2024 will undoubtedly be an important year in the history of crypto.

This year, centered around the two core narratives of ETFs and the US elections, leveraging Bitcoin as the main tool, the cryptocurrency industry has successfully broken through in this year. Listed companies, traditional financial institutions, and even national governments have flocked in, significantly enhancing mainstream acceptance and recognition. The regulatory environment is also moving towards a clearer and more lenient path with the new government's rise, with mainstream collisions, path differentiation, and regulatory evolution becoming the industry's main theme this year.

01

Reviewing 2024: Bitcoin reaches its peak, Ethereum faces competition, and MEME casinos attract attention.

Looking at the main developments in the industry this year, Bitcoin is undoubtedly the core narrative.

ETFs and national reserves have propelled Bitcoin to successfully stand at $100,000, officially declaring Bitcoin's significance beyond cryptocurrency, extending to become a globally resilient anti-inflation asset. Its value as a store of value is recognized, and BTC is gradually transitioning from digital gold to a super-sovereign currency, marking a phased victory in this grand financial experiment that began with Satoshi Nakamoto. On the other hand, Bitcoin's ecosystem has expanded this year. Although inscriptions, runes, and even L2 are in a fiery state of highs and lows, Bitcoin's diversified ecosystem has already begun to take shape, with applications like BTCFi, NFT, gaming, and social networking continuously developing. Bitcoin's DeFi TVL surged from $300 million at the beginning of the year to $6.755 billion, with an annual growth of over 20 times. Among them, Babylon has become the largest protocol on the Bitcoin chain, with its TVL reaching $5.564 billion as of December 20, accounting for 82.37% of the total. The broader BTCFi has performed exceptionally well this year, with Bitcoin spot ETF shares surging and MicroStrategy being selected into the Nasdaq 100, reflecting Bitcoin's overwhelming success in the CeFi sector.

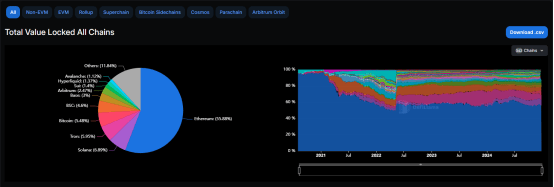

Returning to the public chain sector, this year's leader Ethereum has not had an easy time. Compared to other assets, its performance has been poor, with declining value capture and user activity, and the narrative is not as strong as before. The consensus around the revival of DeFi may sound loud, but aside from the TVL nesting wave triggered by re-staking, it seems that only Aave is shouldering the burden, with actual investment being evidently insufficient. However, the emergence of the dark horse Hyperliquid at the end of the year has not only dealt a blow to CEX but has also sounded the horn for DeFi's counterattack. On the other hand, following the Dencun upgrade, Ethereum Layer 2 has accelerated its internal competition and continues to vie for market share from the mainnet, leading to a heated discussion about Ethereum's mechanism, with a plethora of criticisms emerging, and even the rapid growth of Base has sparked rumors that the future of Ethereum belongs to Coinbase.

The strong rise of Solana contrasts sharply with this. From the perspective of TVL, Ethereum's market share in public chains has dropped from 58.38% at the beginning of this year to 55.59%. In contrast, Solana has jumped from being unknown at the beginning of the year to 6.9% at the end of the year, becoming the second-largest public chain after Ethereum. SOL has also created a growth miracle, skyrocketing from $6 two years ago to $200 now, with over 100% growth just this year. In terms of recovery path, leveraging its unique advantages of low cost and high efficiency, Solana has targeted core liquidity positioning, relying on Degen culture to leap to become the undisputed king of MEME, becoming the retail investor's concentrated camp this year. Solana's daily on-chain fees have repeatedly exceeded those of Ethereum, and the growth of new developers has also surpassed Ethereum, showing a significant catching-up trend.

