November 22, 2024, The First Issue of New Coin People's Daily.

Previously I wrote several hundred issues of Coin People's Daily, and now I am starting a new Coin People's Daily, planning to write 100 issues to completely stop, to commemorate this bull market.

Today I saw a piece written by Mindao on Twitter about MicroStrategy, which I think is a great popular science article, so I decided to move it here for everyone to see.

Part One: The State of the World, What Is the Current Situation — Nangong Yuan

1. Trump came to power, openly supporting Bitcoin and other cryptocurrencies; the richest man, Musk, allied with Trump, bringing Dogecoin in a strong assault.

2. Bitcoin mining and production of Bitcoin mining machines, once controlled by China, have decentralized globally under government crackdowns.

Once controlled by China, digital currency trading has been scattered globally under government crackdowns, achieving de-China-ization.

Under these two premises, American capital has strongly intervened in Bitcoin and other digital currencies.

Previously, American capital was secretly purchasing Bitcoin mined in China. Back then, Bitmain's boss, Mr. Wu, once lamented on Weibo that Americans regularly purchased large amounts of Bitcoin from him at around 3000 RMB each. I saw and remembered this Weibo post.

3. The Bitcoin and Ethereum EFTs have provided traditional capital with a channel to enter the cryptocurrency market.

4. MicroStrategy MSTR is maneuvering the conversion of stocks, cryptocurrencies, and bonds, becoming the largest buyer of Bitcoin currently.

Part Two: Mingdao Yang Talks About MicroStrategy

Today let's talk about the big strategy of MicroStrategy.

MicroStrategy has really played out the biggest golden egg in the crypto circle this cycle, with a face value profit exceeding $15 billion in less than two years.

It is not just a triple arbitrage of stocks, bonds, and cryptocurrencies; the key is turning MSTR into a real Bitcoin in traditional finance (recently MSTR's trading volume surpassed the total of Bitcoin ETFs), a true masterpiece of 'borrowing a false pretext to achieve the real.'

Michael Saylor is neither from a Wall Street blue-blood background nor a crypto OG, he is truly a case of a wild punch killing the master.

I would like to discuss a few key parts of his trading structure design:

Stock/Crypto Relationship

These two have two key flywheels. One is stock premium issuance, purchasing Bitcoin, driving Bitcoin prices up, enhancing its net asset value and earnings per share, which is linear leverage;

The second flywheel is financing to buy cryptocurrencies, accelerating profit growth, and expanding valuation multiples (p/b, p/e increases), leading stock prices to leap from linear to exponential leverage, with market value and stock price increases surpassing the rise in Bitcoin prices themselves.

Stock/Bond Relationship

MSTR's market value increases, pushing it into more indices, resulting in more trading derivatives, increasing trading volume, and lowering the financing costs for stocks and bonds, with a structure that can be both bonds and stocks, further reducing the overall debt ratio.

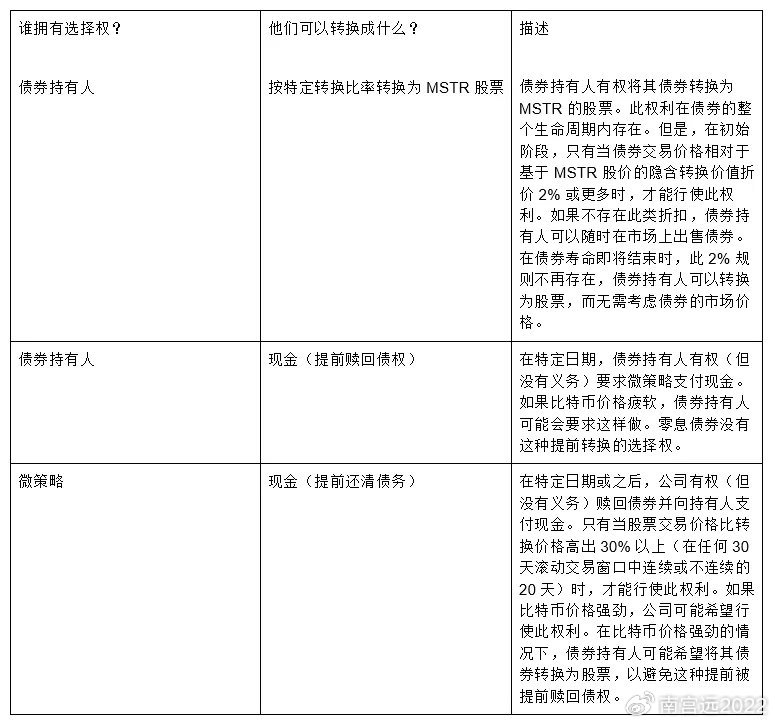

MicroStrategy's convertible bonds are also a very delicate design (full of Buffett's wisdom).

