Even before Trump officially takes office, the crypto market has already celebrated in advance, cashing in on policy news. This morning, following Trump's official nomination of Paul Atkins as SEC Chair, Bitcoin surged past $100,000. Since Trump's election victory, Bitcoin has risen from $68,000 on November 5 to $100,000, achieving a 47% return in just one month. In this article, the author will deeply analyze how policy changes shape market dynamics from the perspective of U.S. crypto policy and the future potential directions in this new landscape.

The 'tough and harsh' crypto regulation is shifting towards being more open and friendly.

During his campaign, Trump made ten crypto-friendly commitments to the crypto market, including establishing a strategic Bitcoin reserve. The nominated SEC Chair Paul Atkins is also known for his friendly stance towards cryptocurrencies, advocating for reduced regulation to support market innovation. Trump mentioned today that Paul understands the importance of crypto assets and other innovations for making America greater than ever and believes in the commitment to strong, innovative capital markets. Paul has also criticized the SEC's hefty fines as detrimental to shareholder interests, advocated for flexible regulatory strategies, and co-chaired the Token Alliance. Trump's actions leverage Paul Atkins' prior experience in promoting crypto to shift the SEC's previous punitive approach towards the crypto industry, bringing the idea of 'financial freedom' into U.S. financial regulatory agencies.

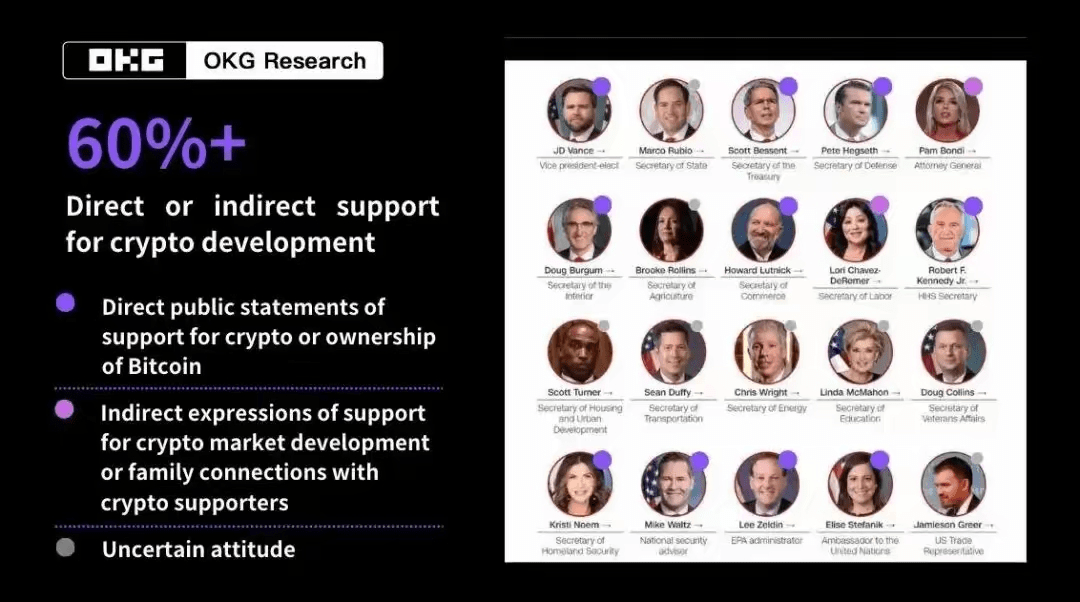

In addition, other members of Trump's team have also provided strong support for the regulation of crypto finance: over 60% of nominated cabinet members have publicly stated they own Bitcoin or support the development of crypto finance or indirectly support the growth of crypto assets.

In addition to Trump's commitments in the crypto market and the previously proposed (Financial Innovation and Technology Act of the 21st Century) (FIT 21 Act), the recent Tornado Cash event also marks that U.S. crypto regulation is moving towards a more open and friendly direction. At the end of November, the Fifth Circuit U.S. Court of Appeals ruled that the Treasury's sanctions against Tornado Cash's immutable smart contracts were illegal, stating that these smart contracts do not meet the legal definition of 'property.' This ruling provides significant support for the legitimacy of smart contracts, allowing developers and users to use these protocols without facing direct conflicts with traditional legal frameworks, thus promoting finance to develop in a more inclusive, friendly, and free direction, which directly benefits the flourishing of decentralized finance (DeFi).

'America First' requires both industry and financial capital to be freer.