TON and SUI also stood out this year. With a user base of 900 million, Telegram has single-handedly ignited the chain gaming field, opening a new entry for Web3 traffic and providing strong stimulation to a market that had been quiet for a long time before September. Backed by this massive tree, TON has finally entered the fast lane of growth after being stuck in the dawn before the explosion for a long time. According to Dune data, TON's cumulative on-chain users have exceeded 38 million, with a cumulative transaction volume exceeding $2.1 billion. SUI has gained favor entirely through price growth. The Move language public chain has made rapid progress, with hardware expansion, diverse protocols, and airdrop introductions working in tandem, seeming to have a bright outlook. Compared to SUI's price-driven rise, the Aptos public chain, despite showing relatively weak price performance, has gained favor from traditional capital, successfully establishing partnerships with BlackRock, Franklin Templeton, and Libre this year. Its compliant attributes may bring it into the spotlight in the new RWA and BTCFi cycles.

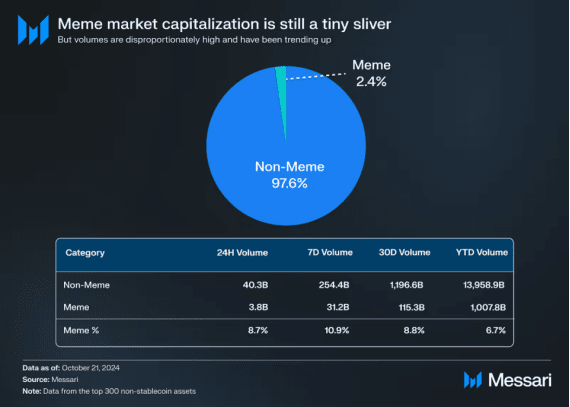

From an application perspective, MEME is the primary driver of the market this year. Essentially, the rise of MEME signifies a shift in the current market landscape. VC tokens are not being acknowledged, and excess liquidity has nowhere to go, ultimately pouring into segments that are fairer and more profit-driven. Within this, the connotation of MEME is also continuously extending, evolving from a single speculative target to a typical representative of cultural finance. 'Everything can be MEME' is happening in reality. Although in terms of market capitalization, MEME accounts for less than 3% of the top 300 cryptocurrencies (excluding stablecoins), its trading volume continues to occupy 6-7% of the share, recently even surging to 11%, making it one of the most concentrated liquidity tracks. According to Coingecko data, MEME accounted for 30.67% of investor attention this year, ranking first among all tracks. Where attention goes, money naturally follows, and indeed, looking back at this year's MEME, presale fundraising, celebrity tokens, zoo battles, PolitFi, and AI have all been top trends in the industry.

In this context, the infrastructure surrounding MEME continues to solidify. The fair launch platform Pump.fun has emerged, not only reshaping the MEME landscape but also successfully becoming one of the most profitable and successful applications of the year. In November, Pump.fun became 'the first Solana protocol to surpass $100 million in revenue in a single month.' According to Dune data, as of December 22, Pump.fun's cumulative revenue exceeded $320 million, with a total number of deployed tokens around 4.93 million.

Of course, a platform making money does not mean retail investors are making money. Considering the one in a hundred thousand odds of the golden dog, and only 3% of users can profit over $1,000 on Pump.fun, coupled with the increasingly prominent trend of MEME institutionalization, from the user's perspective, regardless of how fair it seems, the divide between profit and loss is hard to avoid. Perhaps it is for this reason that adding fundamentals to MEME has become a new development model for projects. Most long-cycle projects like Desci and AIMEME have adopted this model, but from the current perspective, fleeting moments still dominate, and the gold content of 'running fast to survive well' is still on the rise.

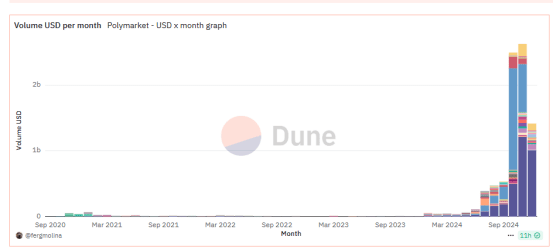

Influenced by the US elections, another legendary application has emerged. Polymarket has surpassed all betting platforms on the market, gaining widespread acclaim in the prediction market for its high accuracy. In just October, Polymarket's website traffic reached 35 million visits, double that of popular betting sites like FanDuel, with monthly trading volume surging from $40 million in April to $2.5 billion. A wide user base and genuine demand equate to clear value applications, which is why Vitalik Buterin speaks highly of it. The only regret is that it has not achieved large-scale conversion of crypto users. However, the new fusion of media and betting is undoubtedly approaching gradually.

