The international foreign exchange market has always been the main battlefield in the financial war between China and the United States. If A-shares in recent years have impressed all global investors, then the performance of the offshore RMB exchange rate market has been a bit disappointing.

However, there is a huge disagreement in the market as to whether the depreciation of the RMB is passive or active. Everyone has different views. For foreign exchange speculators, unilaterally betting on the long-term depreciation and appreciation of the RMB is a thankless task. However, for the country and foreign trade companies, the depreciation of the RMB can indeed offset the negative impact of tariffs.

Does the depreciation of the RMB exchange rate mean that the United States has once again gained the upper hand in this financial war? What profound impact does the depreciation of the RMB have on the prices of Chinese assets?

The stronger the dollar, the sooner the recession will come

On December 2, Federal Reserve Board Governor Waller said at a seminar that he personally preferred the Fed to continue cutting interest rates in December because the current monetary policy was restrictive enough to put downward pressure on inflation.

In other words, even if the Federal Reserve cut interest rates by 25 basis points in December, the overall interest rate level will remain high. Such a high interest rate will still enable the US inflation data to continue to decline.

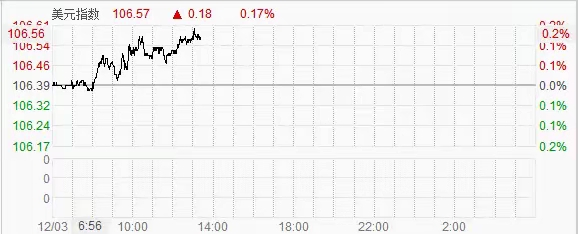

Faced with the Fed's expectations of a rate cut, the foreign exchange market clearly did not take the speech seriously, and the US dollar index continued to perform strongly after the Chinese market opened. The active depreciation of the US dollar directly caused the RMB exchange rate to fall below the key node of 7.3.

It is obvious that the speech made by Federal Reserve Board Governor Waller yesterday was intended to cool down the strong dollar, because in the past two months, investors on Wall Street have been trading that the dollar will return to a strong position after Trump takes office.

A strong dollar market is what the Federal Reserve wants to see, but if it is too strong, it is not a result that any central bank wants to see.

But it is obvious that since Trump won the election, the Federal Reserve's influence on the financial market has been relatively weak, and the market's main attention is still focused on what Trump said, who he will impose tariffs on, and what tweets he sent at night.

The trading side tries not to miss any opportunity to trade Trump policies.

But even Trump himself probably doesn’t know what kind of monetary environment he needs. But in any case, a strong dollar is not conducive to US exports. In addition, a high-interest monetary policy is not conducive to the recovery of the US manufacturing industry.

In summary, the market's current reaction seems to be trading on the success of Trump's policies, but it is actually increasing the difficulty of implementing Trump's policies.

The strength of the US dollar is basically superficial. In essence, it is still guiding global hot spots into the US market through policy expectations and interest rate hike expectations, thereby promoting the appreciation of the US dollar.

However, in the trade settlement market, the stronger the dollar, the greater the risk of holding it. There is no way to talk about the repatriation and rise of the US manufacturing industry, and the hollowing out will become more and more serious.

For the capital market, since holding US dollars and putting money in American banks can make easy money, why bother to invest in real industries?