Financial freedom not only opens up greater development space for the crypto market but also signals a profound market consolidation brewing after the integration of crypto assets with traditional financial assets (TradFi). As the digital society develops, propelled by future technologies such as artificial intelligence (AI), the way value is created is accelerating its transformation. Former Alibaba strategist Chen Ming has pointed out that General Artificial Intelligence (AGI) will become a core technological breakthrough in future productivity, closely intertwined with crypto assets, giving rise to a multitude of new digital assets.

Blockchain, as a value network technology connecting the digital society and the real world, will play a key role for crypto assets in this transformation. Driven by the 'America First' policy, Trump proposed an AI version of the 'Manhattan Project,' intending to elevate AI technology to a national strategic level and vigorously promote the industrialization process.

In addition to the fact that the future digital society driven mainly by AI cannot avoid crypto assets, Standard Chartered has also stated that almost any real asset in the real world can be tokenized, predicting that by 2034, the global demand for tokenized assets will reach $30 trillion. Whether for the future development needs of the digital society or the asset circulation needs of the real society, the integration of crypto assets with traditional financial assets holds a market potential that far exceeds the 'Great Merger Era' of the 1930s and the 'Internet Merger Era' of 2000, with the former spawning $600 billion in industry consolidation and the latter driving the market size to $3 trillion.

The integration process is now unstoppable. Whether it is the promotion of crypto asset ETFs or the emerging sectors represented by RWA (Real World Assets), just the stablecoin application alone has created a market value of over $200 billion. With the continuous penetration of crypto technology, the entire financial market's 'cryptofication' process has already begun, reshaping the global financial landscape and fostering a newer, more open, and integrated capital ecosystem.

The 3 Key Crypto 'Promises' and Their Impact on the Market

Whether announcing the establishment of a strategic Bitcoin reserve or nominating a crypto-friendly SEC chair, Trump's election seems to usher in the most favorable regulatory environment for the crypto industry in history, thereby opening up Bitcoin's recent upward channel. However, in the medium to long term, the true driving force pushing the crypto industry forward is clearly not the price of Bitcoin, but rather whether Trump can fulfill those verbal crypto commitments and begin to provide more space for the crypto market from the legislative level. If Trump can leverage his high standing within the party and the Republican Party's sweeping victory in both houses of Congress to actively promote key legislation represented by the following three major acts, it may lead to a new situation for the crypto industry.

The FIT 21 Act will be prioritized, bringing DeFi innovation 'back' to the U.S.

The FIT 21 Act may be a priority for Trump after taking office. This act, hailed as 'the most important' crypto legislation to date, not only clearly defines when cryptocurrencies are commodities or securities but will also end the 'tug-of-war' between the SEC and CFTC in crypto regulation. The U.S. House of Representatives previously passed the act with an overwhelming majority and submitted it to the Senate, but the latter has not taken decisive action. However, with Trump in office, the market generally expects the process of this act to accelerate.

After the passage of the FIT 21 Act, more compliant trading platforms and publicly listed crypto companies will emerge, and clear property standards will enrich the tradable tokens, providing new opportunities for spot ETFs and other crypto financial products. One reason for the difficulty in approving Ethereum ETFs was the ambiguity in classification; for a long time, the SEC considered Ethereum after converting to a PoS mechanism to be more like a security. It was only after the SEC and Wall Street found a 'balance point'—clarifying that unstaked Ethereum ETFs are not securities—that progress could continue. After the act passes, cryptocurrencies clearly classified as 'digital commodities' will find it easier to launch spot ETFs and related financial products, and we may see more varieties of cryptocurrencies like SoL, XRP, HBAR, and LTC in spot ETFs next year.

Several institutions have already submitted Solana ETF applications.

The FIT 21 Act will also promote innovation in decentralized applications, particularly in the DeFi sector. The FIT 21 Act clearly states that relevant tokens deemed decentralized and functional will be considered digital commodities and not subject to SEC regulation, and as long as the degree of centralization meets the requirements, they can obtain a certain exemption period, encouraging more DeFi projects to evolve towards a more decentralized direction. The act also requires the SEC and CFTC to study the development of DeFi, assess its impact on traditional financial markets, and potential regulatory strategies, and the exemption period will attract more DeFi projects to 'return.'

Furthermore, driven by friendly policies and expectations of interest rate cuts, more traditional funds will flow into DeFi seeking higher yields, thus stimulating further innovation in DeFi. A clear trend is that DeFi will continue to expand collateral assets, bringing more off-chain liquidity on-chain. This will promote the deep integration of DeFi with RWA by allowing tokenized assets such as U.S. Treasury bonds and real estate to be used for collateral or lending operations, enriching the combinability and imaginative space of on-chain finance and allowing the influence of DeFi to spread off-chain. The RWA sector will also benefit from this integration, leading to more considerable returns and accelerating the bidirectional expansion from off-chain to on-chain.