Convertible bonds are basically medium to long-term bonds (5-year term, spanning at least one crypto cycle), most of them are zero-interest, with no principal repayment during the period. This ensures there is no partial repayment or interest payment pressure during this period, further reducing the risk of debt default caused by the downward spiral in cryptocurrency prices.

What’s more impressive is that, unlike traditional convertible bonds, the choice of converting to stock or cash repayment lies with MicroStrategy, not the convertible bondholders, fundamentally avoiding the default issue if the convertible bonds cannot be repaid at maturity (in the worst-case scenario, they can be fully converted to stock). This financing premium capability is extraordinary.

Although many people generally believe that issuing bonds increases the debt ratio and raises risk premiums, which is unfavorable for stock prices, this type of convertible bond essentially gives complete control to MicroStrategy's 'can be debt or stock' tool. It is very friendly to stock prices/shareholders.

Crypto/Bond Relationship

Bonds are denominated in US dollars, and from a crypto-based perspective, purchasing power tends to zero infinitely, and the initiative for conversion conditions lies with MicroStrategy, borrowing a 'bond' that tends to zero purchasing power to buy Bitcoin with infinitely large purchasing power, especially with a zero default risk structure, which is a position that will not lose in the long cycle.

In both the crypto sphere and traditional finance for many years, I really haven't seen a master who can play triple arbitrage of stocks/bonds/cryptos to such an extreme.

Many people speculate whether MicroStrategy's outcome will be a stock version of Luna. I think in terms of overall risk structure, the two are not comparable at all, let alone the so-called death spiral.

As for when the flywheel stops turning and when the music stops, the core lies in how long the high premium of stocks and individual net coins can be maintained.

If market trends break expectations, and the supply of Bitcoin derivatives increases, if MicroStrategy's stock/crypto premium shrinks to below 1.2, this financing will be difficult to sustain. But MicroStrategy will still be a big winner.

The structural construction of MicroStrategy's long-term winning face truly rivals Buffett's Berkshire Hathaway in the traditional financial world.

From the standpoint of premium levels, MSTR reaching $1 trillion seems easier than Ethereum reaching $1 trillion 😂.

A few final points. MicroStrategy currently has a 300% premium over Bitcoin. Participants in the secondary market, if they do not understand the variables involved, face extremely high risks. The continuously growing volume means that premiums will only shrink rather than expand; the sustained financing capability is one of the variables that turns the premium from virtual to real.

Also, it would be best if everyone learned from MicroStrategy. If a hundred listed companies learn its Bitcoin standard and raise the overall holding cost of Bitcoin, it would collectively help reduce the premium bubble.

Can other assets (like ETH, SOL, meme) replicate the same strategy? The core of this strategy is having enough counterparties willing to accept similar convertible bond terms, and their acceptance is because more counterparties wish to gain exposure to different risk combinations compared to Bitcoin.

Assets like ETH/SOL have added more economic models, technology, and market risks beyond liquidity, making them much more difficult to operate, but the potential returns are also high, so it’s hard to say if a degen version of MicroStrategy could be created.

I feel that the institutions are already rubbing their hands in anticipation.

Part Three: Netizen Communication and Questions

1. May I ask, what indicator has the 300% premium of MicroStrategy over Bitcoin now?

Answer: Stock market value / holdings of Bitcoin market value

2. Is there such a risk?

Answer: The difference is that Bitcoin cannot be controlled by the Federal Reserve; MicroStrategy is actually using high-priced stocks (permanent capital) to buy Bitcoin, not bonds, which will not lead to liquidation.

3. Netizen BTC Cycle Master: The six stock issuances were all issued at par, not at a premium. The choice of converting stocks or cash repayment lies with MicroStrategy and not with the convertible bondholders; this statement is ambiguous. It's better to say that buyers cannot choose early redemption. If copycats increase, and MSTR loses its advantage due to high premiums, it will begin to decline until there is no premium.

Answer: The premium refers to the premium of the stock price over the net value of Bitcoin (not the premium of the stock market price).

