Key takeaways

Despite the stable adoption rate of digital assets and the maturation of the sector, some still ignore the evidence of the minor and increasingly insignificant role of cryptocurrencies in illicit transactions, and argue that they are primarily a tool of financial crime .

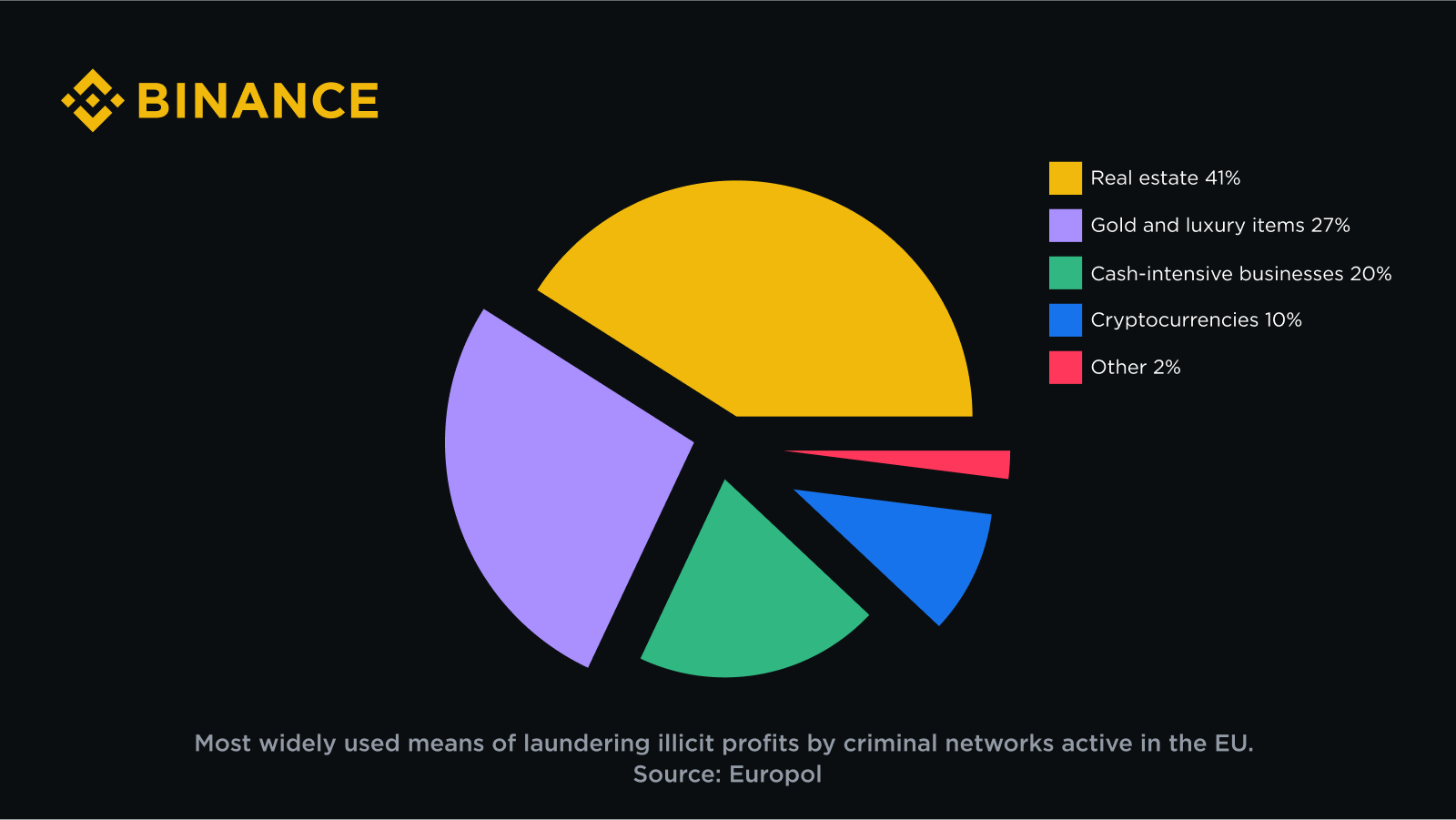

Europol data suggests that real estate, luxury items and businesses with high cash flow are most often used by large European criminal networks to launder money, and that cryptocurrencies only help to a lower percentage of this practice.

Reports from NASDAQ and the US Treasury Department illustrate the considerable disparity between the volumes of illicit funds in traditional sectors and those in digital assets, with the latter representing only a small share of the totals recorded.

In 2024, Wall Street companies, led by BlackRock (the world's largest asset manager), are striving to expose traditional investors to Bitcoin by offering them regulated products traded on exchanges. Around the world, millions of people are using digital assets to protect the value of their savings as inflation soars and national currencies devalue, as well as to take advantage of low-cost cross-border money transfers. cost and almost instantaneous. Traditional industries, from charitable giving to art, are improving and reinventing themselves by benefiting from the innovative capabilities and efficiencies offered by the use of blockchain technology.