The value of DeFi in the Bitcoin ecosystem should not be overlooked. While penetrating off-chain through ETFs, Bitcoin is also showcasing more possibilities in the on-chain ecosystem. Considering that the Bitcoin market is dominated by long-term holders, and the spot ETF keeps the market liquidity at a lower level, the resulting Bitcoin lending sector may usher in new opportunities. Given the SEC's probability of allowing staking for Ethereum spot ETFs, staking projects in the DeFi ecosystem are likely to gain widespread attention.

U.S. stablecoin-related legislation is back on the agenda.

In 2023, the U.S. House Financial Services Committee passed the (Payment Stablecoin Clarity Act) but did not receive approval from the House. In October of this year, crypto-friendly Senator Bill Hagerty reintroduced a similar draft. Coupled with Trump's previous promise not to promote a CBDC issued by the Federal Reserve, and the FIT 21 Act defining licensed payment stablecoins and emphasizing the importance of licensing, stablecoin-related legislation may be reconsidered after Trump takes office.

Stablecoin legislation will directly affect the issuance of USD stablecoins and related payment institutions. Some smaller or algorithmic stablecoins may be forced out of the market, while legitimate stablecoins (like USDC) will capture a larger market share. Meanwhile, as legislation clarifies compliance requirements, traditional payment service providers will accelerate the adoption of compliant stablecoins, enhancing their availability and usability in daily transactions. Relevant companies and users will also be more comfortable accepting stablecoins as a complement to the existing payment system rather than solely for cryptocurrency trading use cases. The market share of stablecoins in cross-border transfers and settlements will continue to rise, with user volume and settlement scale likely to approach or even surpass institutions like Visa.

Moreover, whether directly gaining returns through underlying assets (such as government bonds, money market funds, etc.) and distributing them to relevant participants, or obtaining on-chain returns through DeFi protocols, various yield products based on compliant stablecoins will continue to emerge and gain favor among users. However, care should be taken to avoid making stablecoins exhibit characteristics of investment contracts when designing yield mechanisms.

The repeal of the SAB21 proposal is expected to be restarted, solving the issue of crypto asset custody.

Whether it's the development of crypto financial products like spot ETFs or the growth of RWA, stablecoins, and DeFi, demand for crypto custody services will surge. This will compel the restart of the repeal of the SAB 121 (Staff Accounting Bulletin No. 121) proposal. SAB 121 was issued by the SEC in 2022, requiring companies to account for custodial crypto assets as liabilities, which significantly increased companies' asset-liability ratios, affecting financial health and credit assessments, making relevant firms reluctant to provide custody services.

Trump promised during his campaign to repeal this announcement after taking office. The most direct benefit of repealing SAB 121 is to reduce the compliance burden on crypto custody institutions, allowing banks and other regulated entities to more easily enter the crypto custody space, thus attracting more institutional investors into the market. Due to the accounting treatment requirements of SAB 121, many banks and financial institutions had previously been relatively cautious regarding crypto financial products like spot ETFs; the repeal will reduce the complexity of managing these crypto assets for financial institutions. Stablecoin providers and payment-related businesses are also affected, especially those projects integrated with traditional financial systems. Repealing SAB 121 could create a more favorable regulatory environment for these companies, assisting in the development of core functions such as payments and settlements. The currently popular narrative around RWA will benefit from this, enabling more traditional custody institutions to manage tokenized assets more flexibly, thus attracting more financial institutions willing to participate.

Undeniably, every step of crypto-friendly policies in the Trump 2.0 era is profoundly reshaping the boundaries of the crypto market. From regulation to accounting standards, every seemingly minor change hides far-reaching strategic significance. The nomination of Paul Atkins signals a more relaxed crypto regulatory environment, and the institutional reforms at the asset level should not be overlooked. The new FASB regulations (ASU 2023-08), which will come into effect on December 15, 2024, require businesses to record their held crypto assets at fair value. This means that changes in the value of assets like Bitcoin held by companies will directly reflect in their financial statements, significantly impacting net income. The implementation of this rule will incentivize more companies to include mainstream crypto assets like Bitcoin on their balance sheets. Additionally, Microsoft will hold a board meeting on December 10 to formally discuss whether to include Bitcoin in its corporate strategic reserves, providing a high-recognition industry signal for this trend.