rumored to have been acquired by the AZUKI team, though this has not been officially confirmed.

MON: Issued by the Pixelmoon gaming project.

SWELL: A staking and re-staking protocol in the Ethereum ecosystem.

RIFT: A gaming protocol on Virtual, created by J3ff.

GAME: Rumored to have been acquired for a game project based on Virtual, though there’s no official confirmation yet.

ANZ: A stablecoin protocol built on the Base chain.

SOVRN: Previously known as BreederDAO (a gaming asset platform invested in by a16z and Delphi in the last cycle), soon to launch a game on Hyperliquid.

FARM: An AI pet game native to Hyperliquid, launched via the Hyperfun platform.

ETHC: A mining project associated with Machibigbrother.

SOLV: A staking protocol for the Bitcoin ecosystem, backed by BN Labs, though the token has yet to be issued.

SOLV can be seen as a dividing line for HIP-1 auctions. Prior to SOLV, most auctions revolved around meme tokens and domain or symbolic logic, with the primary focus being the uniqueness of TICKERs within the ecosystem.

However, after SOLV, the focus shifted significantly, with project teams competing to secure ecological niches and listing qualifications. This shift also led to a rise in auction prices, with the highest price, GOD, fetching nearly $1 million. Most projects leaned toward generalized entertainment sectors like gaming and NFTs. However, there were also DeFi projects such as Solv, Swell, and Cream.

As a decentralized exchange, Hyperliquid’s recent month-long spot “listing fee” has stabilized at over $100,000 USD, which is comparable to the listing fees charged by some second-tier centralized exchanges.

Through HIP-1, Hyperliquid has established a transparent “decentralized token listing” mechanism. The payment required for token listing is determined by market participants, eliminating the issues of opaque listing processes seen in centralized exchanges. Moreover, the fees collected from these listings are used for HYPE token buyback and burning, which contributes to the price performance and valuation of HYPE.

HIP-2 (Hyperliquid’s AMM)

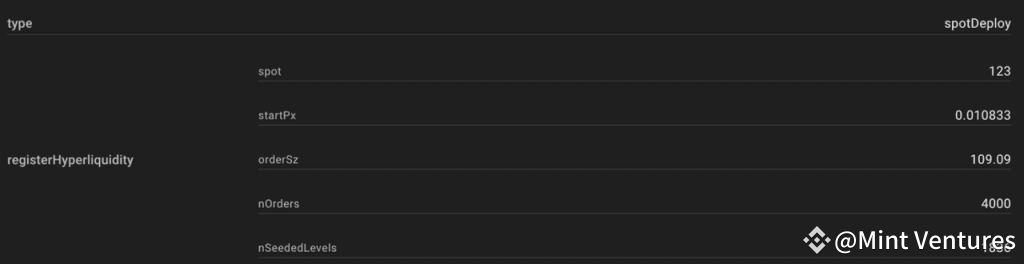

Since Hyperliquid operates its spot trading with an order book model, ensuring liquidity for new tokens is a challenge. To address the initial liquidity problem for HIP-1 tokens, Hyperliquid introduced HIP-2.

In simple terms, HIP-2 provides an automated market-making (AMM) system, allowing developers to automatically provide liquidity for HIP-1 tokens. The market-making logic involves linear liquidity provision within a specified price range. Developers can set the upper and lower bounds of the price range as well as the buy/sell dividing point. The system automatically makes markets in increments of 0.3% price changes within the specified range.

Below is an example of an order book created using HIP-2 and its parameter settings:

After the launch of HIP-2, many newly created tokens within the Hyperliquid ecosystem opted to use this AMM mechanism provided by Hyperliquid. Currently, the total USDC volume in HIP-2 has exceeded $25 million.

Hyperliquid’s average daily spot trading volume over the past 30 days is approximately $400 million, ranking it among the top ten DEXs and placing it close to the trading volumes of Curve, Lifinity, and Orca.