As the year comes to an end, large models are transitioning from technology to application, evidently presenting a heated competitive landscape. After a year of AI oscillating in the Web3 spotlight, it finally makes a comeback to become the annual dark horse. MEME sparks the initial explosion, with Truth Terminal quickly bringing in the golden dog GOAT, ACT, and Fartcoin, recreating the hundredfold myth and igniting a frenzy for the niche application of AI Agents. Currently, almost all mainstream institutions are optimistic about AI Agents, believing they are the second phenomenal track after DeFi. However, as of now, the infrastructure in this field is still not complete, and applications are mostly concentrated on surface layers like MEME and Bots, with few deep integrations of AI and blockchain. But newness also means opportunity, and cyber-style token trading still awaits further observation.

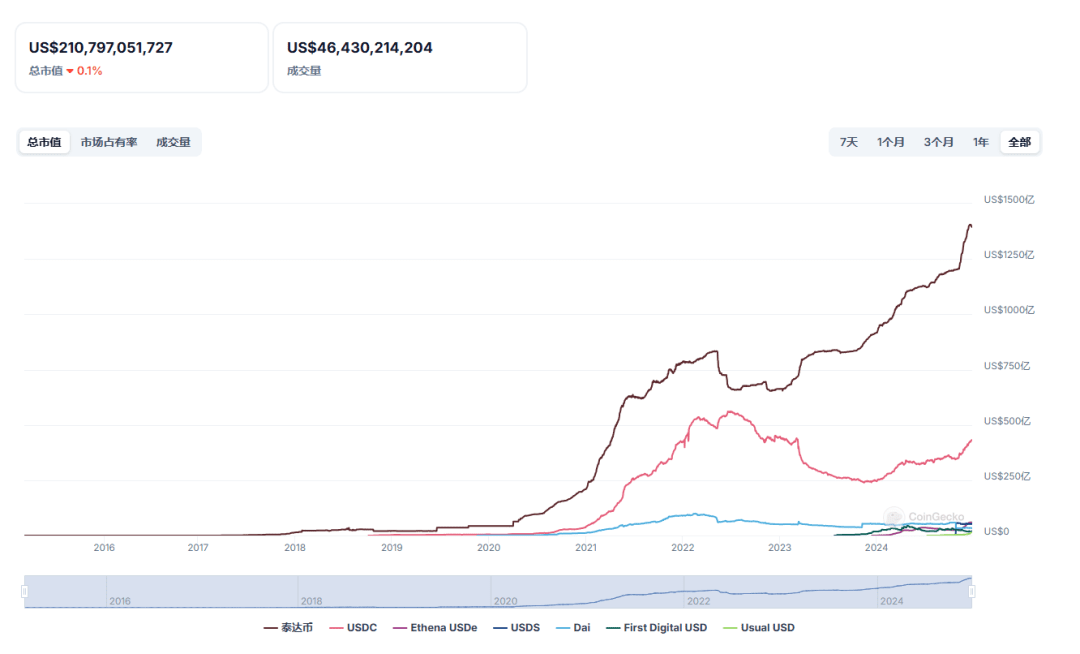

On the other hand, from the core driving institutions of this bull market, seamlessly connecting traditional finance and Web3, PayFi is sure to be at the forefront. Stablecoins and RWA are typical representatives among them. Stablecoins have truly revealed the anticipated large-scale applications this year, not only growing rapidly in the crypto sector but also beginning to occupy a place in the global payment and remittance market. Regions such as Sub-Saharan Africa, Latin America, and Eastern Europe have started bypassing traditional banking systems, directly using stablecoins for transaction settlements, with year-on-year growth exceeding 40%. Currently, the circulating value of stablecoins exceeds $210 billion, significantly higher than the tens of billions in 2020, with an average of over 20 million addresses transacting stablecoins on public blockchains monthly. Just in the first half of 2024, the settlement value of stablecoins has exceeded $2.6 trillion. Among new products, Ethena stands out as the best-performing stablecoin project this year, further sparking the trend of yield-bearing stablecoins, which is also the main driver of AAVE's revenue this year. RWA, on the other hand, was ignited after BlackRock announced its entry, expanding from a market value of less than $2 billion three years ago to $14 billion this year, covering multiple sectors such as lending, real estate, stablecoins, and bonds.