4. Teacher Mindao, is there a similar design in DeFi?

Answer: luna, eos's ICO

5. Netizen Jiubianliuzhen Iron Man: Indeed, this is the case. I just understood that his financing cost is zero, just like Buffett, who relies on insurance company funds for zero-cost financing.

Answer: Buffett is even more impressive; his financing cost is negative because the insurance float has a positive profit at the operational level, which is extremely rare in insurance companies. Most rely on investment income to offset operational losses.

6. Netizen morahaji: Reaching $1 trillion is unlikely; it requires holding $250-300 billion in Bitcoin market value, assuming Bitcoin is $250,000-300,000 each, it would need to hold 100,000 coins. He can't buy that much this round, and in the next round, he can't afford that much. If this round he can buy 50,000 coins and doesn't liquidate, he might reach a market value of $1 trillion.

Answer: The possibility in this cycle is not high. But $1 million Bitcoin is not that difficult, after all, the ETF volume is quite close to this number, and it has not been a year yet.

7. havegas.eth: This is what I found, not sure if it's correct, but the options for converting stocks and bonds are limited; otherwise, it would really be impossible for anyone to buy.

Answer: There are restrictions; most of the restrictions are routine clauses that make it easier for convertible bond investors to justify to their legal and investment committees (such as the occurrence of cross-default, significant changes in debt terms, etc.).

8. Netizen SoullessL.fuel: Interest doesn't count; if there's no cash to repay the principal borrowed, can it be directly given in shares? But if he has to repay $10 billion in principal and the stock market is only worth $1 billion, how is that calculated?

Answer: The conversion price is locked in advance and is no longer related to the stock market value.

9. Netizen B (🤿, 🤿): Although creditors indeed aim for the huge upside of converting to stock, zero interest, five years is fine, but it is really hard to imagine how these creditors can accept that the conversion initiative is not in their hands. However, this system can be played with BTC, but I estimate it will be difficult with ETH.

Answer: Asian bond traders are also puzzled about how this can be sold; in the US market, any tool with a stock nature that has a daily trading volume of $50 billion will have a very large market. The main narrative of BTC is too strong, and many in traditional finance are buying in, while ETH is still a bit lacking.

10. Netizen peter 🐉 $MON ꧁IP꧂: Please ask, if convertible bonds are converted into stocks and the stock price happens to be bad and cannot be sold for the debt previously lent to MSTR, isn't that a loss?

Answer: The conversion price is set at a premium of 30% above twice the net assets, so how can it lose 😂. The loss is also borne by the convertible bondholders who were forced to convert.

11. Netizen alpacino: Are there convertible bonds where the choice is in the hands of the issuer? Who would buy such convertible bonds? Only risks with no returns (interest is zero)

Answer: Very good question. Several possibilities, the conversion price is significantly above net assets, and converting the bond itself lowers the debt ratio, making the choice to convert a win-win for both MSTR and convertible bondholders. Unless in extreme situations, there is no reason not to convert. Additionally, I heard that many who buy convertible bonds do so in conjunction with short-selling strategies of stocks for arbitrage. Various combinations are possible here.

12. Netizen Riguang Blockchain:

Those who understand naturally won't short MicroStrategy, especially when a raging bull market is about to begin. Xiangyuan probably missed the boat; with money borrowed at almost zero interest to buy Bitcoin worth decades, any fool knows this is a surefire win, coupled with Trump's pro-crypto stance, pressuring the Democrats to force funds to flow back! It seems that assets priced in dollars will rise!

13. Netizen DD:

Looking back, although $MSTR was shorted by CITRON and plummeted 16%, I don't think MSTR will immediately enter any death spiral; this is just an overvaluation, but Michael Saylor's financial game can still continue. For me, the condition for buying MSTR is that if one day Bitcoin reaches $1 million each, and MSTR owns 1 million coins by then, then buying MSTR at the current price is far more profitable than directly buying Bitcoin at the current price in the future; I would choose to buy MSTR, otherwise, I would just hold Bitcoin.

14. Netizen business919(💙,🧡)(L3, ❄️)

MicroStrategy is betting that the future demand for Bitcoin (investment, strategic reserve, transfer payments, DeFi collateral) will increase, and the maximum supply of Bitcoin is only 21 million. This means that as demand increases, prices will only go up, hoarding Bitcoin is the best flywheel effect!

(End of full text)