Source: DeFiLlama

2.3 HyperEVM

HyperEVM has not yet been launched. According to Hyperliquid’s official documentation, the current derivatives and spot exchange run on RustVM, referred to as Hyperliquid L1, while HyperEVM is simply called EVM. Based on the definitions in the official documentation, HyperEVM is not an independent chain:

Hyperliquid L1 includes a general-purpose EVM as part of its blockchain state. Importantly, HyperEVM is not a standalone chain but is secured by the same HyperBFT consensus mechanism as other parts of L1. This allows the EVM to directly interact with L1’s native components, such as the spot and perpetual order books.

The ASXN report uses the diagram below to illustrate Hyperliquid’s architecture:

Hyperliquid runs two execution layers, RustVM and HyperEVM, on a single consensus layer (HyperBFT). The core functionalities for contracts and spot trading are hosted on RustVM, which focuses on these two core dApps, while other dApps are deployed on HyperEVM.

Based on the team’s documentation, we know the following about HyperEVM:

Unlike RustVM, which currently hosts Hyperliquid’s spot and derivatives exchange, HyperEVM is permissionless, allowing any developer to build applications and issue assets (both fungible tokens [FTs] and non-fungible tokens [NFTs]).

HyperEVM is interoperable with Hyperliquid L1. For instance, L1’s native oracles can be used by HyperEVM, and certain asset transfers between the two VMs are possible. However, not all assets are transferable between them because L1 assets are “permissioned,” limited to USDC and assets generated via HIP-1, while HyperEVM accommodates a broader range of assets.

HyperEVM will use Hyperliquid’s native token $HYPE as gas, whereas L1 does not require users to pay gas fees.

The author notes that they have not encountered a product architecture like this before in the crypto world. It’s also unclear how such a structure would handle cases of DeFi composability typical on networks like Ethereum — for example, “depositing ETH into Lido to get stETH, then depositing stETH into Aave to borrow USDC, and finally using USDC to buy a meme token like PEPE.” Determining if this is one chain or two chains might depend on whether such composability is possible. From the author’s current perspective, the relationship between HyperEVM and Hyperliquid L1 might be more akin to that of an L2 with some interoperability with L1 or, as seen with centralized exchanges, the relationship between a trading platform and its EVM chain (e.g., Binance and BNB Chain or Coinbase and Base Chain).

Currently, HyperEVM’s testnet is up and running, with numerous validators participating in its testing. Notable participants include Chorus One, Figment, B Harvest, Nansen, among others.

HyperEVM Testnet Validator Node List

Source: ASXN

Since RustVM is not open to all developers, applications developed on Hyperliquid’s RustVM are relatively limited and mostly serve as trading auxiliary tools, such as: Telegram trading bot Hyperfun (token: HFUN), Telegram social trading bot pvp.trade, Trading terminal Tealstreet and Insilico and Derivatives trading aggregator Ragetrade

In contrast, HyperEVM is open to all developers, leading to many planned projects on the platform. Apart from the successful HIP-1 token projects we mentioned earlier, the diagram below and the Hypurr.co website provide a substantial list of upcoming projects.

We still need to wait for the official launch of HyperEVM to gain a clear understanding of its specific mechanisms and its relationship with Hyperliquid L1. As of now, the team has not announced a planned launch date for HyperEVM.

Summary: Hyperliquid’s overall business positioning is similar to that of leading trading groups, with its core focus on trading + L1 operations, making it a direct competitor to top trading groups. While the business model is similar, what sets Hyperliquid apart from existing leading trading groups is its decision to build its trading operations on-chain. Compared to centralized exchanges, which are permissioned and lack data transparency, Hyperliquid’s trading platform offers several key advantages: permissionless access (no KYC required), transparent and verifiable business data, better composability, and lower overall operational costs. This allows Hyperliquid to channel more revenue and profits into its native token, HYPE.