Fed's losses widen

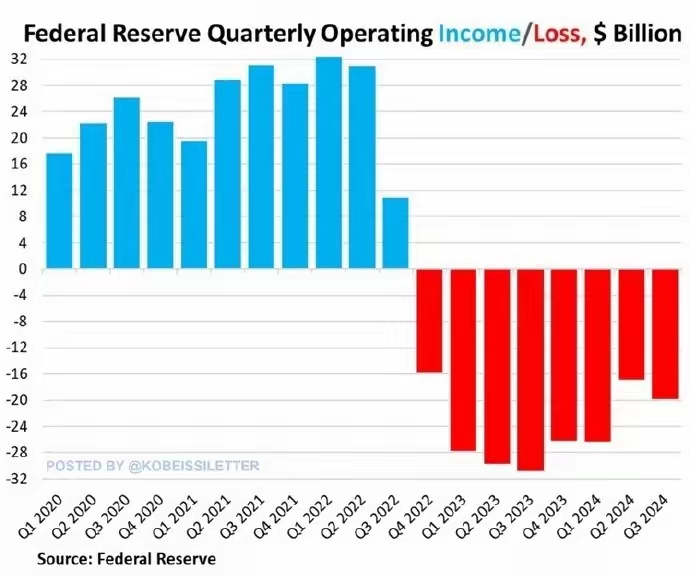

On December 1, the Federal Reserve released a report stating that the US dollar lost $19.9 billion in the third quarter of 2024. Compared with the loss of $16.9 billion in the second quarter, the interest rate cut did not reverse the Federal Reserve's operating conditions, and the loss margin continued to expand.

This is the 32nd consecutive month that the Federal Reserve has been losing money, with the cumulative loss reaching $210 billion. The reason for the loss is that the Federal Reserve has been paying hundreds of billions of dollars in interest to banks and the money market.

At the same time, the continued decline in U.S. Treasury prices in the third quarter of 2024 is also one of the main reasons for the expansion of the Federal Reserve's losses.

Compared with the weakening of the RMB in the overseas offshore exchange rate market, the problems faced by the Federal Reserve and the US dollar are more urgent, so after Trump's victory, this round of Sino-US financial war will be so fierce.

In other words, with the continuous shrinking of the US dollar market, the decline in US bond prices, and the Federal Reserve's losses, all these signs indicate that there is not much time left for Trump and the Federal Reserve.

Today, the offshore RMB fell to the 7.31 warning line, setting a new low this year. Many traders believe that under the inertia of depreciation, the offshore RMB exchange rate may depreciate to around 7.35 in a short period of time.

Faced with the rapid depreciation of the RMB, although the central bank has not taken obvious action, it has released a signal that it does not want the RMB to depreciate too quickly, but the sense of urgency is not very strong.

The main reason is that this round of RMB depreciation is still in a stable range compared with other basket of currencies.

In the foreign exchange market, currencies such as the euro and the pound have depreciated even more.

Therefore, there is no need for China to take any forced action, but the RMB exchange rate midpoint set today is stronger than the market expectation of 695 points.

In other words, although the RMB has fallen below 7.31 against the US dollar in the offshore foreign exchange market, when foreign trade companies use the US dollar to exchange RMB at the central bank, the official exchange rate is still stable at around 7.2.

Trade is trade, speculation is speculation.

For this, we can understand that in the face of Trump's Tariff 2.0 that will be introduced in 2025, the active depreciation of the RMB will help offset the impact of US tariffs on the world.

In short, this round of RMB depreciation will not have a big impact on China's economy and RMB assets.

The performance of RMB assets in recent years has already demonstrated the market’s choice.

What is different from the past is that A-shares have not been greatly affected in this round of RMB depreciation. In other words, the RMB depreciation was not caused by a large outflow of domestic funds.

After the announcement of Trump's tariff policy, A-shares began to trade as negative news came to an end. The Shanghai Composite Index rose against the trend from 3,200 points to above 3,350 points, and this trend has not ended.

In addition, Chinese government bonds have also been subject to massive buying sprees, with the price of 10-year Chinese government bonds rising sharply and the yield falling below 2% yesterday.

According to media reports, an important economic meeting will be held on December 11-12, when China will announce more economic and monetary policies.

The Federal Reserve will hold an interest rate meeting from December 17 to 18, after which the Federal Reserve will announce the latest monetary interest rate policy.

These important meetings will determine the direction of the global economy in 2025. The market is trading or pricing in advance the expected impact of policies on the economy. #XRP市值重回第三