In fact, the development of PayFi is consistent with market performance. It is precisely because the internal market growth has encountered bottlenecks that the mainstream institutional market, as an increment, is at the beginning of a new cycle. To seek incremental space, PayFi has entered a critical process at this stage. It is worth noting that due to its connection with the traditional financial system, this field is also the most favored Web3 track by government agencies. For instance, Hong Kong, China, has already listed stablecoins and RWA as important areas for development next year.

Of course, despite the seemingly positive outlook, it cannot be denied that the cryptocurrency sector has undergone an exceptionally challenging stress test against the backdrop of nearly two years of macro tightening and industry downturn cycles. Innovative applications are hard to show, internal conflicts have intensified, and continuous restructuring and mergers are ongoing. The weakening of liquidity has led to a path differentiation in the crypto industry, forming a pattern where Bitcoin sees core inflows, continuously siphoning off other currencies. The altcoin market has spent most of this year in a garbage time, and the saying that 'this round of bull market has no altcoins' has been repeatedly confirmed and refuted, only rebounding at the end of the year under Wall Street's attention, marking the beginning of the altcoin season. From the current perspective, path differentiation will still continue in the short term, and the trend will likely become more pronounced.

02

Looking ahead to 2025: New cycle, new applications, new directions

Returning to the present, the New Year's bell is about to ring. Looking ahead to 2025, with the Trump administration unveiling a new era for crypto, capital-rich institutions are also eager to try. As of now, more than 15 institutions have released market forecasts for next year.

In terms of price predictions, all institutions are optimistic about Bitcoin's value, with 15-20 million being the peak price range according to six institutions. Among them, VanEck and Dragonfly believe the price will reach $150,000 next year, while Presto Research, Bitwise, and Bitcoin Suisse believe it could reach $200,000. If based on strategic reserves, Unstoppable Domains and Bitwise have even proposed predictions of $500,000 or higher. As for other cryptocurrencies, VanEck, Bitwise, and Presto Research have provided forecasts, believing ETH will be around $6,000-7,000, while Solana could range from $500-750, and SUI may rise to $10. Presto and Forbes estimate that the total market capitalization of cryptocurrencies will reach $7.5-8 trillion, while Bitcoin Suisse states that the total market capitalization of altcoins will increase fivefold.

Price prediction naturally has support, almost all institutions believe that the US economy will achieve a soft landing next year, and the macro environment will improve. Meanwhile, cryptocurrency regulation will also be relaxed, with more than five institutions holding a positive view on Bitcoin as a strategic reserve, believing that at least one sovereign nation and numerous listed companies will include Bitcoin in their reserves. All institutions believe that increased ETF inflows will become an objective fact.

From a specific track perspective, stablecoins, tokenized assets, and AI are the areas most focused on by institutions. In terms of stablecoins, VanEck believes that the settlement volume of stablecoins will reach $300 billion next year, while Bitwise indicates that with accelerated legislation, financial technology applications, and global settlement promotions, the scale of stablecoins will reach $400 billion. Blockworks Mippo is even more optimistic, providing an estimate of $450 billion. A16z also believes that companies will increasingly accept stablecoins as a payment method. Coinbase has pointed out in its report that the next wave of true cryptocurrency adoption (killer applications) may come from stablecoins and payments.

In terms of tokenized assets, A16z, VanEck, Coinbase, Bitwise, Bitcoin Suisse, and Framework all express optimism about the track. A16z's forecast mentions that as the cost of blockchain infrastructure decreases, the tokenization of non-traditional assets will become a new source of income, further promoting a decentralized economy. VanEck provided specific figures, believing that the value of tokenized securities will exceed $50 billion, which aligns with Bitwise's forecast data. Messari has provided differentiated conclusions based on reality. It believes that with the decline in interest rates, tokenized government bonds are expected to face resistance, but idle on-chain funds may receive more attention, with a shift from traditional financial assets to on-chain opportunities.