3. Hyperliquid Team, Tokenomics, and Valuation

3.1 Team

Hyperliquid was founded by two co-founders, Jeff Yan and iliensinc, who are Harvard alumni. Before entering the crypto industry, Jeff worked at Google and Hudson River Trading. The Hyperliquid team is relatively lean, with only 10 members according to ASXN’s report in September, five of whom are engineers. This is particularly impressive for a derivatives exchange with a daily trading volume surpassing tens of billions.

From the development process of Hyperliquid’s entire product, especially their dedication to self-funded research and development, building a high-performance chain from scratch to achieve a fully on-chain order book, and their highly innovative HIP-1, the team demonstrates an impressive ability to solve problems based on first principles despite its small size.

3.2 HYPE Tokenomics

The total supply of HYPE is 1 billion tokens, officially launched on November 29, 2024. Since there was no fundraising involved, there is no allocation for investors. The distribution specifics are as follows:

31.0%: Genesis allocation, airdropped to early Hyperliquid users based on their points. Fully liquid.

38.888%: Reserved for future emissions and community rewards.

23.8%: Allocated to the team, with a 1-year lockup before vesting begins. Most tokens will vest between 2027-2028, with some continuing to vest after 2028.

6.0%: Hyper Foundation.

0.3%: Community grants.

0.012%: HIP-2.

The overall team-to-community token allocation follows a 3:7 ratio. Below is the current token holder distribution:

Excluding community addresses, team addresses, and the foundation addresses, the largest token-holding address currently belongs to the Assistance Fund (AF), which holds 1.16% of the total $HYPE supply and 3.74% of the circulating supply.

At present, there are two primary sources of revenue across the Hyperliquid ecosystem: trading fees and HIP-1 auction fees. Trading fees include spot and derivatives trading fees, derivatives funding fees, and derivatives liquidation fees. Since Hyperliquid’s Layer-1 (L1) does not charge users gas fees and the HyperEVM has not yet been launched, Hyperliquid’s current revenue does not include transaction gas fees.

According to the team’s documentation:

On most other protocols, the team or insiders are the main beneficiaries of fees. On Hyperliquid, fees are entirely directed to the community (HLP and the assistance fund). For security, the assistance fund holds a majority of its assets in HYPE, which is the most liquid native asset on Hyperliquid L1.

All fees are allocated entirely to HLP and AF . However, the team has not explicitly disclosed the exact distribution ratio between HLP and AF.

Fortunately, since Hyperliquid L1 data is publicly accessible, we can refer to the analysis by @stevenyuntcap. Based on their calculations as of early December, Hyperliquid has subsidized HLP with a total of 44 million, while the initial funding allocated to AF for purchasing HYPE was 52 million. This suggests that Hyperliquid’s total cumulative revenue from its launch to early December amounts to $96 million, with the protocol’s revenue split between HLP and AF at a ratio of 46%:54%. (Additionally, using the cumulative trading volume of $428 billion over this period, we can estimate that Hyperliquid’s average derivative trading fee rate is approximately 0.0225%.)

Since AF currently uses all its USDC to repurchase HYPE, we can simplify the revenue model as follows: 46% of Hyperliquid’s perpetual contract trading income is distributed to the supply side (HLP holders), while 54% is used to buy back $HYPE tokens.

Beyond revenue from perpetual contract trading fees, there are two additional income streams in the future that will benefit HYPE holders: HIP-1 auction fees and the USDC portion of spot trading fees. Currently, both revenue streams are fully allocated to AF for HYPE buybacks (this also includes the HYPE portion of trading fees from HYPE-USDC spot transactions, which are directly burned instead of repurchased, with a total of 110,000 HYPE tokens burned to date).

AF’s current strategy remains to periodically use all accumulated USDC to buy back HYPE. Therefore, we can simplify profit tracking by monitoring AF’s USDC inflow data, which reflects Hyperliquid’s profitability and its repurchase pressure on HYPE. According to data from hyperdata.info, AF has accumulated over 77million in USDC inflows, with over 25 million inflows in the past month alone, translating to an average daily buyback of approximately $1 million worth of HYPE.