And yet, curiously, there remain people who stubbornly refuse to acknowledge the progress the digital assets industry has made in recent years, instead resorting to hackneyed notions that were never true or are hopelessly outdated. These individuals argue that cryptos are nothing more than an online casino, whose primary use case is to facilitate money laundering and various other crimes. The most radical of these skeptics even call for excessive regulation of digital assets, or even their outright ban.

Reliable data shows that the share of illicit crypto transactions in 2023 was only 0.34%, compared to 0.42% in the previous year; other reports indicate that the value of digital assets received by illicit addresses is low and decreasing year over year. All this, however, is rarely enough to convince these staunch detractors: after all, most sources of this reliable information come from the industry itself.

In fact, even unaffiliated data sources provide enough evidence supporting the idea that cryptos are far from being the first choice for bad actors committing financial crimes. Today we present to you several statistics proving that the most common instruments of crime are by far the goods and tools that one would never dream of prohibiting.

Europol: EU criminal networks prefer real estate

The European Union Agency for Law Enforcement Cooperation (Europol) is responsible for helping EU Member States combat serious international and organized crime. As such, it focuses on large-scale criminal and terrorist networks operating across the Union. The latest report published by the agency contains a comprehensive assessment of the activities of the most threatening criminal networks in Europe.

All these criminal organizations involved in drug trafficking, online fraud, property crime and other malicious operations have one thing in common: their members need to launder their ill-gotten gains. By assessing the prevalence of the various tools that criminal networks use for this purpose, Europol experts found that real estate is most often used in money laundering (41%), followed by luxury items and businesses with high cash flow.

Cryptocurrencies are used to launder 10% of these funds, a much smaller percentage than those demonizing crypto would have us believe. Furthermore, it can reasonably be expected that the share of funds laundered through digital asset-related channels will further decrease in the next version of the Europol Criminal Networks Report, given the observed downward trends of year over year in most other criminal areas.

The next time you hear someone suggest banning cryptocurrencies because of their role in money laundering, you might respond by suggesting banning door-to-door sales, removing the sale of luxury watches, or the closing of the local newsstand in the first place.