In the AI direction, A16z, which has heavily invested in the AI field, remains highly optimistic about the combination of AI and crypto. It believes that the autonomous agency ability of AI will be greatly enhanced, allowing artificial intelligence to have dedicated wallets to achieve subjective actions. Meanwhile, decentralized autonomous chatbots will become the first truly autonomous high-value network entities. Coinbase also agrees, pointing out that AI agents equipped with crypto wallets will be at the forefront of disruptive fields. VanEck states that on-chain activities of AI intelligences have exceeded one million, while Robot Ventures believes that the total market value of AI agent-related tokens will increase at least fivefold. Despite Dragonfly agreeing that tokens will rise significantly, it maintains a relatively conservative view on actual applications, believing that the applications of underlying protocols may be relatively limited.

Bitwise and Defiprime point out the core use scenarios. The former believes AI Agents will lead to a Meme explosion, while the latter states that DeFi is the deeply integrated scenario. Messari provides more specific pathways, believing the integration of AI and crypto has three major directions: first, new types of AI casinos like Bittensor and Dynamic TAO; second, blockchain technology will be used for fine-tuning small and specialized models; third, the combination of AI Agents and MEME.

In other areas, institutions have different focal points for predictions. For instance, YBB believes the revival of DeFi will be the main theme of 2025, Robot Ventures anticipates a wave of consolidation in application chains and L2 tracks, and Messari estimates that nearly all infrastructure protocols will adopt ZK technology in 2025. The DEPIN industry is projected to achieve revenue between eight and nine figures by 2025, while VanEck and Bitcoin Suisse predict a return of NFTs, among others. Due to the abundance of information, details are not elaborated here.

03

Conclusion: Where do investors go from here?

Despite slightly differing arguments and variations in subfields, it is evident that all institutions hold optimistic and proactive expectations for next year. Whether in terms of price increases, ecosystem expansion, or mainstream adoption, they are expected to continue reaching new heights in 2025.

It is foreseeable that, from a price perspective, the rise in mainstream coin prices is inevitable, especially in Q1 of next year, which will be a period of intensive policy benefits. The altcoin market will continue to differentiate, and under the influence of ETFs, altcoins that comply with regulatory tones will find it easier to attract capital inflows and continue narratives, while others will gradually retract. If macro liquidity tightens, the risks of altcoins will become increasingly prominent.

From an industry perspective, strong old public chains still hold ecological advantages, but the impact from new public chains is unavoidable. Ethereum's value capture and narrative methods will continue to ferment, but optimistically, the influx of external funds may alleviate this somewhat, while technical expansions and the popularization of account abstraction will become significant breakthroughs for Ethereum in 2025. Solana's growth momentum remains under the influence of capital discourse, but its heavy reliance on MEME poses hidden risks, and competition with Base will intensify. Additionally, a number of new public chains such as Monad and Berachain are expected to enter the market for competition.

The direction of development from infrastructure to applications is the major trend for future industry growth, with consumer-level applications becoming the main focus in the coming years. Application chains and chain abstraction may become the primary methods for building DAPPs. From the track perspective, the revival of DeFi has become a consensus, but at this stage, it is still reflected in AAVE, while the focus on centralized aspects is on the payment track, with Hyperliquid and Ethena still worthy of attention.

The speculative trend surrounding MEME is likely to continue in the short term, but the pace will significantly slow down, especially under the influence of the altcoin season. However, key directions such as Politifi still have relatively long narratives to pursue. Nevertheless, the infrastructure surrounding MEME is expected to improve, enhancing user experience, lowering barriers to entry, and institutionalization of MEME is an inevitable trend. It is noteworthy that new methods of token launches will always trigger new rounds of excitement.

As the incremental market comes from institutions, the tracks favored by institutions are expected to accelerate development. Stablecoins, AI, RWA, and DePin will still become the focus of the next narrative. Furthermore, in the context of tight liquidity, any on-chain liquidity tools and protocols that can increase leverage are likely to gain favor.

A new cycle is about to arrive, and as investors, it is essential to discard the old and welcome the new, discover cycles, adapt to cycles, and engage in deep research and participation.