On December 30, 2024, Hyperliquid officially launched the HYPE staking feature. Currently, the annual staking yield for HYPE is approximately 2.5%. This yield solely includes the fixed reward from the PoS consensus layer, with its consensus-based yield rate modeled after Ethereum’s consensus layer yield mechanism (where the yield rate is inversely proportional to the square of the total amount of staked HYPE). As of now, aside from the 300 million tokens held by the team and the foundation, nearly 30 million user-owned tokens have also been staked.

Looking ahead, the economic model of HYPE still has room for numerous potential adjustments, such as:

Launch of HyperEVM,

$HYPE being used as gas for HyperEVM,

Allocation of execution layer revenue to HYPE stakers (currently, HYPE staking rewards only include consensus layer rewards),

Redistribution of transaction fees to $HYPE holders,

Transaction fee discounts for $HYPE stakers.

3.3 Valuation

Below, we will explore two valuation frameworks for Hyperliquid. Before diving in, it is important to note:

Extreme fluctuations in Hyperliquid’s data: Metrics such as market capitalization, TVL, revenue, and user numbers have experienced massive changes recently. For example, in the past month alone, these metrics saw multiple-fold or even tenfold increases, followed by a 50% pullback. The volatility of these indicators far exceeds the comparative valuation parameters listed below. As such, the following valuation frameworks are better suited for long-term reference.

Currently, HYPE’s price constitutes the most critical fundamental aspect of Hyperliquid. Much of the sharp growth in metrics is a result of the rise in HYPE’s price, rather than the other way around.

Framework 1: Comparison with BNB

The key thesis for Hyperliquid, as proposed by Messari, is that it could become the “on-chain Binance.”

This analogy is overall quite reasonable and could indeed serve as an appropriate framework. Binance/BNB likely represents the most suitable comparison for Hyperliquid/HYPE:

Core business: Hyperliquid’s core operations focus on derivatives and spot trading, which align with Binance’s primary business model.

HyperEVM vs. BNBChain: While HyperEVM has yet to launch, both HYPE and BNB share similarities, as they can be used as gas on their respective EVM chains and staked for rewards.

Transaction Fee Benefits: Both HYPE and BNB benefit directly from platform transaction fees.

Below, we will compare Hyperliquid’s derivatives exchange, spot exchange, and EVM layer by dividing its structure into these three components, drawing comparisons to Binance.

Derivatives Exchange

As mentioned earlier, Hyperliquid’s recent metrics for open interest and trading volume reached around 10% of Binance’s corresponding data. Therefore, we can roughly assume that in the derivatives exchange module: HYPE = 10% of BNB.

Spot Exchange

Hyperliquid’s average daily spot trading volume over the past 30 days is approximately 400 million, while Binance′s average daily spot trading volume is about 26 billion.Therefore, in the spot trading market:HYPE = 1.5% of BNB.

EVM

Based on the reasoning above, we conclude that the relationship between HyperEVM and Hyperliquid L1 is akin to the relationship between Binance Exchange and BNBChain.

Although HyperEVM has not yet launched, it’s unclear how much TVL will migrate from RustVM to HyperEVM. However, considering the product architecture and corresponding user experience, the overall logic is still based on migrating Hyperliquid’s existing exchange users to the chain.To provide a comparison, we reference Binance and Coinbase’s data. Considering the market’s enthusiasm for HYPE, we assume 10% of the exchange’s TVL will migrate on-chain (this is an optimistic estimate, especially since most articles using TVL valuation assumptions presume 100% of Hyperliquid’s TVL will migrate to HyperEVM). Based on this calculation: HYPE = 3% of BNB.

Economic Model

In addition to the above, we also need to consider the differences between the economic models of HYPE and BNB.

From the analysis of HYPE’s economic model mentioned earlier, it can be seen that HYPE currently converts 54% of the platform’s gross profit and 100% of its net profit into buybacks or token burns for HYPE.

