Key Points

Despite the steady adoption of digital assets and the maturing industry, some still claim that cryptocurrency is primarily used for financial crime, ignoring its minimal and waning role in illicit transactions.

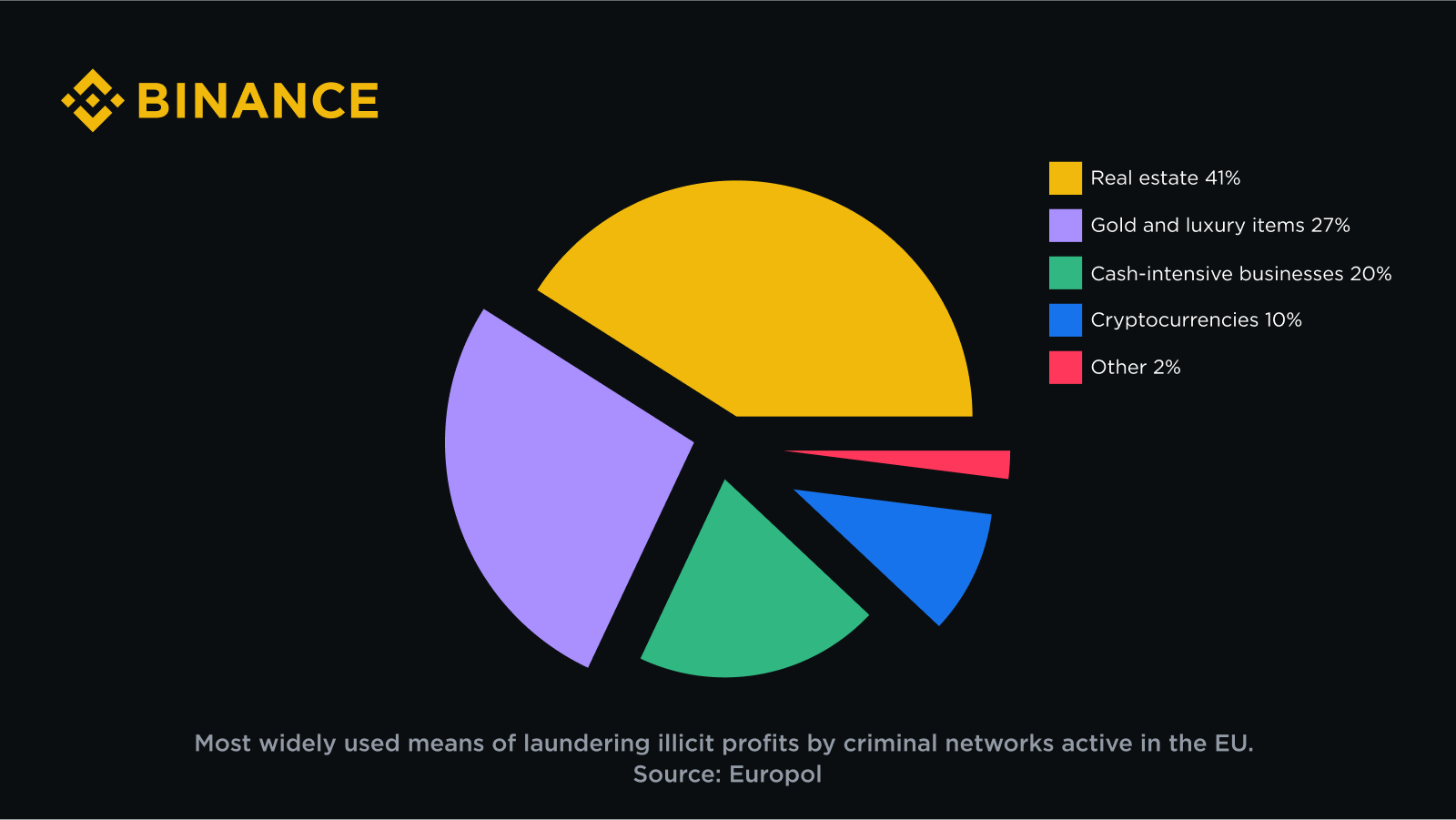

Data from Europol shows that among major criminal networks in the European Union, real estate, luxury goods and cash-intensive businesses are the main means of money laundering, while cryptocurrencies only account for a small part.

The Nasdaq and U.S. Treasury Department reports noted a huge disparity in the size of illicit funds in the traditional and digital asset sectors, with the latter accounting for only a small portion of the total.

In 2024, Wall Street companies, led by BlackRock, the world's largest asset manager, competed to provide mainstream investors with Bitcoin investment opportunities through regulated exchange-traded products. Millions of people around the world use digital assets to preserve their savings to resist the impact of high inflation and depreciation of their own currencies. At the same time, cross-border cryptocurrency transfers with low fees and near real-time arrival are also highly sought after. With the high efficiency and new functions brought by blockchain technology, traditional fields from charitable donations to art have been revitalized and opened up new imagination space.