Less than 1% of illicit funds worldwide

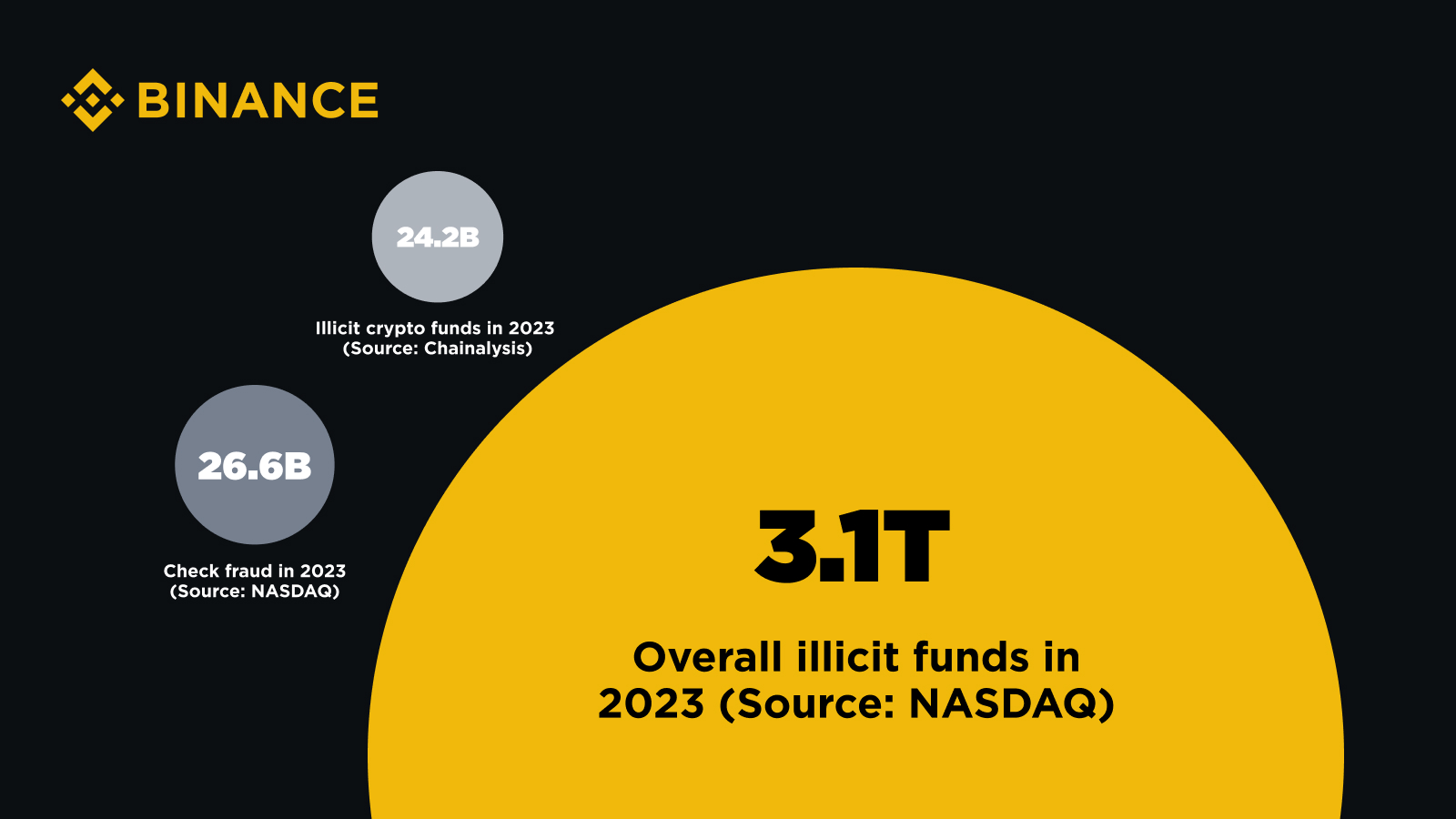

Blockchain analysis firm Chainalysis estimates that the total value of digital assets received by illicit addresses in 2023 was $24.2 billion, up from $39.6 billion in 2022. These figures include assets stolen in crypto hacks as well as funds sent to wallets that Chainalysis has determined to be illegal and whose addresses are associated with ransomware groups, fraudulent operations, darknet markets , to the financing of terrorism and above all, to entities and jurisdictions subject to sanctions. This is perhaps the most rigorous and comprehensive study of the scale of criminal activity associated with digital assets available to date.

$24 billion is a huge amount; but what exactly does it represent, all financial crimes combined? The recent global financial crime report from NASDAQ estimated the total sum of illicit funds (fiat and crypto) that passed through the global financial system last year at 3.1 $1 trillion.

Although these two figures are not completely comparable (they are in fact taken from two separate reports using different methodologies), they give a fairly good idea of the relative magnitude of the two phenomena. 24.2 billion is less than 1% of 3.1 trillion; specifically, Chainalysis calculates that the volume of illicit crypto funds constitutes exactly 0.78% of the total volume of global illicit funds determined by NASDAQ.

To put things in perspective, the NASDAQ report attributes more than $485 billion of total 2023 losses to various forms of scams and fraud. Bank check fraud generated an amount of illicit funds comparable to that associated with digital assets and caused individuals and businesses to lose $26.6 billion last year, primarily in the Americas where they are still widely used.

In other words, checks, an old payment method whose existence in our time is due to the remarkable inertia of banking practices, are used to perpetrate more financial crimes than an entire innovative asset class still portrayed in wrongly as the tool of choice for criminals. Is it time to ban these awkward pieces of paper?

Treasury: Conventional money laundering methods far outpace crypto

Each year, the United States Department of the Treasury publishes its National Risk Assessments on Money Laundering, Terrorist Financing, and Proliferation Financing. which detail the key vulnerabilities and risks related to illicit financing and threatening Americans. The Money Laundering Risk Assessment for 2024 does not ignore existing and evolving trends in risks associated with cryptocurrencies, but specifies that “the use of virtual assets for money laundering is still significantly lower than fiat currencies and more conventional methods that do not involve virtual assets.”

The majority of the report focuses on persistent and emerging money laundering risks related to conventional areas such as misuse of legal entities, lack of transparency of certain real estate transactions, lack of comprehensive coverage anti-money laundering and counter-terrorist financing for affected sectors (e.g. lack of oversight of investment advisors), complicit professionals who abuse their positions or businesses, and gaps in compliance and supervision of certain regulated financial institutions.

All of these areas represent familiar structural failures inherent in the traditional financial system and corporate practices that highlight the systemic nature of financial crime; This is not a problem that could be attributed to a specific type of technology infrastructure or asset class.

A solution rather than a problem

As we look to the future of finance and think about where the industry is headed, it is essential to continually examine and set the record straight on outdated and outright misconceptions about digital assets. Far from being the instrument of choice for financial criminals, cryptocurrencies represent a relatively insignificant portion of illicit funds worldwide. Data shows that traditional methods and tools like real estate transactions and old banking practices are much more frequently used as conduits for illicit activities like money laundering.

Instead of making cryptocurrencies the scapegoats for systemic financial crimes, it would be good to pay more attention to these classic areas and the problems rooted in them. Despite lingering skepticism, compelling data from a variety of unaffiliated sources highlights the significant developments in the cryptocurrency sector and how far they are from making it easier for bad actors. A systemic problem requires systemic solutions, and digital assets should be seen as part of that solution rather than an added challenge.