BNB, on the other hand, previously followed the whitepaper’s guidelines, allocating 20% of Binance’s net profits for BNB buybacks. However, since 2021, after buybacks and burns were decoupled from the platform’s net profit, we can no longer determine the proportion of Binance’s net profits benefiting BNB. Nonetheless, based on the trend of burn data and Binance’s market position during the same period, the proportion of net profits allocated to burns appears to have remained at a similar level.

From the perspective of the economic model benefiting token holders, HYPE is significantly superior to BNB.

Source of BNB Burn Data

It is also worth mentioning that Hyperliquid currently directs 54% of its revenue toward the HYPE token, and this percentage still has room for further growth. Due to the underlying mechanism, since July 2023, during a bull market in which BTC has risen by over 200%, HLP has maintained substantial short positions on cryptocurrency, using USDC as collateral. Although HLP’s strategies have been well-executed and have managed to maintain a rare breakeven, it still incurs an annualized APR of over 30% to retain funds within HLP.

HLP Historical Net Positions

Source:Hyperliquid Official Website

In the future, as the market gradually reaches its peak, the overall trend of crypto users being net long in derivatives is unlikely to change. However, the probability of HLP’s strategy yielding higher returns increases during sideways or bear markets (as observed in the historical returns of GMX’s GLP and GNS’s Vault). As a result, Hyperliquid may no longer need to allocate such a high proportion of its revenue as “rental payments” to HLP. This suggests that Hyperliquid’s net profit margin has room for further growth.

Speaking of net profit margins, while we are unable to determine Binance’s exact net profit margin, we can gain some insights into the operating costs of centralized exchanges from the reports of publicly-listed company Coinbase.

Coinbase quarterly report 24Q3

In 2023, Coinbase’s operating expenses (including R&D, administrative, sales, and transaction fees) averaged over $600 million per quarter, which was roughly equivalent to its total revenue, leaving its net profit margin near 0%. In 2024, as the market experienced a boom, Coinbase’s net profit margin improved significantly but still remained below 30%.

From the above numbers, we can clearly observe the relative advantage of Hyperliquid’s profit margin (economic model) compared to centralized exchanges. This can also be illustrated through a specific example: the handling process of token listing.

For centralized exchanges, the token listing process typically involves a dedicated team. This team is responsible for tracking market trends and negotiating with project teams, enabling the exchange to charge listing fees and/or receive project tokens. Centralized exchanges must also cover the substantial salaries and bonuses of the listing team, in addition to paying internal control teams tasked with monitoring and mitigating potential conflicts of interest during the token listing process.

In contrast, Hyperliquid’s HIP-1 token listing process, as previously mentioned, runs entirely via pre-programmed code. This automation drives the operating cost for new token listings almost to $0, allowing the listing revenue (e.g., “listing fees”) to be fully distributed to HYPE token holders.

To summarize, as of the end of December 2024, we have the following comparisons:

Derivative Trading: HYPE = 10% of BNB

Spot Trading: HYPE = 1.5% of BNB

EVM (Estimated): HYPE = 3% of BNB

Economic Model: HYPE significantly outperforms BNB

Circulating Market Cap: HYPE = 9% of BNB

Fully Diluted Market Cap: HYPE = 27% of BNB

Since derivative trading is currently Hyperliquid’s primary business, it should carry more weight in valuation comparisons. In the author’s view, although HYPE’s current market cap cannot be considered cheap, it is also not overpriced.

Framework 2: PS HYPE incorporates a token buyback and burn mechanism, both directly impacting the HYPE token itself. Therefore, the PS ratio can be used for valuation. The specifics are as follows:

Derivative Trading Fees:

Using an average contract trading fee of 0.0225%, with profits distributed between HLP and AF in a 46:54 split, projections are made as follows:

The monthly derivative trading revenue for Hyperliquid is: 154.7 billion USD×0.0225%=34.8 million

Out of this, 54% (approximately 18.79 million USD) enters the AF fund to buy back HYPE. This translates into an annualized net profit of 225.5 million USD.

HIP-1 Auction Fees:

Over the past month, the HIP-1 auction fee revenue was 6.1 million USD. Based on the 46:54 split between HLP and AF, this corresponds to an annualized net profit of 39.5 million USD.