However, it is strange that there are still some people who turn a blind eye to the great progress made by the digital asset industry in recent years and cling to some wrong or outdated stereotypes. They claim that cryptocurrencies are just a kind of online casino, and their main use is to facilitate money laundering and various other crimes. This has led some of the most radical skeptics to call for the regulation of digital assets and outright banning them.

Reliable data shows that illegal cryptocurrency transactions accounted for only 0.34% in 2023, a further decrease from 0.42% the previous year, and the value of digital assets obtained by illegal addresses is also extremely small and has been declining year by year, but these data are difficult to convince those stubborn detractors. After all, most of the strong data insights we can present come from within the industry.

In reality, however, even unconnected data sources provide ample evidence that cryptocurrencies are far from the first choice for malicious actors to commit financial crimes. Here are some statistics showing that by far, the assets and instruments most often used as a means of crime are precisely those that no one would suggest banning.

Europol: Real estate sector is a top target for EU criminal networks

Europol, whose mission is to help EU member states fight serious international and organised crime, focuses on large-scale criminal and terrorist networks operating across the EU. Its latest report provides a comprehensive assessment of the most threatening criminal networks operating in Europe.

What these criminal organizations, which specialize in activities such as drug trafficking, cyber fraud and property crime, have in common is the need to legalize their ill-gotten gains. When evaluating the various tools used by criminal networks for this purpose, Europol experts found that real estate is the main means of money laundering (accounting for 41%), followed by luxury goods and cash-intensive businesses.

Although cryptocurrencies account for 10% of laundered funds, it is still far from what those who demonize cryptocurrencies claim. Moreover, based on the year-on-year downward trend observed in most other areas of crime, there is reason to believe that the next Europol Criminal Networks Report will show a decrease in the share of funds laundered through digital asset-related channels.

So the next time someone suggests banning cryptocurrencies on the grounds that they are a haven for money launderers, suggest they first ban real estate sales, luxury brand watches, or neighborhood newsstands.

Cryptocurrency accounts for less than 1% of global illicit funds

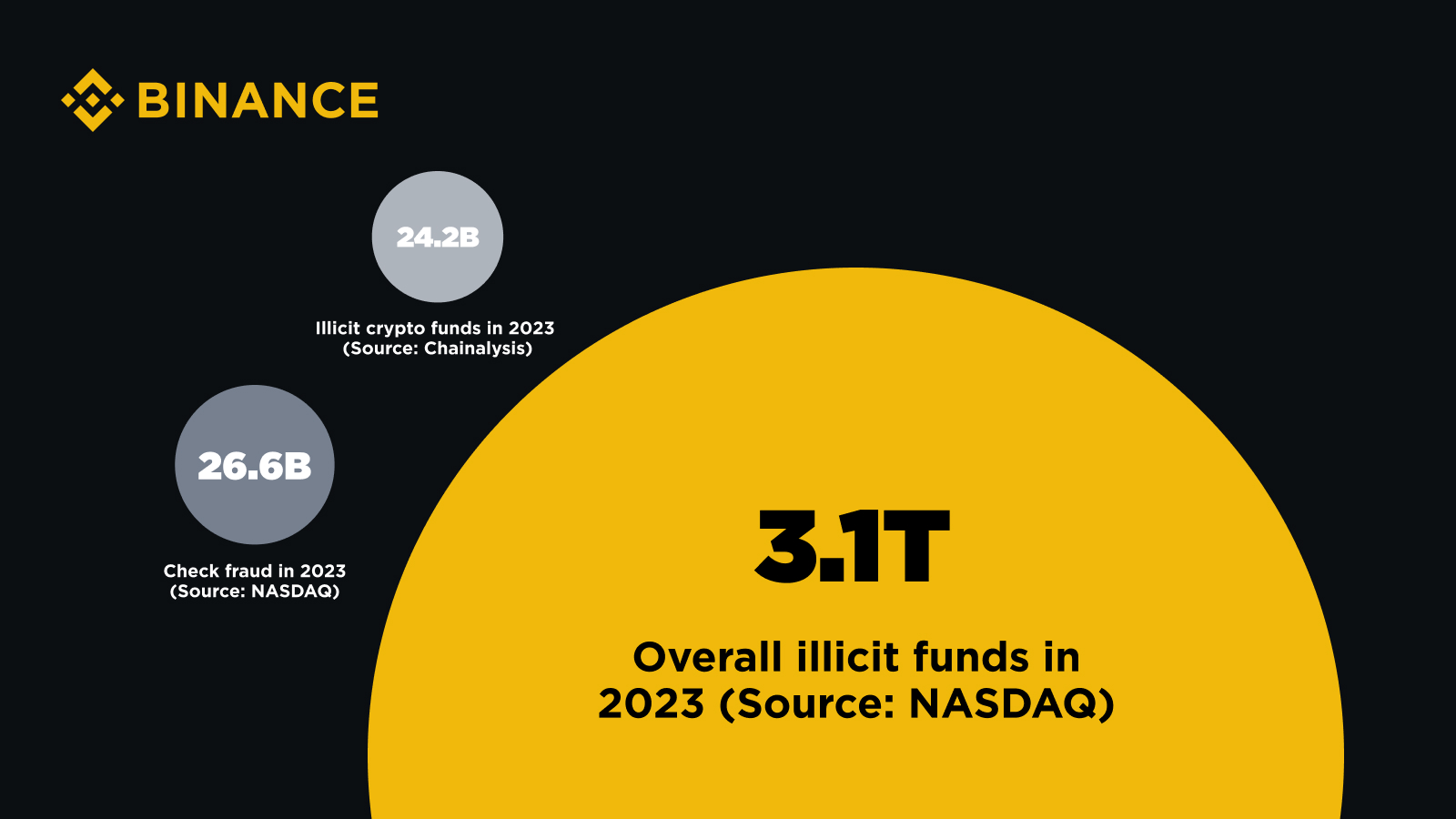

According to estimates by blockchain analytics firm Chainalysis, the total value of digital assets acquired by illicit addresses in 2023 was $24.2 billion, a significant decrease from $39.6 billion in 2022. These figures include assets stolen in cryptocurrency hacks as well as funds sent to illicit wallets designated by Chainalysis. Illegal wallets include addresses associated with ransomware groups, fraudulent activities, dark web black markets, and terrorist financing, with the largest number of addresses associated with sanctioned entities and jurisdictions. This is perhaps the most rigorous and comprehensive assessment of the scale of criminal activity related to digital assets that we have ever conducted.

While $24 billion sounds like a lot, it’s just the tip of the iceberg when it comes to all the financial crime activity. According to Nasdaq’s recently released Global Financial Crime Report, the total amount of illegal funds (including cryptocurrencies and fiat currencies) processed by the global financial system last year was as high as $3.1 trillion.

While the two figures are not completely comparable, as they come from two different reports and use different statistical methods, they can at least give us a rough idea of the relative size of the two phenomena. $24.2 billion represents less than 1% of the $3.1 trillion. More specifically, the amount of illicit cryptocurrency funds counted by Chainalysis only accounts for 0.78% of the total amount of illicit funds counted by Nasdaq worldwide.

Nasdaq’s report further states that more than $485 billion of the total losses in 2023 will be caused by various forms of scams and fraudulent activities. The amount of illicit funds generated by bank check fraud is comparable to that of digital asset-related activities, causing losses of $26.6 billion to individuals and businesses last year, mainly in the Americas, where checks are still widely used.

In other words, checks, a legacy technology that survives largely due to the enormous inertia of banking, are responsible for more financial crime than an entire innovative asset class, which has been branded a safe haven for criminals. Is it time to ban these clunky banknotes?

Treasury: Cryptocurrency money laundering is far less common than traditional money laundering methods

The U.S. Treasury Department publishes a National Money Laundering, Terrorist Financing, and Proliferation Financing Risk Assessment report each year, detailing the main illicit financial vulnerabilities and risks that pose a threat to U.S. citizens. The 2024 National Money Laundering Risk Assessment Report references existing and evolving trends in cryptocurrency-related risks, while noting that “the use of virtual assets for money laundering remains far less than fiat currencies and traditional methods that do not involve virtual assets.”

The report focuses on persistent and emerging money laundering risks in traditional sectors, such as the abuse of legal entities, the lack of transparency in certain real estate transactions, the lack of comprehensive AML/CFT systems in related industries such as investment advisors, collusion among professionals to abuse their position or business, and weaknesses in compliance and supervision of some regulated financial institutions.

All of these areas highlight structural flaws inherent in traditional financial systems and corporate practices, demonstrating that financial crime is a systemic problem that cannot be blamed solely on specific technological infrastructure or asset classes.

Cryptocurrency is the solution, not the problem

As we look to the future of the financial industry and think about where it is headed, we must continue to examine and expose outdated and completely wrong ideas about digital assets. Cryptocurrencies are far from being the primary tool for financial crime and account for a tiny fraction of the world's illicit funds. Data shows that traditional methods and tools such as real estate transactions and traditional banking are the hardest hit areas for illegal activities such as money laundering.

Rather than viewing cryptocurrencies as a scapegoat for systemic financial crime, we should focus more on these traditional sectors and the deep-rooted problems within them. Despite the constant skepticism, data from a variety of unrelated sources strongly demonstrates the significant developments in the cryptocurrency industry and how it is far from being the first choice for criminals. Solving systemic problems requires systemic solutions, and digital assets should be seen as part of the solution, not the source of the problem.