Spot Trading Fees:

The fee structure for Hyperliquid’s spot trading is the same as for derivative trading, with the USDC portion of fees being distributed similarly—46% to HLP and 54% to AF. In spot trading, fees for other tokens (e.g., in HYPE-USDC trading, where HYPE buyers pay USDC fees and HYPE sellers pay HYPE fees) are directly burned.

Therefore, the net profit from spot trading fees contributing to HYPE can be divided into two parts:

HYPE Portion: This can be directly queried through a blockchain explorer. It has been exactly 30 days since the HYPE token’s TGE, during which 110,490 HYPE tokens were burned. Annualizing this, the burn amount would be 1,325,880 tokens, which, at the current price, is approximately 37 million USD.

USDC Portion: Over the past 30 days, Hyperliquid’s spot trading volume reached 11.5 billion USD. The portion of spot trading fees used to buy back HYPE equals: 11.5 billion USD×0.0225%×54%=1.397 million. Annualizing this, the net profit amounts to 16.77 million USD.

Combining the above three sources of revenue and calculating annualized values based on the past month’s data, the total amount used for HYPE buybacks is 318.77 million USD.

Using the circulating market cap, HYPE’s P/S ratio is 29.4. Using the fully diluted market cap, HYPE’s P/S ratio is 88.

Finally, we’ve compiled the P/S ratios for some crypto projects that are somewhat comparable to Hyperliquid.

It can be observed that the P/S valuation of L1 is significantly higher than that of applications, while the P/S valuation of Hyperliquid is noticeably lower compared to other comparable L1s.

The following outlines two frameworks for evaluating HYPE. It is important to emphasize the following points:

Hyperliquid’s data is highly volatile—key metrics such as its market capitalization, TVL (Total Value Locked), revenue, and user data have experienced several-fold or even tenfold growth in the past month, only to subsequently see a 50% retracement. The dramatic fluctuations of its metrics far exceed the comparisons shown in the valuation indicators outlined below. Therefore, the valuation frameworks discussed above are more suitable as long-term valuation references.

The current price of HYPE is the most significant fundamental factor for Hyperliquid. The surge in its various metrics is more a result of HYPE’s price increase, rather than an indication that “Hyperliquid achieved such impressive data, which then led to this price.”

4. Risks

Hyperliquid currently faces the following risks:

Capital Risk: At present, all of Hyperliquid’s funds are stored in the Arbitrum network bridge. The security of this smart contract, as well as the safety of the 3/4 multi-signature system managing all the funds, is absolutely critical.

Code Risk: This includes risks associated with both its current L1 infrastructure and HyperEVM. Hyperliquid utilizes innovative architecture and consensus mechanisms. While its decision not to open source its L1 at this stage reduces the likelihood of attacks, as Hyperliquid scales and HyperEVM goes live, the potential risks of attacks or code vulnerabilities will increase.

Oracle Risk: Oracle risks are an inherent challenge faced by all derivatives exchanges.

Regulatory Risk Leading to Loss of Competitive Advantage: The absence of KYC requirements is currently one of Hyperliquid’s key advantages compared to centralized exchanges. However, as the platform continues to grow, it may encounter regulatory demands, such as anti-money laundering compliance, which could erode its comparative advantage.

References

https://hyperfnd.medium.com/hype-genesis-1830a4dc2e3f

https://newsletter.asxn.xyz/p/hyperliquid-the-hyperoptimized-ord

https://data.asxn.xyz/dashboard/hl-auctions

https://hypurrscan.io/stats

https://hypurrscan.io/token/0x0d01dc56dcaaca66ad901c959b4011ec

https://www.hypeburn.fun/

https://www.prestolabs.io/research/hyperliquid-the-hype-begins#4.1-Decentralization

https://x.com/0xak_/status/1871051318267445562

https://x.com/Darrenlautf/status/1869961681671184629

https://x.com/stevenyuntcap/status/1863643385002652044

https://hyperdata.info/